68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

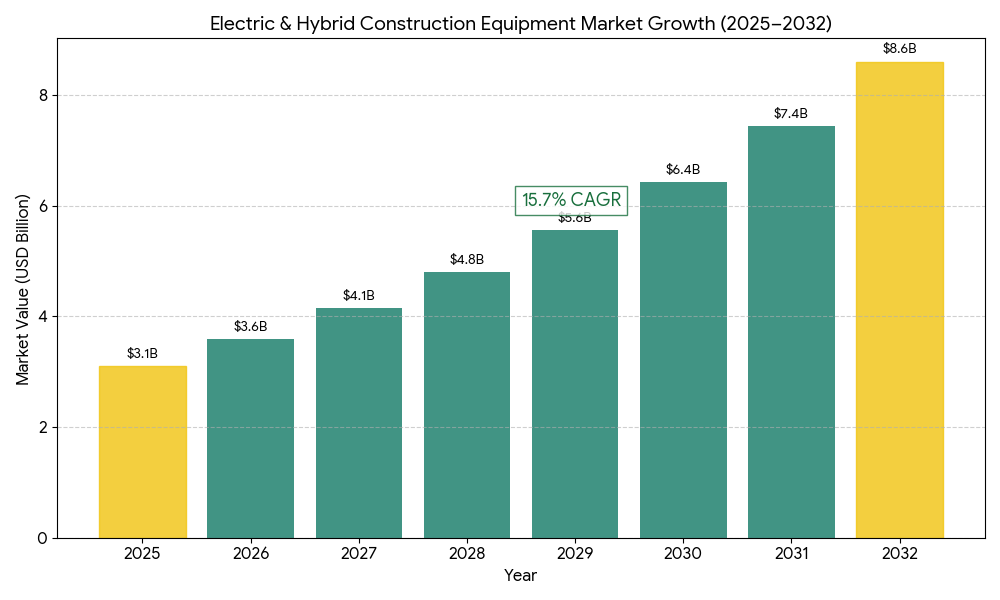

Europe Electric and Hybrid Construction Equipment Market (2026–2032): Forecasting from ~USD 3.1 Billion in 2025 to ~USD 8.6 Billion by 2032, CAGR (~15.7%)

The Europe electric and hybrid construction equipment market is projected to expand from USD 3.1 billion in 2025 to USD 8.6 billion by 2032, reflecting a 15.7% CAGR. Driven by EU emission mandates, green public procurement policies, and battery innovation, the region is accelerating adoption of electric excavators, loaders, and hybrid machinery. OEMs are rapidly transitioning fleets toward low-emission, noise-free construction solutions as governments invest in urban sustainability projects. Technological progress in lithium-ion, solid-state, and hydrogen fuel cells is improving range and charging times, while digital fleet management platforms enhance energy monitoring. With Norway, Germany, and the Netherlands leading adoption, the European market is witnessing the strongest shift toward zero-emission construction ecosystems globally.

What's Covered?

Report Summary

Key Takeaways

- Market forecast: USD 3.1B (2025) → USD 8.6B (2032), 15.7% CAGR.

- Electric excavators hold 30% of total market value in 2026.

- Electric loaders and dumpers growing fastest at 17.5% CAGR.

- Hybrid construction machines maintain 28% share due to longer runtime.

- Battery capacity improvements (25→65 kWh) extend operation by 80%.

- Public infrastructure electrification driving > 45% of regional demand.

- Germany, Norway, Netherlands = top 3 adopters.

- Charging infrastructure coverage to triple by 2030 across major metros.

- EU Fit-for-55 and Green Deal fueling fleet transition policies.

- Equipment with telemetry + energy analytics reducing idle energy by up to 40%.

