68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

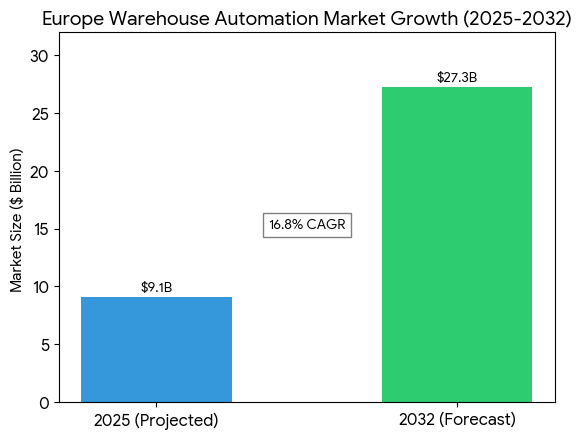

Europe Warehouse Automation Market (2026–2032): Forecasting from ~USD 9.1 Billion in 2025 to ~USD 27.3 Billion by 2032, CAGR (~16.8%) | Automated Storage, Robotics, WMS, AI-driven Solutions, E-commerce & Logistics

The Europe warehouse automation market is expected to grow significantly, from USD 9.1 billion in 2025 to USD 27.3 billion by 2032, at a CAGR of 16.8%. This growth is driven by the increasing adoption of automated storage solutions, robotics, and AI-driven warehouse management systems (WMS), particularly within the e-commerce and logistics sectors. As businesses strive to meet growing demand for faster order fulfillment and inventory management, automation is seen as a key enabler of operational efficiency. Robots, automated conveyors, and AI-powered solutions are being integrated into warehouses to enhance throughput, reduce labor costs, and improve supply chain resilience. E-commerce giants and third-party logistics (3PL) providers are leading the adoption, while smaller enterprises are increasingly following suit as automation becomes more affordable and accessible. The integration of IoT-enabled sensors and data analytics further boosts the intelligence of automated systems, leading to smarter operations and predictive decision-making.

What's Covered?

Report Summary

Key Takeaways

- Market projected to grow from USD 9.1B (2025) to USD 27.3B (2032), 16.8% CAGR.

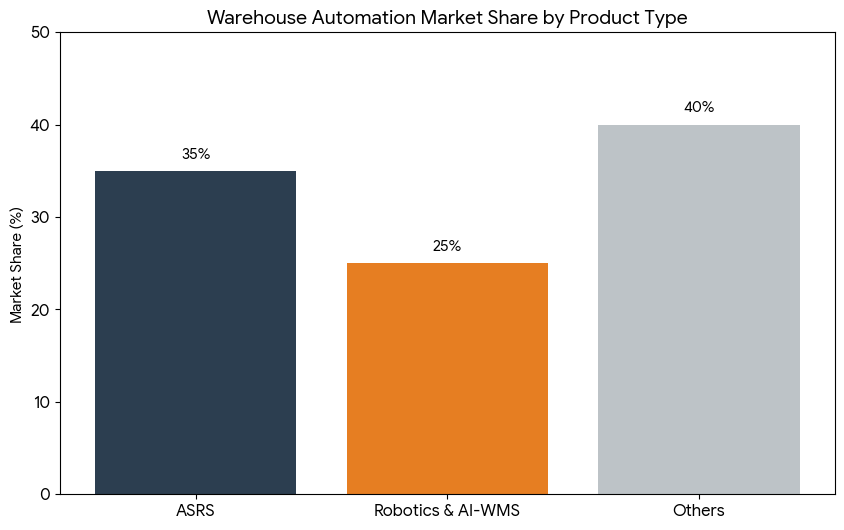

- Automated storage and retrieval systems (ASRS) lead, comprising 35% of market share.

- Robotics adoption will grow at 18% CAGR, especially in e-commerce fulfillment centers.

- AI-driven WMS solutions contributing to 20% cost reduction in warehouse operations.

- E-commerce and logistics sectors represent 70% of total market demand.

- AI-powered data analytics improving inventory accuracy by up to 30%.

- Automated guided vehicles (AGVs) and drones are expected to grow by 14% CAGR.

- Warehouse leasing models incorporating automation will reduce operational costs by 25%.

- Robotics reducing labor dependency by 40% in distribution centers.

- EU sustainability regulations driving demand for energy-efficient automated solutions.

