68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

North America Smart Manufacturing Market (2026–2034): Set to hit 345.8 Billion by 2034, CAGR (~11.9%)

The North America smart manufacturing market is projected to reach USD 345.8 billion by 2034, growing at a CAGR of 11.9% from 2026. This surge is driven by rapid industrial digitalization, adoption of Industrial IoT (IIoT), AI-driven robotics, and digital twin technologies across manufacturing sectors. U.S. and Canadian manufacturers are investing heavily in automation infrastructure, edge computing, and predictive analytics to enhance operational efficiency and supply chain resilience. Increasing government incentives under programs such as the U.S. CHIPS Act and Made in America initiative are strengthening domestic production capabilities. By 2030, over 70% of North American factories are expected to operate as smart facilities, optimizing throughput, energy consumption, and workforce safety through intelligent automation and connected ecosystems.

What's Covered?

Report Summary

Key Takeaways

- Market to reach USD 345.8B by 2034, growing at 11.9% CAGR.

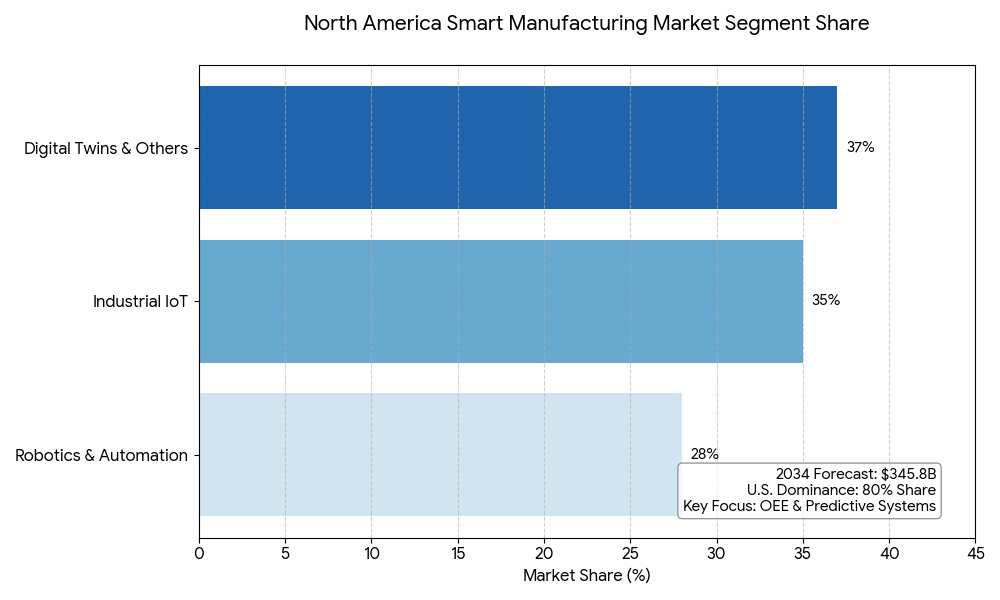

- U.S. accounts for 80% of regional market value by 2030.

- Industrial IoT (IIoT) leads with 35% market share, followed by robotics at 28%.

- AI and machine learning adoption to enhance productivity by 25–30%.

- Digital twin technology to reach USD 48B market value by 2034.

- Predictive maintenance systems cut unplanned downtime by 40%.

- Automotive and electronics industries remain top adopters.

- Energy management solutions save manufacturers 15–20% operational costs.

- 5G-enabled smart factories projected to increase fivefold by 2032.

- Cybersecurity and data governance now represent 12% of total automation spending.

