68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

USA Building-Integrated Photovoltaics (BIPV) Modules Market (2026–2034): Forecasting from ~USD 3.2 Billion in 2025 to ~USD 17.2 Billion by 2034, CAGR (~20.3%) | Crystalline Silicon, Thin-Film, Commercial & Industrial Applications

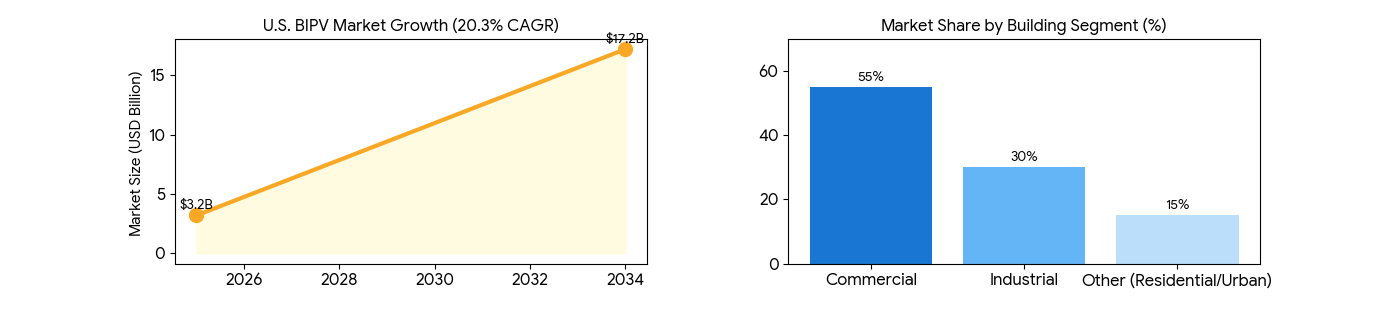

The USA Building-Integrated Photovoltaics (BIPV) modules market is expected to grow significantly from USD 3.2 billion in 2025 to USD 17.2 billion by 2034, driven by a 20.3% CAGR. This rapid growth is propelled by energy-efficient construction trends, government incentives for green buildings, and advancements in photovoltaic technology. BIPV systems, incorporating crystalline silicon and thin-film technologies, offer dual functionality—serving as both building material and energy generator. With increasing demand for commercial and industrial applications, particularly in urban developments, BIPVs are becoming a crucial element in sustainable architecture. The integration of solar modules into roofs, facades, and windows reduces energy consumption and carbon footprints while providing cost savings in the long term. As the U.S. shifts toward net-zero energy buildings, BIPVs are set to play a critical role in achieving these ambitious goals, especially in line with Clean Energy Standards and Building Code improvements.

What's Covered?

Report Summary

Key Takeaways

- Market forecast: USD 3.2B (2025) to USD 17.2B (2034) at 20.3% CAGR.

- Crystalline silicon BIPV systems will dominate with 45% of total market share.

- Thin-film technology to grow fastest at 22% CAGR due to cost reduction.

- Commercial buildings represent 55% of market demand, followed by industrial at 30%.

- Urban areas will see a 30% increase in BIPV adoption by 2030.

- Government incentives for net-zero energy buildings will drive 40% of market growth.

- Roof-integrated systems lead the market, accounting for 60% of BIPV installations.

- Energy savings from BIPV systems expected to reduce building energy costs by 30%.

- Solar windows and facade-integrated panels gaining popularity for architectural aesthetics.

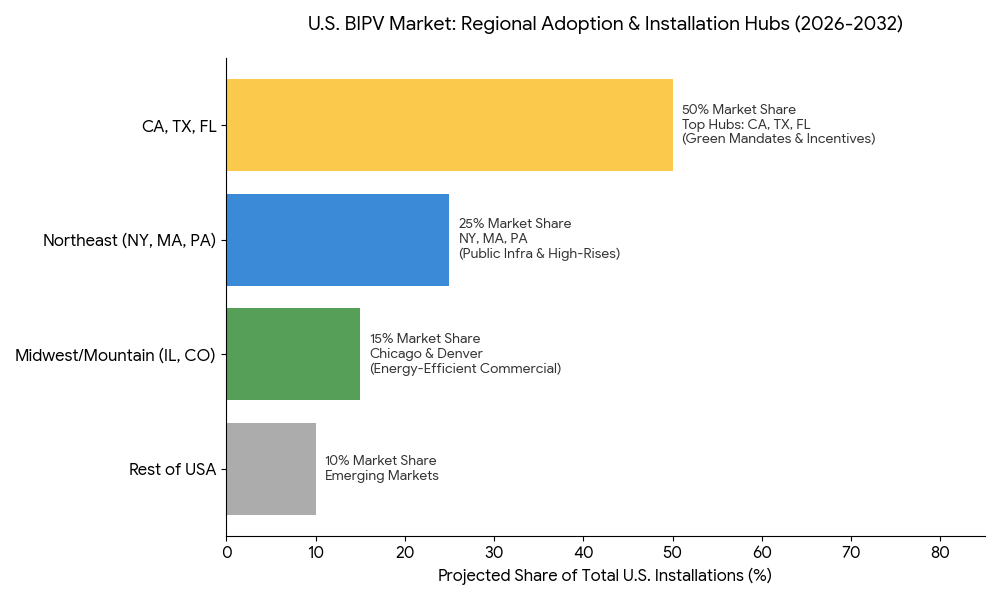

- California, Texas, and Florida are leading adopters of BIPV systems.

