68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

USA Aerospace Parts Manufacturing Market (2026–2034): Forecasting from ~USD 92.4 Billion in 2024 to ~USD 178.6 Billion by 2034, CAGR (~6.8%) | Aerostructures, Engines, Avionics, Cabin Interiors & Aircraft Systems”

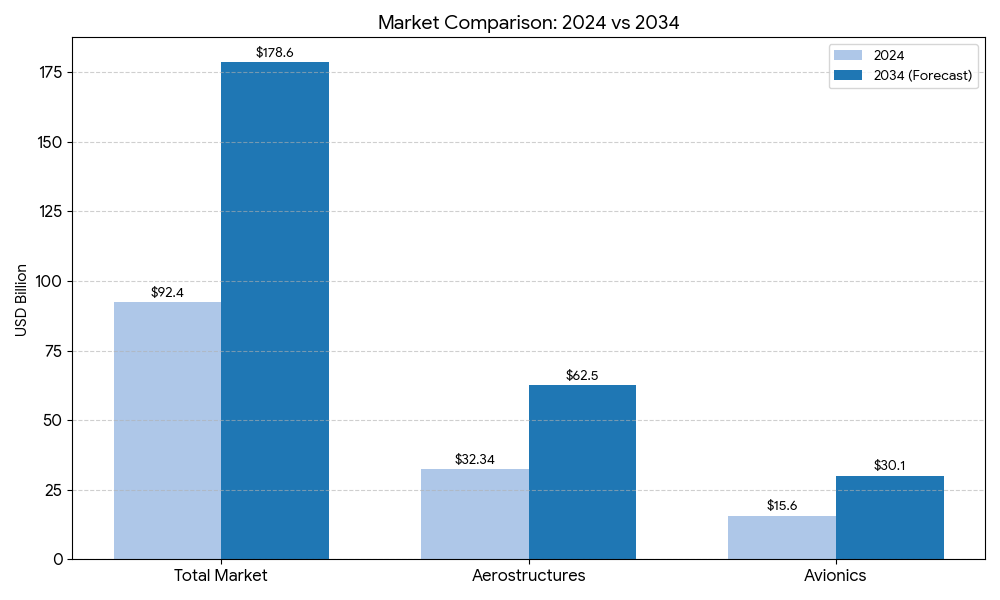

The U.S. aerospace parts manufacturing market is projected to grow from USD 92.4 billion in 2024 to USD 178.6 billion by 2034, expanding at a CAGR of 6.8%. Growth is driven by strong demand for next-generation aircraft, rising defense budgets, and technological advancements in lightweight materials, 3D printing, and digital manufacturing. The sector’s rebound post-pandemic is further supported by increasing commercial air travel, fleet modernization programs, and sustained exports of U.S.-made components. Key segments aerostructures, engines, avionics, cabin interiors, and aircraft systems—are witnessing innovation focused on fuel efficiency, noise reduction, and sustainability. Partnerships between OEMs and suppliers, coupled with AI-driven production optimization, are improving operational efficiency across the aerospace supply chain. The shift toward electric and hybrid aircraft will also reshape manufacturing priorities through 2034.

What's Covered?

Report Summary

Key Takeaways

- Market expected to expand from USD 92.4B (2024) to USD 178.6B (2034) at 6.8% CAGR.

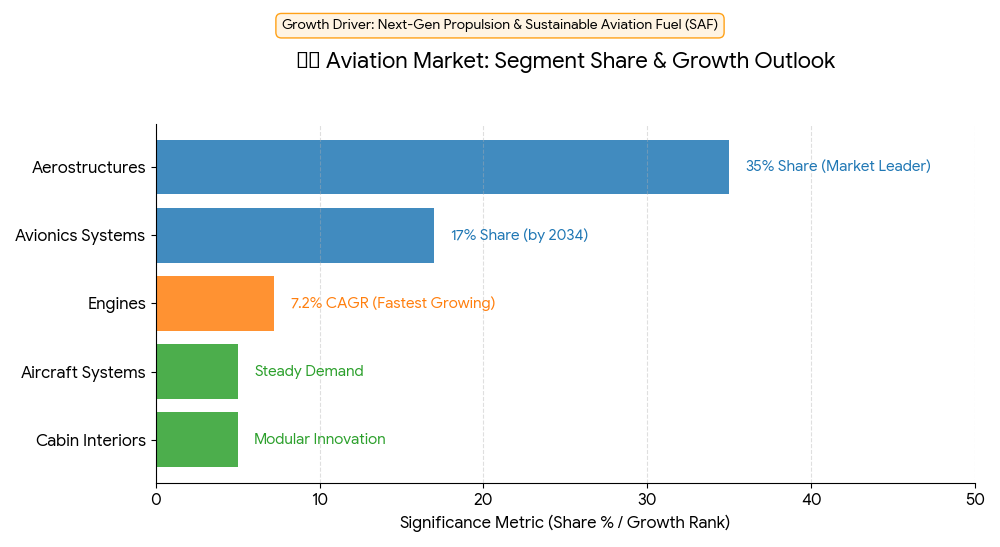

- Aerostructures remain the largest segment, accounting for 35% of total market share.

