68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

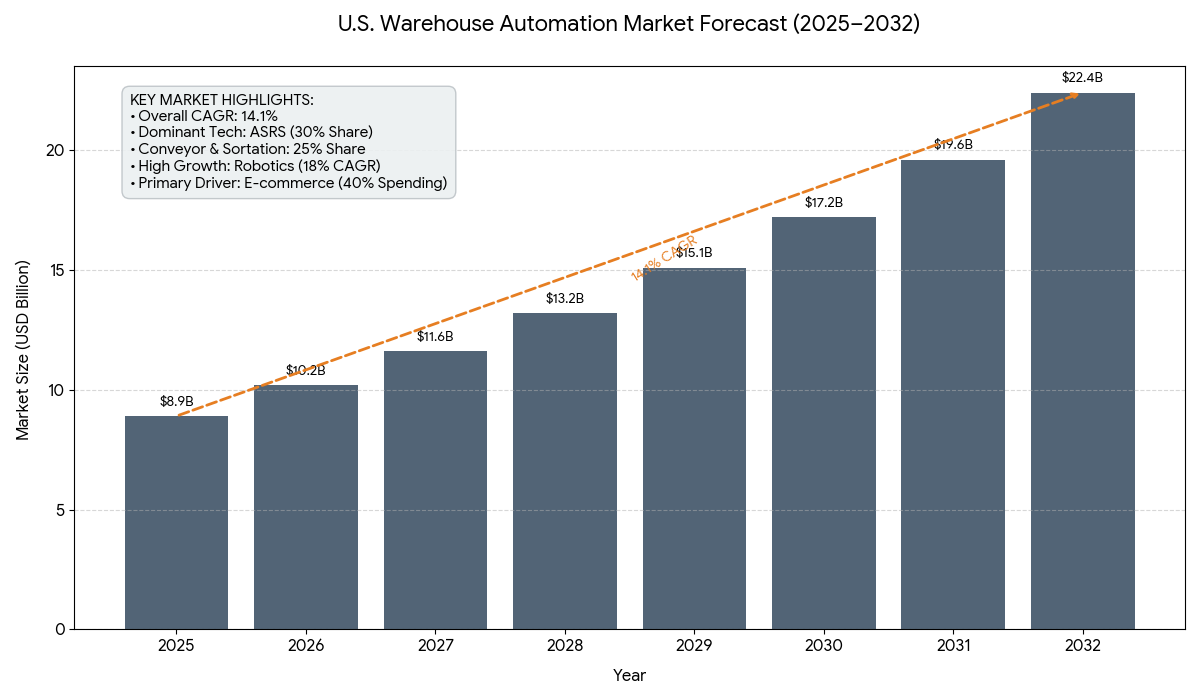

USA Warehouse Automation Market (2026–2032): Forecasting from ~USD 8.9 Billion in 2025 to ~USD 22.4 Billion by 2032, CAGR (~14.1%)

The U.S. warehouse automation market is projected to grow from USD 8.9 billion in 2025 to USD 22.4 billion by 2032, registering an impressive CAGR of 14.1%. This surge is driven by the rapid expansion of e-commerce, labor shortages, and the increasing need for operational efficiency in logistics and fulfillment centers. Key technologies such as Automated Storage and Retrieval Systems (ASRS), autonomous mobile robots (AMRs), conveyor systems, and Warehouse Management Systems (WMS) are transforming warehouse operations. Companies are prioritizing speed, accuracy, and scalability, adopting AI, IoT, and digital twin technologies to optimize throughput. The trend toward micro-fulfillment centers and last-mile automation is also accelerating market adoption. Additionally, U.S. supply chain resilience strategies are encouraging firms to reshore operations and invest in smart warehouse solutions.

What's Covered?

Report Summary

Key Takeaways

- Market projected to grow from USD 8.9B (2025) to USD 22.4B (2032) at 14.1% CAGR.

- E-commerce fulfillment centers account for 40% of total automation demand.

