68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

USA Industrial Robotics Market (2026–2034):USD 7.4 Billion in 2024 to ~USD 27.6 Billion by 2034, CAGR (~14.1%) | Traditional & Collaborative Robots, Payload Classes, Manufacturing, Automotive & Electronics Applications

The USA industrial robotics market is forecast to grow exponentially from USD 7.4 billion in 2024 to USD 27.6 billion by 2034, recording a strong CAGR of 14.1%. Growth is fueled by the rapid adoption of automation, the rise of collaborative robots (cobots), and technological advancements in AI, machine vision, and IoT integration. The manufacturing, automotive, and electronics sectors are leading adopters, driven by labor shortages, demand for precision, and increasing productivity requirements. Small and mid-sized enterprises (SMEs) are also accelerating adoption due to lower robot costs and improved ROI. The push for reshoring U.S. manufacturing, coupled with the emergence of Industry 4.0, is enhancing deployment across assembly lines, material handling, and quality control processes. Additionally, collaborative robots designed for human-robot interaction will drive the next phase of industrial automation, while AI-enabled predictive maintenance reduces downtime and operational costs.

What's Covered?

Report Summary

Key Takeaways

- Market to expand from USD 7.4B (2024) to USD 27.6B (2034) at 14.1% CAGR.

- Collaborative robots (cobots) to grow at 18% CAGR, outpacing traditional robots.

- Automotive manufacturing remains the largest application, with 30% market share.

- Electronics sector to grow at 15.2% CAGR due to precision assembly and microcomponent handling.

- Material handling robots to account for 25% of installations by 2030.

- SMEs adopting robotics to improve productivity and offset labor shortages.

- AI integration and IoT connectivity boosting predictive maintenance efficiency.

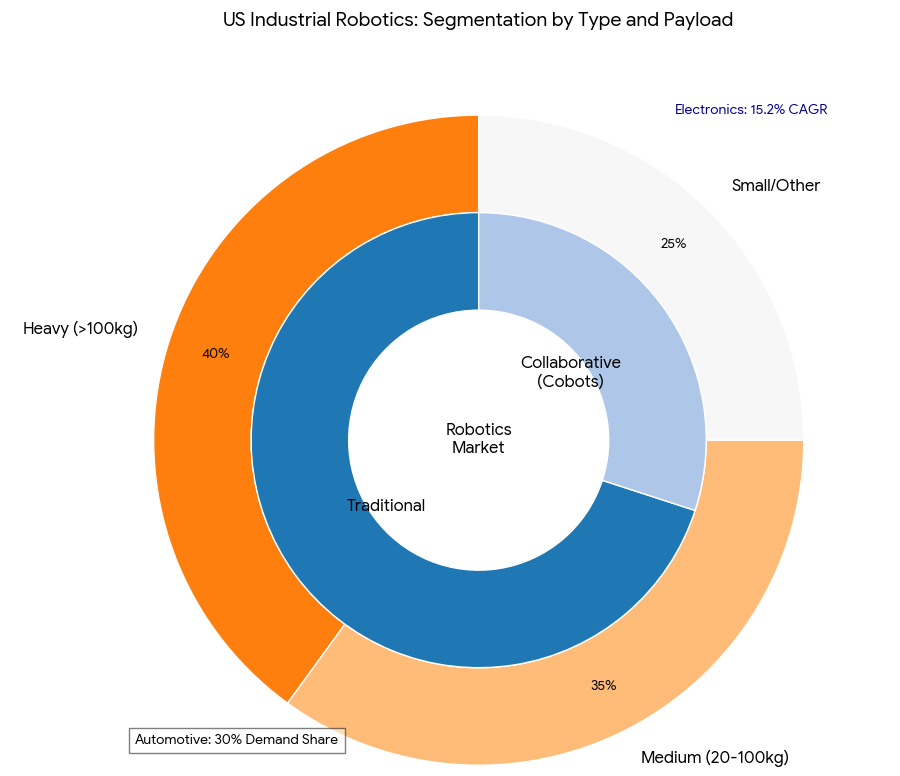

- Heavy payload robots dominate industrial manufacturing, with 40% share.

- Labor cost optimization driving automation in warehousing and logistics.

- U.S. firms to invest over USD 3.5B annually in robotics R&D by 2030.

