68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

North America Robotic Lawn Mowers Market (2026–2033): Forecasting from ~USD 1.05 Billion in 2025 to ~USD 3.05 Billion by 2033, CAGR (~14.3%) | Smart Lawn Care, Autonomous Mowing, Residential & Commercial Landscaping

The North America robotic lawn mowers market is forecasted to grow from USD 1.05 billion in 2025 to USD 3.05 billion by 2033, registering a CAGR of 14.3%. The surge is driven by the rising adoption of smart home technologies, growing demand for automated lawn maintenance, and advancements in AI navigation and battery efficiency. Residential and commercial property owners are investing in low-maintenance, noise-free, and emission-free mowing solutions. Enhanced GPS mapping, LiDAR, and sensor-based obstacle detection are expanding usability across larger and complex lawns. Additionally, labor shortages in landscaping and a focus on sustainability are accelerating market uptake. The region’s growing network of smart home integrations (Alexa, Google Home, Apple HomeKit) positions North America as a global leader in autonomous lawn care innovation.

What's Covered?

Report Summary

Key Takeaways

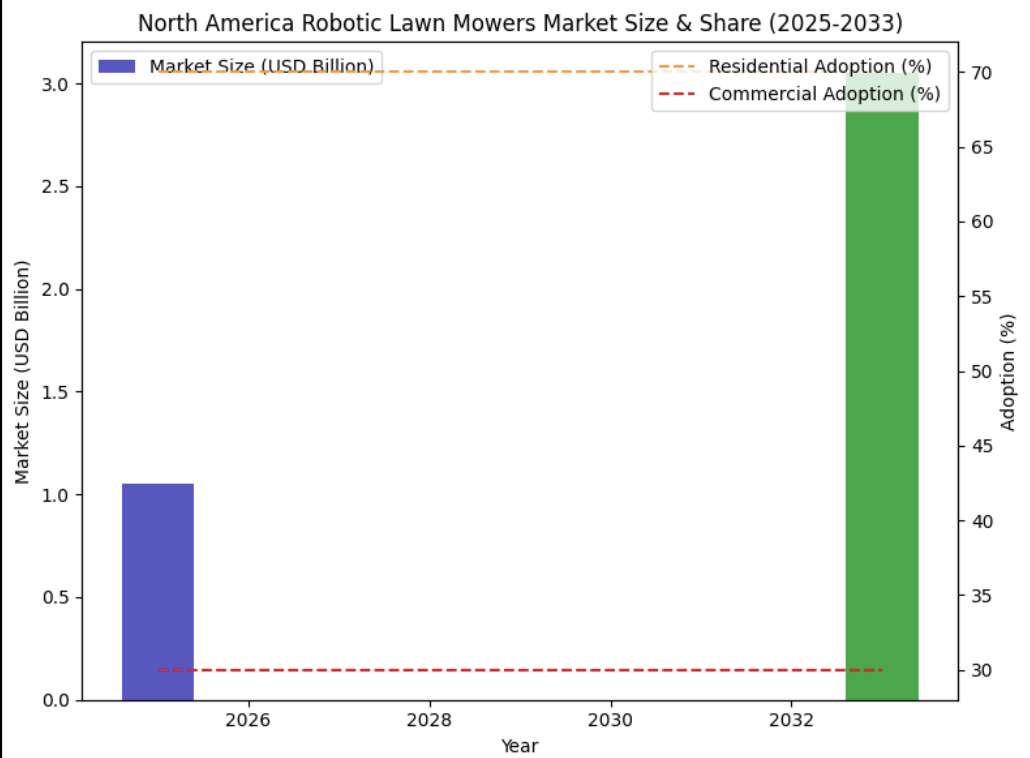

- Market to grow from USD 1.05B (2025) to USD 3.05B (2033) at a 14.3% CAGR.

- Residential segment dominates with 70% share, followed by commercial landscaping at 30%.

- AI-powered navigation improving mowing efficiency by 35%.

- Battery life enhancements (2.5 → 4 hours) extend coverage area by 60%.

- Connectivity integration (Wi-Fi, Bluetooth, 4G) in over 80% of models by 2030.

- Americans spend USD 105B annually on lawn care, creating massive automation potential.

- Labor shortages pushing commercial landscapers toward autonomous solutions.

- Eco-friendly electric mowers reducing CO₂ emissions by >50% compared to gas models.

- GPS + LiDAR-enabled mowers achieving 98% accuracy in path optimization.