Market Size & Share

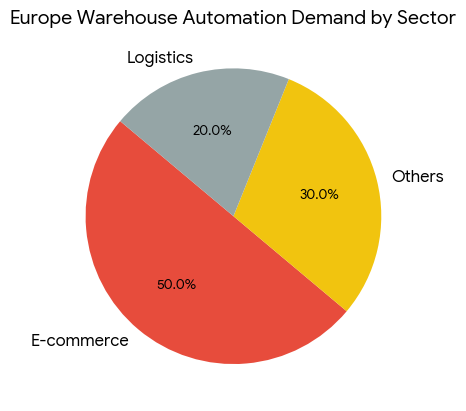

The Europe warehouse automation market is projected to expand significantly, growing from USD 9.1 billion in 2025 to USD 27.3 billion by 2032, reflecting a 16.8% CAGR. Automated storage and retrieval systems (ASRS) will dominate with 35% of the market share, while robotics—particularly automated forklifts, AGVs, and drones—will grow at an 18% CAGR as e-commerce fulfillment centers and distribution hubs demand more efficient operations. AI-driven warehouse management systems (WMS) will drive operational optimization across sectors, while energy-efficient automation solutions are gaining traction due to the increasing sustainability goals imposed by EU regulations. The e-commerce sector will represent 50% of the market demand, followed by logistics with 20%.

Market Analysis

The rise of smart factories and intelligent warehouses is shifting the landscape in the Europe warehouse automation market. The adoption of AI-driven WMS, robotics (such as automated forklifts, robots, and drones), and automated guided vehicles (AGVs) is transforming warehouse operations. Companies are integrating IoT sensors into their systems to improve real-time tracking, inventory accuracy, and dynamic route optimization. The need for predictive maintenance, energy-efficient solutions, and real-time decision-making is propelling the growth of robotic systems in the logistics sector. As e-commerce continues to expand, AI-powered systems are streamlining workflows and enabling faster order fulfillment, creating a high demand for automation solutions. Energy-efficient automated systems are becoming a key selling point as companies seek to comply with EU sustainability and energy consumption regulations.

Trends & Insights

- E-commerce driving real-time inventory management through AI-based WMS.

- AGVs and drones becoming integral in last-mile delivery and intra-warehouse logistics.

- Automation in warehousing improving order fulfillment speeds by up to 50%.

- AI-powered robots assisting with picking, sorting, and packaging operations.

- Sustainability-focused design leading to low-emission and energy-saving automation solutions.

- Data-driven decision-making enabling on-the-fly route optimization and maintenance scheduling.

- Cloud-based solutions gaining traction for scalability and remote monitoring.

- Warehouse leasing models integrating automation as a service for greater flexibility.

- Robotics-as-a-service (RaaS) model offering affordable automation options for SMEs.

- Collaborative robots (cobots) enhancing human-robot interaction and safety in warehouses.

Segment Analysis

The warehouse automation market is divided by product type, industry, and application. Automated storage and retrieval systems (ASRS) dominate with 35% market share, followed by robotics and AI-based WMS solutions. By industry, e-commerce represents the largest demand, as fast order fulfillment and inventory tracking are key needs. Logistics and automotive industries are expanding their automation adoption, particularly in distribution centers. Industrial safety solutions are seeing significant growth, with companies increasingly adopting robotic safety systems to minimize workplace injuries. The energy-efficient solutions segment is also gaining ground, especially in regions where green building certifications and sustainability initiatives are a priority.

Geography Analysis

The UK, Germany, and France are the top adopters of warehouse automation technologies in Europe, driven by supply chain innovation and government sustainability mandates. Germany leads with its strong manufacturing and automotive sectors, which are early adopters of robotics and AI-based solutions. France is investing heavily in logistics automation, particularly in the retail and e-commerce sectors. Southern Europe, particularly Italy and Spain, is also witnessing growth in automated warehouses as companies look to enhance supply chain efficiency. Eastern European countries, such as Poland and Hungary, are rapidly catching up, driven by EU funding for automation and smart manufacturing initiatives.

Competitive Landscape

Key players in the Europe warehouse automation market include Siemens, Rockwell Automation, Honeywell, Schneider Electric, KUKA, Fanuc, Dematic, and Swisslog. Siemens and Rockwell Automation are leaders in SCADA and WMS solutions, while Honeywell and Schneider Electric offer energy-efficient warehouse solutions. KUKA and Fanuc dominate the robotics segment, providing automated forklifts and robotic arms for manufacturing and logistics applications. Dematic and Swisslog are leading in automated storage solutions and intralogistics, with a focus on AI integration and smart warehouse management. Strategic alliances between software developers, OEMs, and robotics manufacturers are accelerating innovation in the warehouse automation landscape.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071