Market Size & Share

The North America smart manufacturing market is on track to hit USD 345.8 billion by 2034, driven by the convergence of AI, IoT, robotics, and advanced analytics. The U.S. dominates with 80% share, underpinned by federal incentives for domestic semiconductor production, electric vehicle (EV) manufacturing, and AI-driven automation. Industrial IoT accounts for the largest market share (35%), followed by robotics and automation systems (28%), and digital twin solutions gaining rapid adoption in aerospace, automotive, and healthcare. The focus is on reducing downtime, improving OEE (Overall Equipment Effectiveness), and enabling data-driven manufacturing. The integration of sensors, cloud platforms, and edge AI has transformed traditional factories into predictive, adaptive systems capable of responding to real-time demand fluctuations.

Market Analysis

Market expansion is fueled by reshoring initiatives, energy efficiency mandates, and a growing need for supply chain resilience post-2020 disruptions. Industrial IoT networks enable seamless connectivity between machines, while AI-driven process optimization enhances throughput and product quality. Collaborative robots (cobots) are expanding production capacity across mid-sized factories, while digital twins are enabling virtual replication of assets to optimize design and lifecycle management. Cloud-to-edge integration allows real-time analytics and autonomous decision-making at scale. Cyber-physical systems (CPS) are reshaping industrial workflows, combining hardware sensors with AI logic. Investments in robotics automation and additive manufacturing are further bridging gaps between design and production agility, positioning North America as a leading global hub for Industry 4.0 innovation.

Trends & Insights

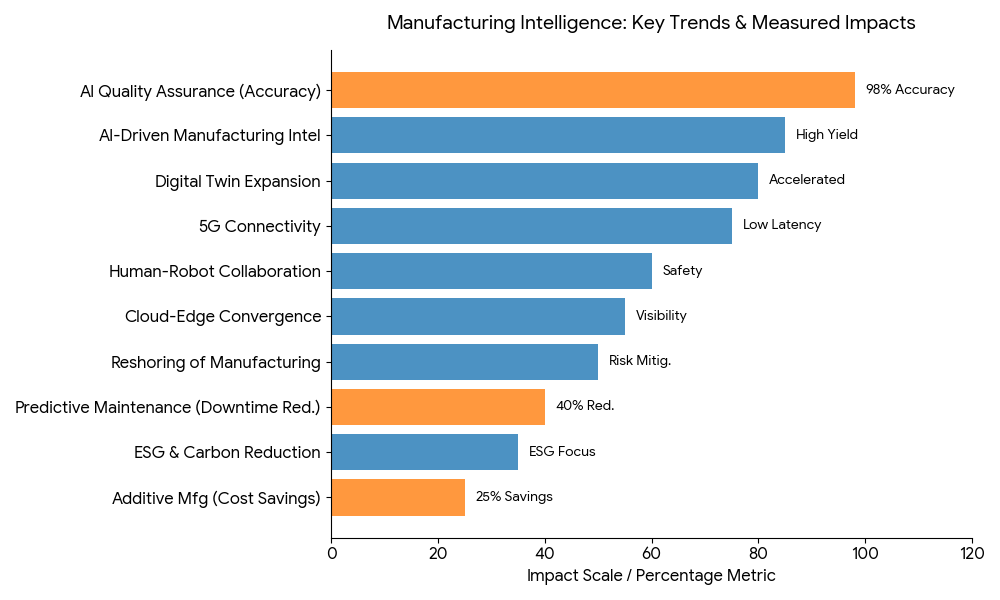

- AI-Driven Manufacturing Intelligence improving defect detection and yield optimization.

- Predictive Maintenance Adoption reducing unplanned downtime by over 40%.

- Digital Twin Expansion accelerating across EV and aerospace assembly lines.

- 5G Connectivity enabling low-latency robotic operations and edge analytics.

- Cloud-Edge Convergence improving data orchestration and production visibility.

- Additive Manufacturing Integration cutting prototyping costs by 25%.

- ESG and Energy Monitoring Platforms reducing carbon emissions across industrial parks.

- Human-Robot Collaboration (Cobots) increasing safety and precision.

- AI Quality Assurance Systems improving inspection accuracy to 98%.

- Reshoring of Critical Manufacturing driven by policy incentives and geopolitical risk mitigation.