Market Size & Share

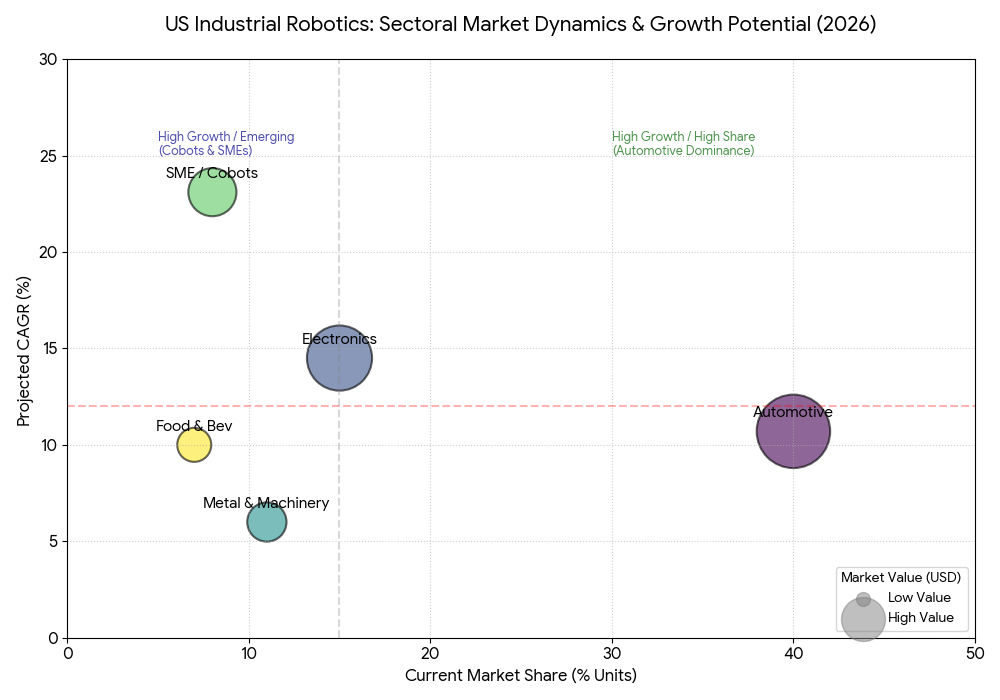

The U.S. industrial robotics market is expected to expand from USD 7.4 billion in 2024 to USD 27.6 billion by 2034, achieving a 14.1% CAGR. The automotive and electronics industries will dominate adoption, accounting for 55% of market share collectively. The rise of collaborative robots (cobots)—offering flexibility and safety in shared workspaces will reshape factory automation, growing at an estimated 18% CAGR. Material handling and assembly applications will account for 25% of total installations by 2030, while heavy payload robots will maintain 40% of the market share due to their extensive use in industrial manufacturing. The U.S. government’s focus on manufacturing modernization and reshoring production is creating favorable conditions for automation investments across sectors.

Market Analysis

Industrial robotics adoption in the U.S. is being accelerated by AI, machine vision, and edge computing innovations, which are enhancing performance and accuracy. Automotive manufacturers remain the primary adopters, using robots for welding, painting, and assembly operations. The electronics sector is experiencing robust growth due to precision manufacturing needs for semiconductors and consumer devices. Furthermore, labor shortages and rising wage pressures are pushing SMEs toward automation. Collaborative robots are emerging as key enablers for SMEs, providing an optimal balance between cost, flexibility, and ease of integration. The demand for connected robots, capable of data sharing through IoT platforms, is expected to increase operational efficiency across the industrial ecosystem.

Trends & Insights

- AI-Powered Robots: Integration of AI and ML algorithms is enabling adaptive learning and autonomous decision-making.

- Collaborative Robots (Cobots): Rising adoption in SMEs for cost-effective automation.

- Reshoring Manufacturing: U.S. industries bringing production back home to mitigate supply chain risks.

- Predictive Maintenance: IoT-enabled sensors improving uptime by predicting mechanical failures.

- Workforce Augmentation: Human-robot collaboration redefining industrial productivity models.

- Heavy-Duty Payload Expansion: Robots capable of lifting >100 kg gaining traction in automotive manufacturing.

- Modular Robot Design: Allowing scalability and customization across industrial applications.

- Data-Driven Optimization: Robotics data analytics improving throughput and process efficiency.

- Green Robotics: Energy-efficient robot designs reducing power consumption by up to 20%.

- Public-Private Partnerships: Increased federal investment in robotics R&D to boost industrial innovation.

