68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

USA Compact Electric Construction Equipment Market (2026–2032): USD 4.86 Billion by 2032, CAGR (~15.1%) | Electric Loaders, Electric Forklifts, <2 Ton & 2–5 Ton Equipment for Urban & Sustainable Construction”

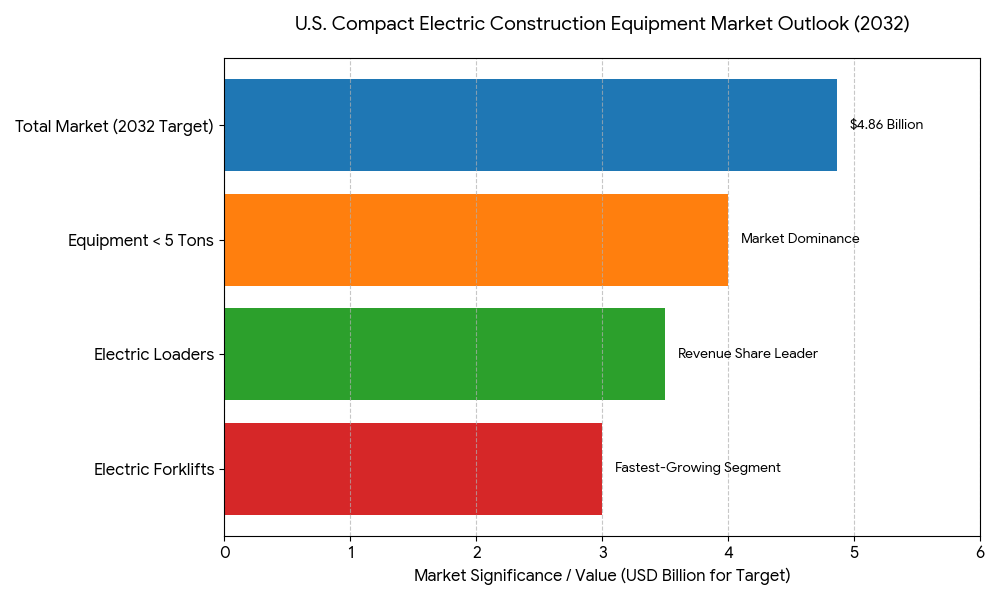

The U.S. compact electric construction equipment market is forecasted to reach USD 4.86 billion by 2032, growing at a 15.1% CAGR from 2026. The rapid adoption of electric loaders, forklifts, and compact excavators (<5 tons) is transforming urban construction, warehousing, and infrastructure maintenance. This shift is powered by federal emission reduction goals, state-level green procurement mandates, and technological innovation in battery chemistry, charging, and powertrain efficiency. Manufacturers are focusing on compact, low-noise, zero-emission machinery for urban and indoor projects, while contractors benefit from reduced fuel and maintenance costs. With growing support from the Infrastructure Investment and Jobs Act (IIJA) and DOE clean fleet programs, compact electrified construction equipment is emerging as a central pillar of the sustainable construction revolution in the U.S.

What's Covered?

Report Summary

Key Takeaways

- Market to reach USD 4.86B by 2032, expanding at 15.1% CAGR.

- Electric loaders and forklifts account for 52% of total market share.

- Equipment under 5 tons represents 65% of U.S. demand by volume.

- Lithium-ion batteries dominate with 80% share, replacing lead-acid systems.

- Average battery runtime improved by 40% (6 → 8.5 hours) from 2025–2032.

- Urban infrastructure projects drive 55% of compact electric machinery deployment.

- Fleet electrification grants under IIJA supporting SME contractor adoption.

- Electric forklifts growing fastest at 17% CAGR, driven by logistics automation.

- Charging infrastructure installations up 3.5× since 2024 across major U.S. metros.

- Contractors achieve 20–25% TCO reduction through maintenance savings.

Market Size & Share

The U.S. compact electric construction equipment market is expected to hit USD 4.86 billion by 2032, driven by urban infrastructure renewal, logistics facility construction, and indoor maintenance projects. Equipment below 5 tons dominates due to its versatility and maneuverability in dense city environments. Electric loaders hold the largest revenue share, while electric forklifts are the fastest-growing due to rapid e-commerce expansion and warehouse automation. Federal incentives for clean fleet conversion and California’s zero-emission construction mandate are propelling nationwide adoption. Contractors are investing in compact, telematics-enabled machinery that enhances uptime, optimizes power usage, and reduces carbon footprint. The convergence of sustainability targets and technology innovation positions the U.S. as one of the most dynamic global markets for compact electric equipment.