- U.S. and Canada together account for over 90% of regional demand.

Market Size & Share

The North America robotic lawn mowers market will triple from USD 1.05 billion (2025) to USD 3.05 billion (2033), marking a 14.3% CAGR. Residential adoption (70%) leads growth, driven by time-saving convenience and sustainability goals. Commercial landscaping—covering golf courses, parks, and campuses—accounts for 30% but shows higher ROI due to reduced labor costs. Battery-powered models are displacing traditional gas mowers amid emission regulations and energy cost concerns. AI and GPS integration enable precision mowing patterns, reducing energy consumption by 20–25%. With electricity costs stable and labor expenses rising, robotic solutions are becoming mainstream in the U.S. E-commerce distribution is accelerating growth, with Amazon and Home Depot dominating online sales channels.

Market Analysis

The market’s acceleration is fueled by the convergence of automation, sustainability, and digital connectivity. Manufacturers like Husqvarna, Worx, Robomow, and Greenworks are integrating AI-based obstacle detection, vision sensors, and autonomous route mapping to enhance efficiency. Battery technology advancements, including lithium-ion and LFP cells, are improving run time and charging cycles. Smart connectivity via Wi-Fi, 4G, and app-based control enables users to schedule, monitor, and geo-fence mowing zones remotely. The rise in urban smart homes and suburban landscaping trends is expanding demand across mid- to high-income households. Commercial property managers are investing in fleets of mowers equipped with cloud-based dashboards for multi-property maintenance optimization.

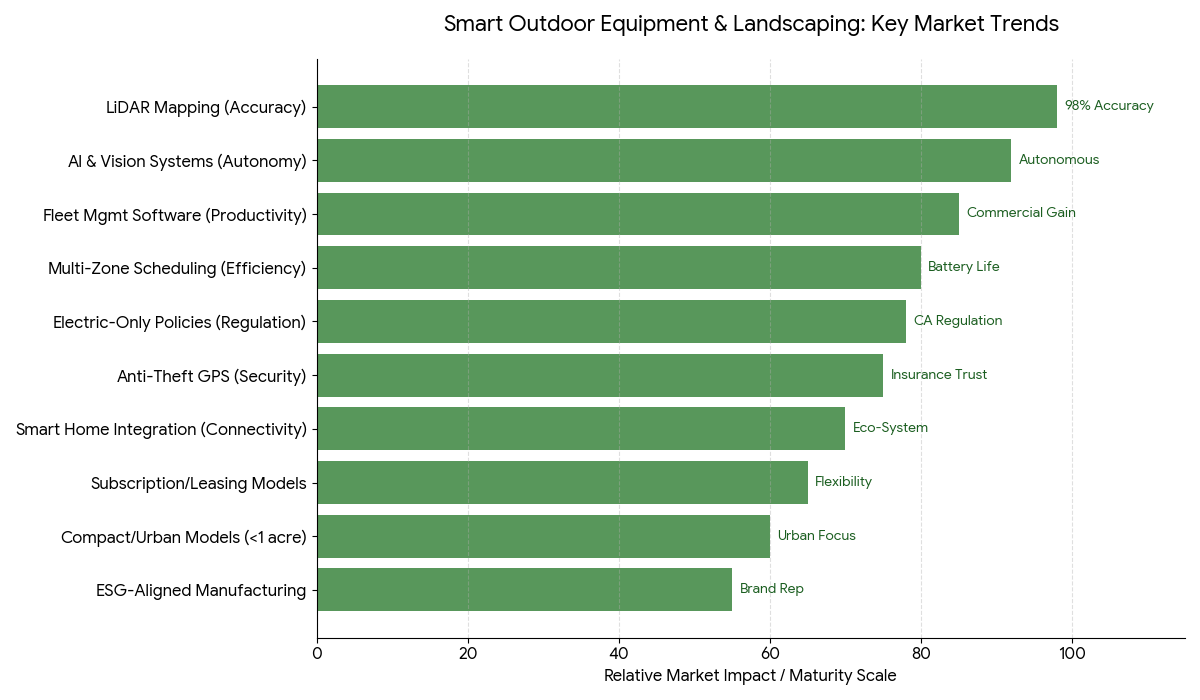

Trends & Insights

- AI & Vision-Based Systems enabling autonomous operation in complex terrains.

- LiDAR Mapping improving navigation accuracy to 98%.