- Aircraft engine manufacturing to grow at 7.2% CAGR, driven by efficiency upgrades and hybrid propulsion.

- Avionics systems segment projected to reach USD 30.1B by 2034, led by digital cockpit and connectivity systems.

- Cabin interiors to record 6.1% CAGR, supported by passenger comfort and customization demand.

- Defense procurement programs to contribute over 25% of total revenue by 2030.

- Additive manufacturing (3D printing) adoption increasing at 12% annually for lightweight component fabrication.

- Sustainability focus driving shift toward composite materials and recyclable alloys.

- OEM-supplier collaboration optimizing lead times and reducing costs by up to 15%.

- Electric & hybrid aircraft R&D investments to surpass USD 5B by 2030, reshaping engine and avionics design.

Market Size & Share

The U.S. aerospace parts manufacturing market is forecast to grow steadily from USD 92.4 billion in 2024 to USD 178.6 billion by 2034, achieving a 6.8% CAGR. Aerostructures, including fuselage and wing components, dominate with 35% market share due to high replacement rates and ongoing fleet expansion. Engines will grow at 7.2% CAGR, driven by new-generation propulsion systems and hybrid aircraft research. Avionics will reach USD 30.1 billion by 2034, powered by demand for digital cockpit systems, cybersecurity, and in-flight connectivity. Cabin interiors and aircraft systems will follow closely as passenger experience remains central to fleet modernization. The overall market will benefit from sustained defense contracts, export competitiveness, and the push for lightweight, sustainable designs.

Market Analysis

A strong manufacturing base, supported by Boeing, Lockheed Martin, and a network of Tier 1 and Tier 2 suppliers, ensures U.S. dominance in global aerospace production. Growth is fueled by increased aircraft deliveries, defense programs such as F-35, KC-46, and B-21 Raider, and modernization of commercial fleets. The adoption of digital manufacturing and automation technologies has reduced assembly time and errors, improving throughput by nearly 20%. Composite materials like carbon fiber and titanium alloys are replacing traditional metals to enhance fuel efficiency. Moreover, supply chain diversification post-COVID is prompting localized production of critical aircraft components. Additive manufacturing continues to disrupt traditional part fabrication, particularly for engine nozzles, structural parts, and interior components, offering cost savings and rapid prototyping capabilities.

Trends & Insights

- Fleet Modernization: Rising replacement cycles in both commercial and defense segments driving consistent demand.

- Lightweight Materials: Growth in carbon fiber and titanium alloy usage for fuel-efficient designs.

- Additive Manufacturing Expansion: 3D printing adoption reducing production lead time by 25–30%.

- Sustainability Goals: OEMs adopting eco-friendly manufacturing processes and recyclable materials.

- Digital Twin Technology: Improving production simulation, part reliability, and maintenance planning.

- Defense Spending Surge: The U.S. Department of Defense increasing aircraft procurement budgets through 2030.

- AI-Driven Production Optimization: Enhancing quality control and process automation.

- Hybrid-Electric Aircraft: Early R&D investments driving a future shift in propulsion component design.

- Post-COVID Recovery: Increased travel and cargo demand boosting OEM and aftermarket revenues.

- Reshoring Initiatives: U.S. manufacturers expanding domestic capacity to mitigate supply chain risks.

Segment Analysis

The market is divided into aerostructures, engines, avionics, cabin interiors, and aircraft systems. Aerostructures dominate with 35% of market share, driven by continuous innovation in lightweight composites. Engine manufacturing is growing fastest at 7.2% CAGR, fueled by next-gen propulsion and sustainable aviation fuel compatibility. Avionics systems—comprising flight control, navigation, and connectivity—will account for 17% share by 2034. Cabin interiors are evolving toward modular, customizable designs for airlines seeking differentiation. Aircraft systems, including hydraulics and landing gear, maintain steady demand as aircraft production rates rise across commercial, defense, and cargo segments.

Geography Analysis

Key aerospace manufacturing hubs in the U.S. include Washington, Texas, California, and Kansas, each hosting major OEMs and supply chain networks. Washington leads with Boeing’s operations, while Texas and Alabama are expanding their defense production footprint. Ohio and Connecticut specialize in engine components and precision machining, while California drives R&D in advanced avionics and hybrid propulsion. Growing investments in Southern states—owing to favorable policies and lower operational costs—are further strengthening the U.S. aerospace supply base. Export demand from Europe, Asia, and the Middle East continues to reinforce the country’s manufacturing competitiveness.

Competitive Landscape

The U.S. aerospace parts manufacturing market is dominated by global leaders such as Boeing, Lockheed Martin, Raytheon Technologies (Collins Aerospace & Pratt & Whitney), GE Aerospace, and Northrop Grumman. Spirit AeroSystems, Hexcel Corporation, and Triumph Group are major suppliers specializing in aerostructures and composite materials. Honeywell leads in avionics and systems, while Safran USA and Rolls-Royce North America contribute to engine manufacturing. The competitive landscape is shaped by long-term contracts, M&A activities, and joint R&D initiatives aimed at achieving fuel efficiency, lightweight construction, and digital manufacturing excellence. Emerging suppliers are leveraging additive manufacturing and AI-driven process automation to strengthen their position in the aerospace value chain.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071