Market Size & Share

The market will grow from USD 3.1 billion in 2025 to USD 8.6 billion by 2032, driven by a 15.7% CAGR. Electric excavators lead with 30% share, followed by hybrid loaders and dozers (28%). The demand for electric compact equipment is surging as cities enforce zero-emission construction zones. Public infrastructure projects including roads, bridges, and municipal redevelopment account for nearly 45% of equipment deployments. OEM alliances such as Volvo CE–Hitachi and Caterpillar–Cummins are investing in modular battery packs and hydrogen hybrid prototypes. With over €120 billion in EU Green Deal investments, the region’s construction electrification pace is outpacing North America, particularly in the Nordic and Benelux markets.

Market Analysis

Growth is underpinned by sustainability mandates, carbon-neutral fleet goals, and infrastructure renewal programs. Hybrid models remain dominant in high-load segments where range remains a limitation, while fully electric compact excavators and mini-loaders dominate in urban settings. Manufacturers are optimizing battery architecture, adopting liquid-cooled packs for thermal stability and fast-charge systems (350 kW) enabling <60-minute recharges. Digital twins and energy simulation platforms are enabling predictive maintenance and charge scheduling. Despite higher upfront costs, TCO savings reach 20–25% over 5 years due to reduced fuel and maintenance. Rental fleets are becoming early adopters, accelerating market penetration among small and medium contractors.

Trends & Insights

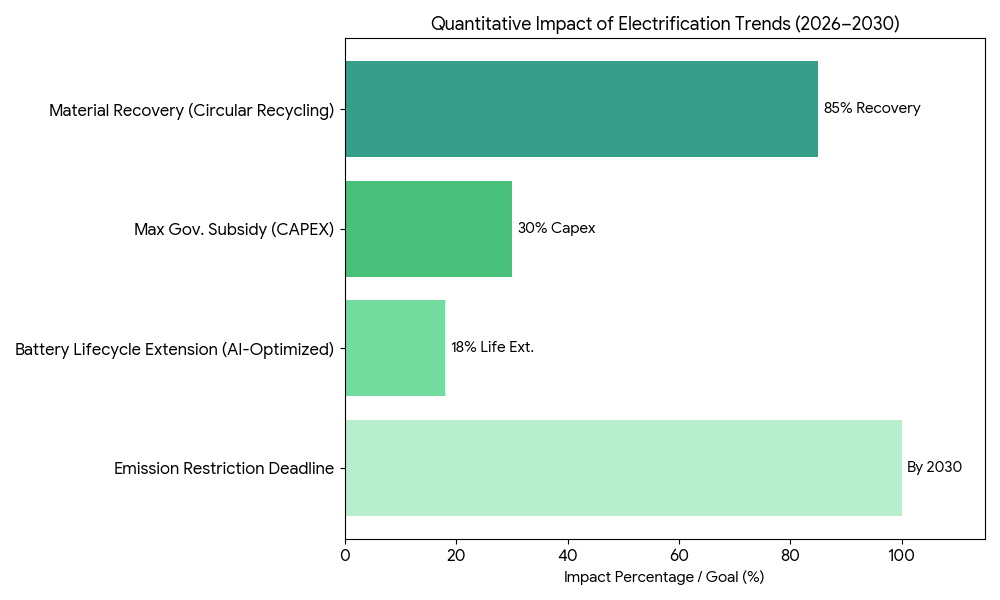

- Urban Low-Emission Zones enforcing diesel restrictions by 2030.

- Battery Swapping Depots emerging across Germany and Norway.

- AI-Optimized Energy Management extending battery lifecycle by 18%.

- OEM-Utility Partnerships (Volvo CE × Iberdrola, JCB × Shell Recharge).

- Hydrogen ICE Hybrids tested for heavy loaders and cranes.

- Circular Battery Recycling Programs recovering 85% of materials.

- Government Subsidies covering 10–30% of capex for electric fleets.

- Telematics Integration reducing downtime through predictive analytics.

- Compact Electric Equipment gaining traction for residential projects.

