68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Europe Drill Rods Market (2026–2032): Forecasting from ~USD 1.18 Billion in 2026 to ~USD 2.80 Billion by 2032, CAGR (~5.5%) — Mining, Construction, Quarrying, Oil & Gas Drilling Applications

The Europe drill rods market is projected to grow from USD 1.18 billion in 2026 to USD 2.80 billion by 2032, registering a CAGR of 5.5%. The growth is driven by expanding mining and construction activity, the revival of oil and gas exploration projects, and technological innovations in drill rod materials and design. Increasing demand for deep drilling operations in geothermal, hydrocarbon, and mineral exploration is also supporting market expansion. High-strength steel alloys, friction-welded rods, and thread connection enhancements are improving durability and performance, reducing downtime in operations. Countries such as Germany, Sweden, and Poland are leading contributors, given their strong mining infrastructure and quarrying activity. Furthermore, the push for energy independence in Europe and infrastructure modernization programs are sustaining long-term demand for drill rods across both industrial and energy applications.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 1.18B (2026) to USD 2.80B (2032) at 5.5% CAGR.

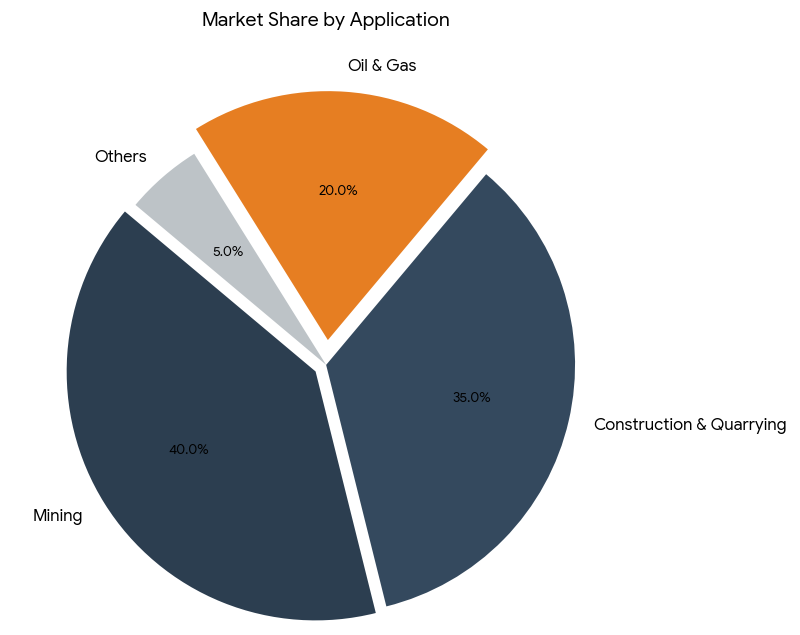

- Mining applications account for 40% of total drill rod demand.

- Construction and quarrying segments combined contribute 35% of market revenue.

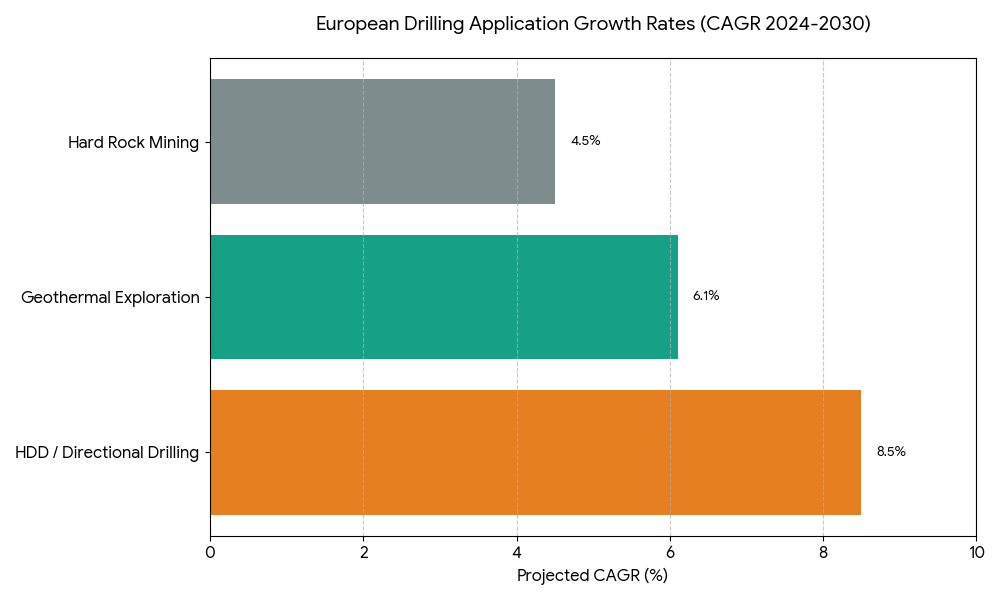

- Oil & gas drilling to grow at 6.2% CAGR due to deep well expansion projects.