Segment Analysis

The market is segmented by robot type, payload class, and end-use industry. Traditional industrial robots account for 70% of installations, while collaborative robots are projected to grow at 18% CAGR, reaching 30% share by 2030. By payload, heavy payload robots (>100 kg) dominate with 40% share, followed by medium payload (20–100 kg) robots at 35%. The automotive industry leads adoption, accounting for 30% of total demand, while electronics and semiconductor manufacturing will grow fastest at 15.2% CAGR. General manufacturing and warehousing will also contribute significantly as automation extends beyond traditional assembly lines.

Geography Analysis

Within the U.S., industrial robotics adoption is concentrated in California, Texas, Michigan, and Ohio, which host large manufacturing and automotive clusters. The Midwest remains a key hub for automotive production, while California’s tech corridor is leading investments in AI-integrated robotics. Southern states are emerging as new automation centers due to lower operating costs and logistics advantages. Cross-industry adoption—particularly in electronics, packaging, and warehousing—is spreading robotics demand across the nation. The expansion of robotics-as-a-service (RaaS) models is also accelerating adoption among SMEs across all U.S. regions.

Competitive Landscape

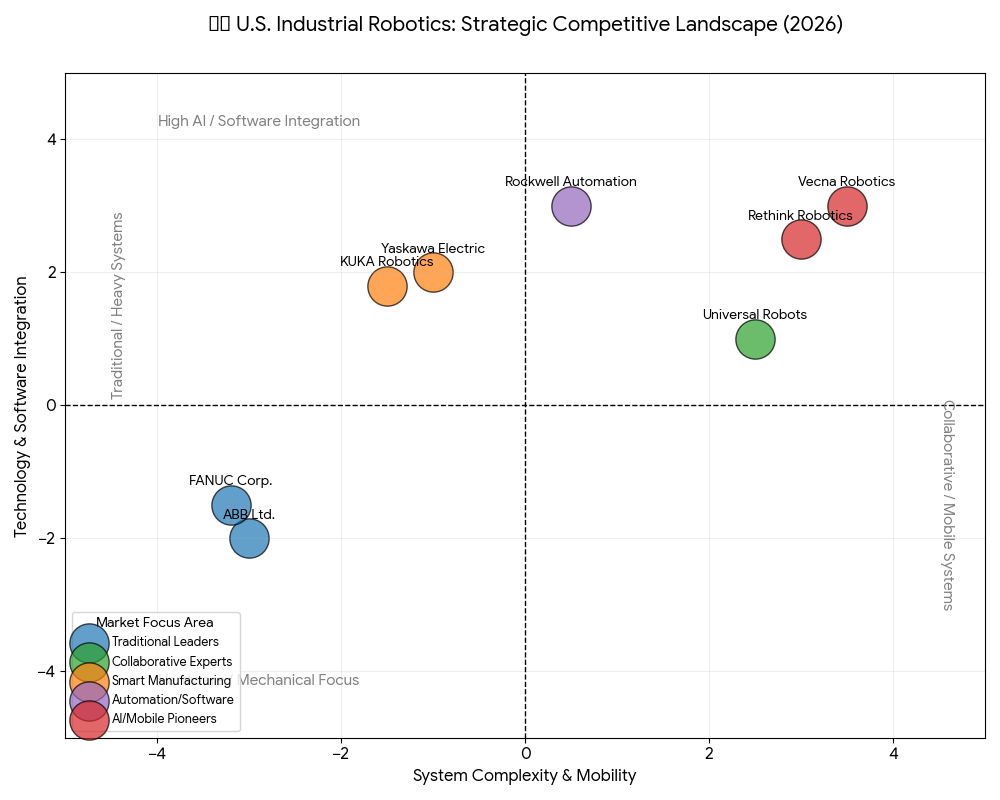

Key players in the U.S. industrial robotics market include ABB Ltd., FANUC Corporation, Yaskawa Electric, KUKA Robotics, Universal Robots, and Rockwell Automation. ABB and FANUC lead in heavy payload and traditional robotic systems, while Universal Robots dominates the collaborative robotics space with lightweight, flexible systems. Yaskawa and KUKA are expanding in smart manufacturing solutions integrating AI and machine learning. Emerging U.S.-based players such as Rethink Robotics and Vecna Robotics are pioneering AI-driven and mobile robotic solutions. Strategic partnerships between robotics OEMs, AI startups, and industrial automation firms will continue to shape competitive advantages through innovation, interoperability, and R&D investments.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071