- Fleet Electrification as ESG KPI in contractor tenders.

Segment Analysis

By product, electric excavators lead due to strong OEM penetration and municipal fleet upgrades. Electric loaders and dumpers will expand fastest, supported by incentives for heavy-duty electrification. Hybrid cranes and dozers fill interim gaps in long-runtime operations. By powertrain, battery-electric holds 58%, hybrid diesel-electric ≈ 30%, and hydrogen fuel cell remains under 10% but growing. Telematics-enabled equipment now represents over 40% of deployed fleets. Application-wise, infrastructure (roads, bridges, utilities) leads demand, followed by residential and commercial construction, each exceeding 25% market contribution.

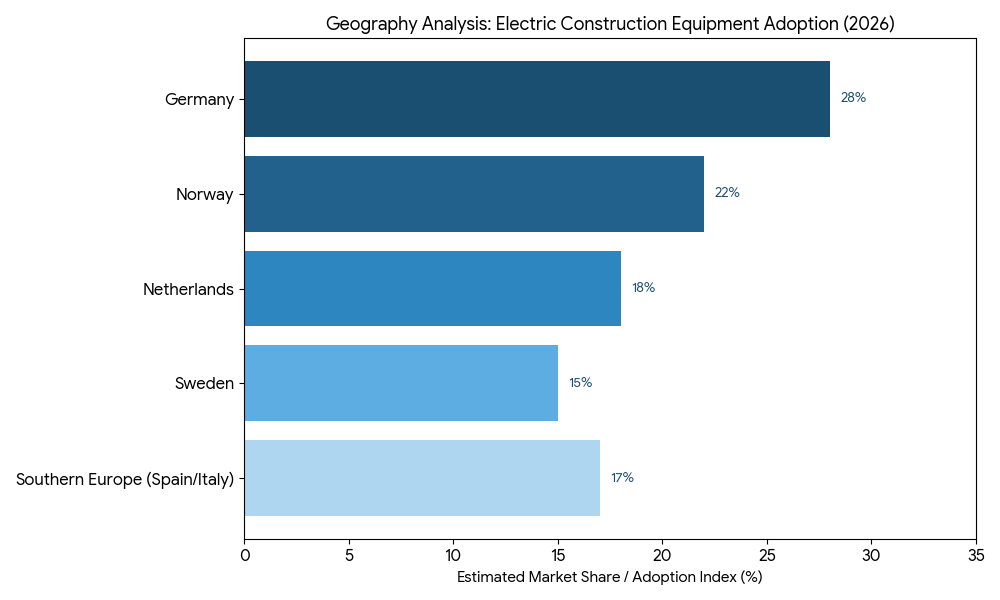

Geography Analysis

Germany leads with 28% market share, driven by strong green fleet regulations and industrial electrification policies. Norway follows as the earliest adopter of zero-emission construction equipment, with over 60% urban projects deploying electric machinery. The Netherlands and Sweden are investing heavily in battery charging depots and smart site management systems. Southern Europe (Spain, Italy) is catching up via EU recovery funds focused on carbon-neutral construction. Regional clusters around Rotterdam, Oslo, and Munich are evolving into innovation testbeds for next-gen hybrid equipment.

Competitive Landscape

Key players include Volvo Construction Equipment, Hitachi Construction Machinery, Caterpillar Inc., Komatsu Europe, JCB, and Wacker Neuson. Volvo CE leads in compact electric excavators, while Komatsu is expanding hybrid models for heavy-duty applications. Caterpillar and JCB are piloting hydrogen-fuel hybrid systems. Startups like Epiroc Electric Systems and Green Machine Equipment are pushing battery innovations. Partnerships with battery suppliers (Northvolt, LG Energy Solution) and charging providers (ABB, Shell Recharge) are shaping the ecosystem. Competitive differentiation increasingly centers on range per charge, charging speed, and total cost of ownership optimization through connected telematics platforms.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071