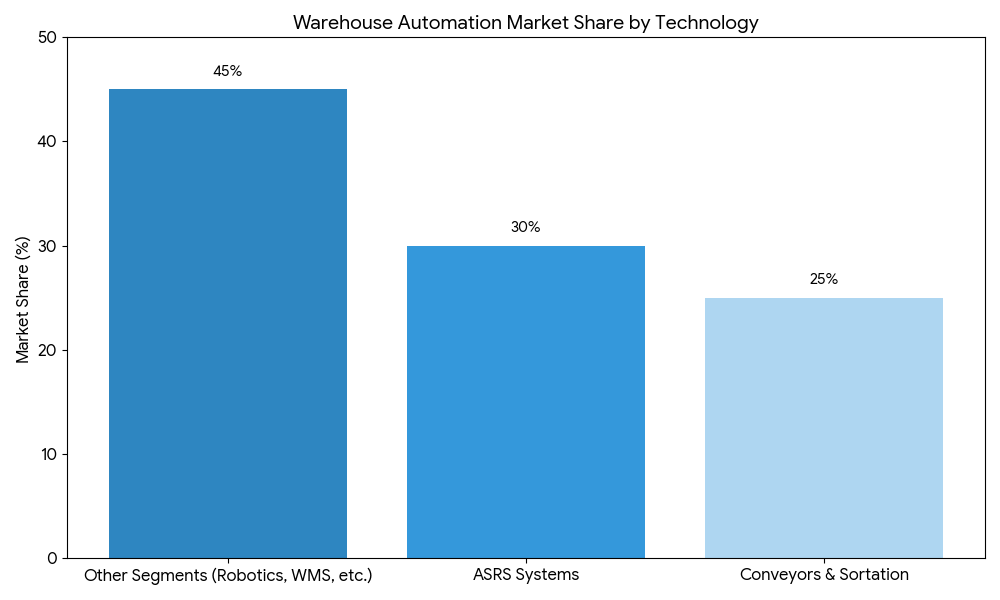

- Automated Storage & Retrieval Systems (ASRS) represent 30% of total market share.

- Warehouse robotics (AMRs & AGVs) growing fastest at 18% CAGR.

- Conveyor and sortation systems make up 25% of warehouse automation revenue.

- Warehouse Management Systems (WMS) adoption increasing at 12% CAGR due to digital transformation.

- Labor shortages driving 60% of automation investments in 2025–2030.

- Retail and 3PL sectors are leading adopters, followed by grocery and pharma logistics.

- Micro-fulfillment and dark warehouse models gaining traction in urban areas.

- AI-powered predictive analytics expected to cut warehouse downtime by 25%.

Market Size & Share

The U.S. warehouse automation market is projected to grow from USD 8.9 billion in 2025 to USD 22.4 billion by 2032, achieving a 14.1% CAGR. E-commerce fulfillment centers remain the primary demand drivers, contributing 40% of total automation spending, followed by retail and third-party logistics (3PL) sectors. ASRS systems dominate with 30% market share, enabling high-density storage and faster retrieval. Robotics, including AMRs and AGVs, are growing at 18% CAGR due to flexibility and scalability benefits. Conveyor and sortation systems account for 25% of total installations, while Warehouse Management Systems (WMS) adoption is expanding at 12% CAGR. The industry’s shift toward micro-fulfillment centers, driven by consumer demand for same-day delivery, will further amplify market growth.

Market Analysis

The market’s acceleration is underpinned by logistics digitization, labor challenges, and consumer expectations for rapid delivery. The e-commerce boom has made warehouse throughput optimization critical, leading to heavy investment in ASRS and robotic picking systems. Autonomous mobile robots (AMRs) are increasingly integrated for dynamic task allocation and inventory movement, reducing human dependency. Artificial intelligence and machine learning embedded in WMS platforms are enabling predictive maintenance, real-time routing, and automated decision-making. Retailers and 3PL operators are modernizing facilities to accommodate SKU complexity, while grocery and pharmaceutical logistics sectors are focusing on temperature-controlled automation. The growing focus on energy-efficient operations and warehouse sustainability is also fostering adoption of green robotics and solar-integrated systems.

Trends & Insights

- E-Commerce Acceleration: Rising online shopping volumes driving large-scale automation in fulfillment centers.

- Robotics Revolution: Increasing deployment of AMRs, AGVs, and AI-enabled robotic arms for order picking.

- Micro-Fulfillment Growth: Urban warehouses adopting compact automation solutions for faster order cycles.