- Electric-Only Equipment Policies gaining traction in U.S. states like California.

- Subscription & Leasing Models emerging for homeowners and landscapers.

- Smart Home Integration through Alexa, Google Home, and Apple ecosystems.

- Multi-Zone Scheduling reducing overlap and extending battery efficiency.

- Anti-Theft GPS Features increasing consumer trust and insurance coverage.

- Compact & Lightweight Models designed for small urban yards (<1 acre).

- Fleet Management Software enhancing commercial landscaping productivity.

- ESG-Aligned Manufacturing influencing brand reputation and adoption.

Segment Analysis

By product type, electric autonomous mowers lead with 65% market share, followed by hybrid solar-assisted models at 20%. By end user, residential households dominate due to ease of use and availability of connected smart systems. The commercial segment is forecasted to grow at 16% CAGR, driven by landscaping service providers and facility managers. AI-based high-end mowers with GPS and obstacle detection capabilities will account for over 70% of total revenue by 2033. In terms of distribution, online channels (e-commerce platforms) are expected to represent 55% of total sales by 2030, while retail dealerships remain relevant in rural and suburban markets.

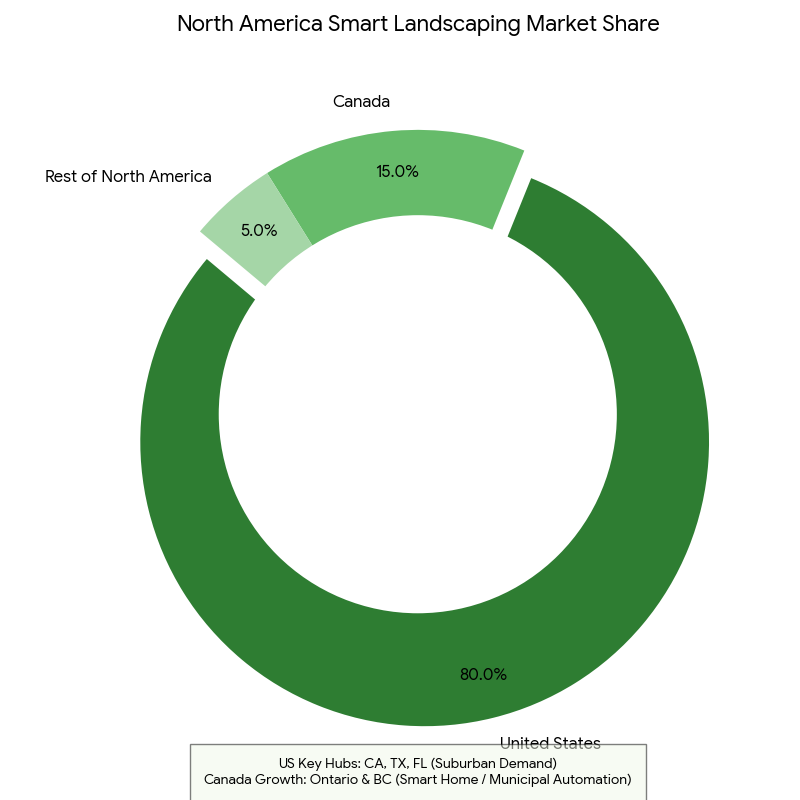

Geography Analysis

The United States dominates with 80% of the North American market, supported by large suburban housing stock and a high proportion of detached homes with lawns. California, Texas, and Florida are key demand hubs due to their extensive landscaping and environmental policy support. Canada follows with strong growth in smart home adoption and municipal automation programs in provinces like Ontario and British Columbia. Increasing energy efficiency mandates and consumer awareness of sustainable landscaping are aligning with regional policy incentives for electric equipment adoption.

Competitive Landscape

The market features leading players such as Husqvarna Group, Worx (Positec), Robomow (MTD Products), Greenworks Tools, Honda, Stiga Group, and Ego Power+. Husqvarna leads with its Automower® series, offering advanced AI navigation and connectivity integration. Worx and Robomow dominate the mid-tier consumer segment with smart app control and affordability. Greenworks and Ego Power+ are gaining ground with wire-free, GPS-based mowers for compact lawns. Honda and Stiga are expanding their commercial-grade offerings with fleet connectivity and solar-charging prototypes. Strategic trends include collaborations with home automation platforms, OEM partnerships for AI chip integration, and expansion of subscription-based maintenance programs targeting recurring revenue streams.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071