Market Analysis

The shift toward electric compact machinery is a response to rising fuel prices, tightening emission regulations, and demand for low-noise, energy-efficient construction tools. Manufacturers such as Bobcat, Volvo CE, Caterpillar, and JCB are expanding their electric loader, mini-excavator, and forklift lines with improved battery density and fast-charging capabilities. Average runtime has risen by 40%, while TCO reductions of up to 25% make electrification economically viable for contractors. Lithium-ion and LFP batteries dominate, while solid-state prototypes are under development. Digital fleet management and energy telematics systems are enabling operators to track energy consumption, optimize charge cycles, and prevent idle losses. Rental fleets are seeing rapid electrification as smaller contractors opt for short-term use without capital overhead.

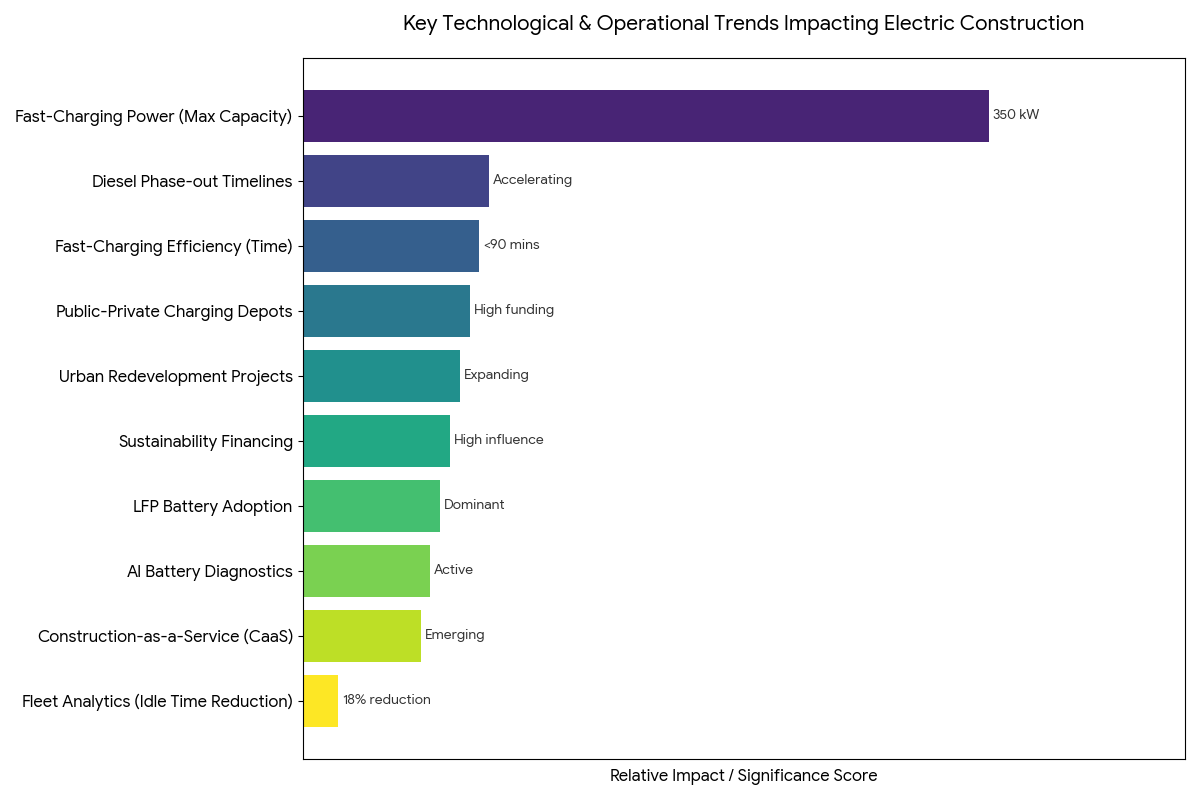

Trends & Insights

- Diesel phase-out timelines in major U.S. states accelerating electric shift.

- Telematics-driven optimization enabling real-time power monitoring.

- Compact excavators and loaders expanding into urban redevelopment projects.

- Public-private partnerships funding job-site charging depots.

- Fast-charging (250–350 kW) reducing downtime to under 90 minutes.

- LFP battery dominance ensuring longer cycle life and thermal safety.

- Fleet analytics platforms cutting idle time by up to 18%.

- Construction-as-a-Service (CaaS) models emerging for electrified fleets.

- OEMs integrating AI diagnostics to enhance battery performance.

- Sustainability-linked financing influencing purchase decisions.