Segment Analysis

By technology, Industrial IoT remains the foundation of smart manufacturing, connecting machinery, sensors, and control systems to cloud analytics. Robotics, particularly collaborative and mobile units, is expanding rapidly across automotive and electronics industries. Digital twins and simulation platforms are revolutionizing product lifecycle management, reducing design-to-production cycles by 30%. By industry, automotive and aerospace hold 40% of total market share, followed by electronics (20%), pharma-biotech (10%), and energy-intensive sectors. Software platforms for AI-driven process optimization and MES (Manufacturing Execution Systems) are gaining momentum due to their scalability and integration with legacy systems.

Geography Analysis

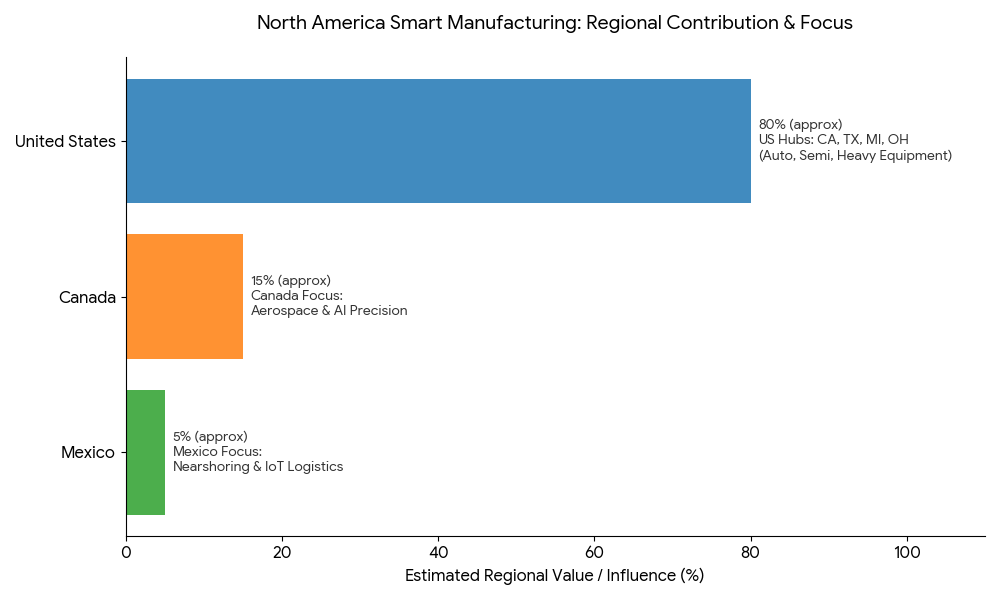

The United States leads North America’s smart manufacturing landscape, driven by automation in automotive, semiconductor, and heavy equipment industries. California, Texas, Michigan, and Ohio are the top investment hubs due to proximity to automotive supply chains and robotics R&D centers. Canada contributes ~15% of regional value, focusing on AI-powered precision manufacturing and digital twin simulation in aerospace and industrial machinery sectors. Mexico, while smaller, is seeing strong adoption of robotic assembly systems and IoT-integrated logistics due to supply chain nearshoring from Asia. Collectively, these regions are transforming into digitally synchronized manufacturing corridors.

Competitive Landscape

The market features leading technology providers and OEMs including Siemens, Rockwell Automation, Honeywell, ABB, Emerson Electric, General Electric, and Schneider Electric. Siemens and Rockwell Automation dominate IIoT and control systems, while ABB and Fanuc lead in robotics integration. Microsoft Azure and Amazon Web Services (AWS) power cloud-based manufacturing analytics, supporting interoperability across factories. Dassault Systèmes, PTC, and Autodesk are expanding digital twin platforms. Mergers and strategic partnerships—such as Siemens × NVIDIA (industrial metaverse) and Rockwell × Microsoft (connected factory analytics) are shaping the evolution of next-gen smart manufacturing ecosystems in North America.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071