Market Size & Share

The U.S. BIPV market is expected to grow significantly, reaching USD 17.2 billion by 2034 from USD 3.2 billion in 2025, representing a 20.3% CAGR. Crystalline silicon BIPV systems are projected to hold 45% of market share, with the thin-film segment growing fastest at 22% CAGR due to reductions in manufacturing costs. Commercial buildings will continue to be the largest segment, contributing 55% of market share, while industrial applications will represent 30%. Government regulations, such as building code revisions and net-zero building mandates, will drive a significant portion of market growth. By 2030, urban areas will see a 30% increase in the use of BIPV systems for roof, facade, and window applications.

Market Analysis

The U.S. BIPV market is benefiting from a combination of policy support, technological innovation, and rising demand for sustainable building materials. Key drivers include reduced energy consumption, lower carbon footprints, and long-term cost savings. The market is evolving with innovations in solar windows, transparent BIPV modules, and integrated energy management systems, which enhance both aesthetic value and functionality. Crystalline silicon panels remain dominant due to their high efficiency, while thin-film technology is being increasingly adopted for lower-cost installations and its suitability for large surface areas. Urbanization trends and the push for smart cities are accelerating the adoption of BIPVs, with local governments encouraging green building certifications and renewable energy integration.

Trends & Insights

- Architectural Integration: Transparent solar windows and facade-integrated panels are gaining market traction for energy efficiency and aesthetic appeal.

- Urbanization Impact: Demand for green buildings and eco-friendly materials is driving urban BIPV installations.

- Battery Storage Integration: The rise of solar + storage systems is driving demand for BIPVs with integrated storage capabilities.

- Government Subsidies: Federal and state-level tax credits and incentives fueling adoption of BIPV technologies.

- Commercial Building Growth: Retailers, warehouses, and office buildings adopting BIPVs for energy efficiency and solar panel integration.

- Cost Reductions: Advancements in thin-film technology and manufacturing efficiency are lowering the initial investment required for BIPV installations.

- Smart Cities: Increasing focus on smart grids and building automation systems driving BIPV adoption in city-wide energy programs.

- BIPV as a Service: Emerging financing models allowing property developers and builders to adopt BIPVs without upfront capital expenditures.

- Post-installation Support: Growing demand for maintenance contracts and system performance monitoring for long-term reliability.

- Recycling and Sustainability: Eco-friendly manufacturing processes and module recycling initiatives promoting sustainability in the BIPV value chain.

Segment Analysis

The market is segmented by product type, application, and technology. Crystalline silicon BIPV systems are expected to hold 45% market share in 2025 due to their high conversion efficiency and widespread use in residential, commercial, and industrial buildings. The thin-film segment will grow the fastest, driven by lower manufacturing costs and the ability to be applied on larger surface areas. By application, residential buildings will represent 40% of the market, with commercial buildings following at 30%. Industrial applications, including factories and warehouses, will continue to expand, accounting for 25% of total demand.

Geography Analysis

California, Texas, and Florida are projected to lead the market, accounting for 50% of total BIPV installations, driven by the states' green energy mandates, net-zero goals, and incentive programs. Northeastern states such as New York, Massachusetts, and Pennsylvania are also adopting BIPVs for public infrastructure and high-rise buildings, aligned with the region’s climate action policies. Chicago and Denver are emerging hubs for commercial applications due to rising demand for energy-efficient office buildings. Urban centers with a high concentration of smart city developments and eco-conscious building practices will see the highest adoption of BIPVs through 2032.

Competitive Landscape

Key players in the U.S. BIPV market include Tesla (Solar Roof), Onyx Solar, Sungrow, Solaria, Panasonic, Sharp Solar, and Soltec. Tesla is leading with its Solar Roof product, combining high-efficiency solar cells with architectural roofing materials. Onyx Solar specializes in transparent solar windows, while Sungrow focuses on integrating BIPV with energy storage solutions. Panasonic and Sharp Solar are expanding their thin-film offerings, targeting large-scale building facades. Solaria and Soltec are enhancing efficiency and aesthetic appeal of BIPV modules, offering customized solar glass for integration into building envelopes. Companies are also increasingly partnering with construction firms, energy providers, and smart grid developers to deliver integrated BIPV solutions.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071