Segment Analysis

By tonnage, the <2 ton segment serves indoor operations and confined spaces, representing 40% of unit volume, while 2–5 ton machines dominate outdoor and medium-load projects. Electric forklifts and loaders contribute more than half of total market revenue, driven by warehouse construction and distribution logistics expansion. The lithium-ion battery segment accounts for 80% share, followed by LFP variants gaining traction for high-heat environments. Urban infrastructure projects, including sidewalk reconstruction, public transit maintenance, and airport expansion, account for 55% of market demand. The rental segment is projected to grow 1.8× by 2032, supporting SMEs in transitioning toward low-emission operations.

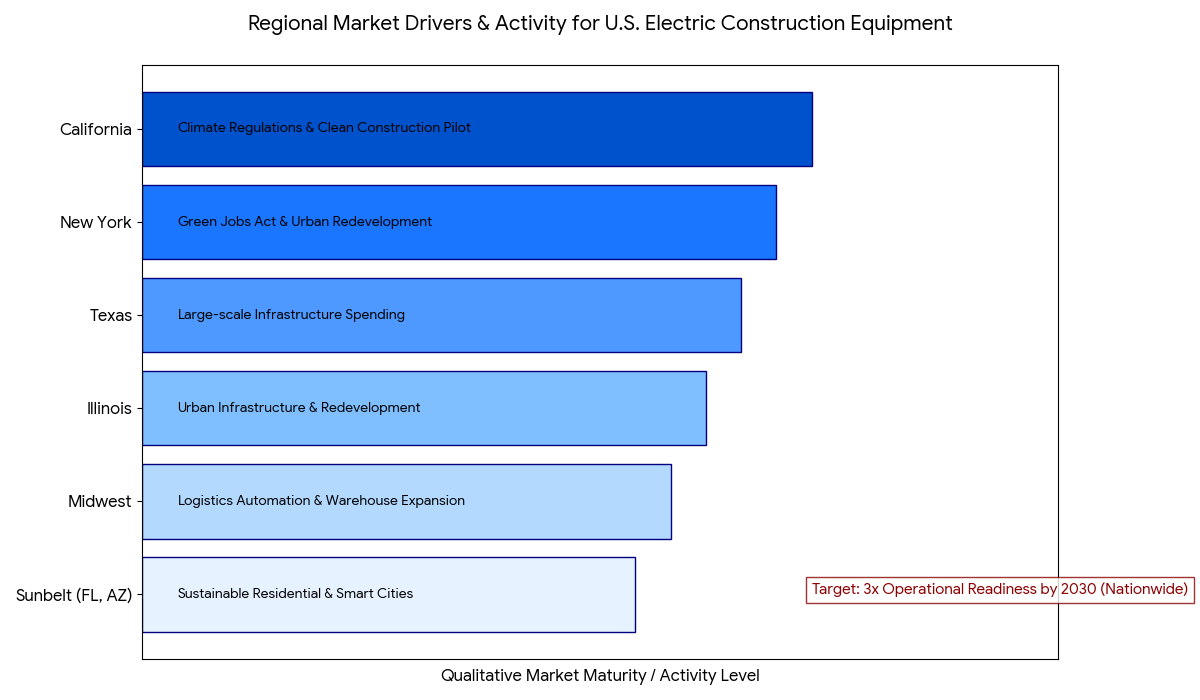

Geography Analysis

California, Texas, New York, and Illinois dominate due to infrastructure spending, climate regulations, and urban redevelopment initiatives. California’s Clean Construction Pilot and New York’s Green Jobs Act are key regulatory enablers. Midwestern states are emerging as logistics automation hubs, fueling demand for electric forklifts and mini loaders in warehouse construction. Sunbelt regions such as Florida and Arizona are adopting compact electric machinery for sustainable residential projects and smart city developments. The nationwide build-out of fast-charging and mobile battery stations is expected to triple operational readiness by 2030.

Competitive Landscape

Key industry players include Bobcat, Volvo Construction Equipment, Caterpillar, JCB, Komatsu, Takeuchi, and Wacker Neuson. Bobcat leads the market with its E10e and T7X fully electric models, while Volvo CE is expanding its compact electric line in partnership with Northvolt. Caterpillar focuses on hybridized systems with scalable battery packs, while JCB invests in hydrogen-electric solutions. Rental companies like United Rentals and Sunbelt Rentals are scaling their electric equipment fleets to support the growing urban market. Strategic partnerships between OEMs, utilities, and tech providers are improving charging availability and fleet interoperability, solidifying the U.S. as a pioneer in compact, zero-emission construction machinery.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071