- Germany, Sweden, and Poland collectively hold 50% of the regional market.

- Friction-welded and seamless steel rods dominate with 60% market share.

- Carbon steel and alloy steel rods remain most preferred for hard rock drilling.

- Automation and mechanization in mining driving demand for precision-engineered rods.

- The geothermal energy sector will witness rising consumption due to deep-well drilling initiatives.

- R&D investment in lightweight, high-tensile materials improving energy efficiency and tool life.

Market Size & Share

The Europe drill rods market will grow from USD 1.18 billion in 2026 to USD 2.80 billion by 2032, maintaining a 5.5% CAGR. Mining will account for 40% of total demand, driven by increased exploration of metallic and non-metallic minerals in regions such as Sweden, Poland, and Finland. The construction and quarrying sectors, contributing 35%, are being supported by large-scale infrastructure development and civil engineering projects. Oil & gas drilling will record the highest growth at 6.2% CAGR, supported by deep-well drilling in the North Sea and Eastern Europe. The use of high-grade steel alloys, coupled with precision threading and heat treatment processes, is improving rod longevity and torque capacity, resulting in higher operational efficiency.

Market Analysis

The European drill rod market is evolving rapidly due to industrial modernization and the energy transition movement. With Europe prioritizing domestic resource extraction and energy security, demand for robust and efficient drilling equipment is rising. Friction-welded rods dominate, offering superior tensile strength and joint integrity. The shift toward automation in mining operations is leading to higher precision requirements and consistent performance under extreme drilling conditions. Alloy and carbon steel rods remain the preferred materials for hard rock drilling, while composite materials are gaining traction for geothermal and directional drilling applications. Additionally, aftermarket services and maintenance programs are contributing to overall market expansion, as end users prioritize equipment reliability and cost optimization.

Trends & Insights

- Green Mining Initiatives: European nations are adopting sustainable mining techniques, driving innovation in eco-friendly and recyclable drill materials.

- Geothermal Expansion: Rising focus on renewable geothermal energy is boosting deep drilling requirements across Germany and Iceland.

- Material Innovation: Titanium-blended steel alloys offering 20% higher strength are being adopted for hard rock applications.

- Automation Integration: Use of robotic drilling systems increasing precision and reducing human intervention.

- Oil & Gas Resurgence: Post-2025 rebound in exploration projects in the North Sea driving new demand for high-torque rods.

- Maintenance Efficiency: Smart sensors embedded in rods enabling real-time wear monitoring.

- 3D-Printed Connectors: Additive manufacturing improving threading accuracy and joint performance.

- Supply Chain Localization: European manufacturers increasing local production to reduce dependency on Asian imports.

- Sustainability Regulations: EU green compliance policies promoting eco-lubricants and low-emission drilling systems.

- OEM Partnerships: Collaboration between drill rig OEMs and rod manufacturers streamlining equipment compatibility.

Segment Analysis

The market is segmented by application, material, and design type. Mining dominates with 40% market share, followed by construction and quarrying at 35%, where urban development projects are increasing the use of surface drilling equipment. Oil & gas accounts for 20%, growing fastest at 6.2% CAGR, driven by increased onshore and offshore drilling. By material, carbon and alloy steels dominate with 70% share, while stainless and titanium-based rods are emerging for specialized geothermal projects. Friction-welded rods remain the standard due to high torque resistance, while seamless steel rods are gaining popularity for deep directional drilling operations.

Geography Analysis

Germany leads the European market, followed by Sweden, Poland, and Norway, which together represent 50% of regional demand. Germany’s mining and construction sectors, coupled with sophisticated engineering capabilities, make it a key producer and consumer of drill rods. Sweden and Finland are driven by metallic ore mining, while Poland’s coal and limestone mining industries ensure steady demand. Eastern Europe is emerging as a new hub for oil and gas exploration, with offshore drilling projects in the Baltic Sea further boosting demand. The Nordic countries are investing in geothermal drilling infrastructure, enhancing market diversity.

Competitive Landscape

The Europe drill rods market is moderately consolidated, with major players such as Sandvik AB, Boart Longyear, Atlas Copco, Epiroc AB, and DATC Group dominating. Sandvik leads in friction-welded rods for mining and quarrying, while Boart Longyear focuses on precision-threaded rods for exploration drilling. Atlas Copco and Epiroc are expanding portfolios through automation and IoT-integrated drilling tools. Emerging players are leveraging 3D printing and material R&D to offer lightweight, corrosion-resistant rods for niche geothermal and construction projects. Partnerships between drilling contractors, OEMs, and material science firms are reshaping the competitive ecosystem, emphasizing performance reliability, durability, and sustainability

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071