- WMS Integration: Seamless connectivity between ERP, IoT sensors, and warehouse control systems.

- AI & Predictive Analytics: Enhancing workflow orchestration and reducing unplanned downtime by 25%.

- Sustainability Initiatives: Energy-efficient conveyors and solar-powered AMRs supporting ESG mandates.

- Human-Robot Collaboration: Safety-certified cobots enhancing speed while maintaining operational safety.

- Labor Gap Mitigation: Automation bridging the workforce shortage in peak season logistics.

- Reshoring Logistics: U.S. companies investing in domestic warehousing capacity for supply chain resilience.

- Cyber-Physical Systems: Integration of digital twins and cloud-based WMS improving asset tracking accuracy.

Segment Analysis

By technology, ASRS systems lead with 30% market share, supporting dense storage and precision retrieval. Warehouse robotics—including AMRs, AGVs, and picking robots are the fastest-growing segment at 18% CAGR, driven by operational flexibility and reduced downtime. Conveyors and sortation systems remain essential for bulk material movement, accounting for 25% of market revenue. The WMS software segment is expected to see 12% CAGR, as integration with AI and IoT becomes standard. By application, e-commerce and 3PL logistics dominate, followed by grocery, pharmaceutical, and manufacturing warehouses. The micro-fulfillment and cold storage automation segments are emerging as high-growth opportunities as omnichannel retailing expands.

Geography Analysis

Within the United States, California, Texas, Illinois, and Pennsylvania are the leading hubs for warehouse automation investments, driven by proximity to major logistics corridors and retail distribution networks. Midwestern states are seeing a surge in automated cold storage and food logistics, while southern regions such as Georgia and Florida are expanding port-linked fulfillment centers. The West Coast leads in robotics integration, given the concentration of tech-driven e-commerce companies. Meanwhile, Amazon, Walmart, and Target are setting industry benchmarks with fully automated facilities integrating AI-based sorting and real-time analytics for predictive inventory planning.

Competitive Landscape

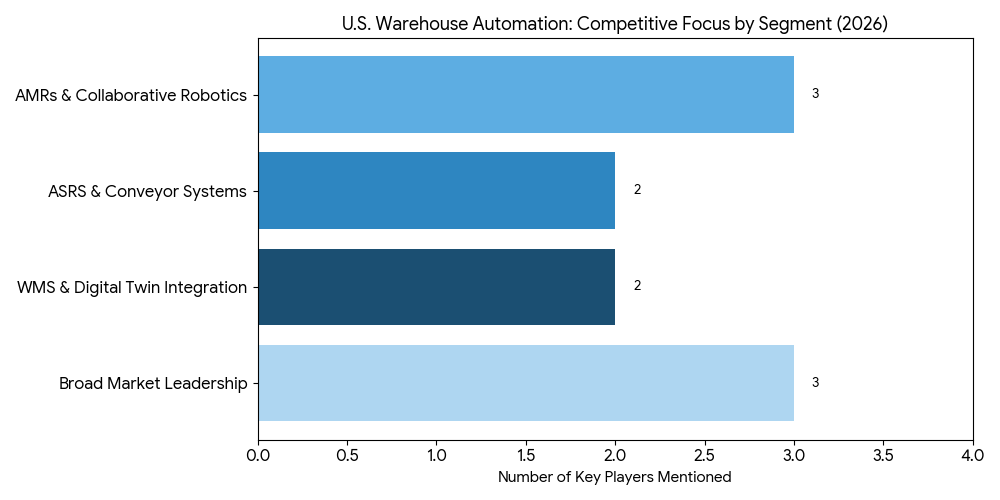

The U.S. warehouse automation market is highly competitive, with key players including Honeywell Intelligrated, Dematic, Daifuku Co., Swisslog (KUKA Group), GreyOrange, Zebra Technologies, and ABB Robotics. Honeywell and Dematic lead in ASRS and conveyor systems, while GreyOrange, Locus Robotics, and 6 River Systems are innovating in AMRs and collaborative robotics. Zebra Technologies and Manhattan Associates are pioneers in WMS and digital twin integration, focusing on AI-driven workflow optimization. Strategic partnerships between logistics providers, automation OEMs, and software developers are defining market competitiveness, while private equity investment continues to accelerate consolidation across the robotics ecosystem.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071