68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

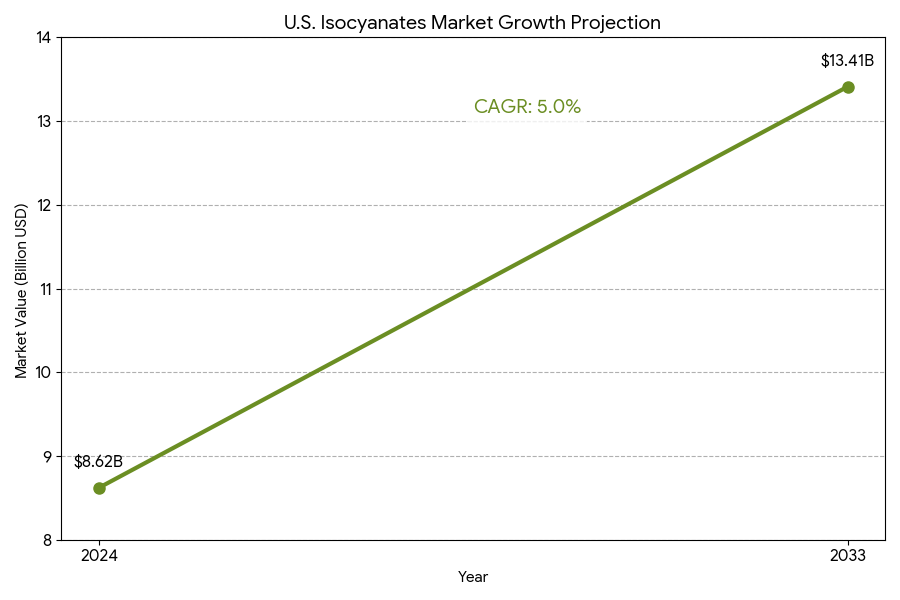

U.S. Isocyanates Market (2025–2033): From ~USD 8.62 Billion in 2024 to USD 13.41 Billion by 2033 & CAGR (~5.0%) | Polyurethane Foams, Coatings, Adhesives, Insulation

The U.S. isocyanates market is projected to grow from USD 8.62 billion in 2024 to USD 13.41 billion by 2033, at a CAGR of 5.0%. The primary drivers of this growth are the increasing demand for polyurethane foams, coatings, adhesives, and insulation materials across various industries, including construction, automotive, and furniture manufacturing. Polyurethane foams, particularly in building insulation, are expected to be the largest consumer of isocyanates, owing to their energy-efficient properties and widespread use in energy-efficient building materials. The automotive industry will continue to rely on coatings and adhesives, driving demand for isocyanates in automotive manufacturing. Environmental considerations and the move towards sustainable, bio-based isocyanates will shape the market as manufacturers look to reduce the use of volatile organic compounds (VOCs) in their formulations. The growth in infrastructure projects and increased construction activity will further contribute to the rising demand for insulation and coatings.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 8.62B (2024) to USD 13.41B (2033) at 5.0% CAGR.

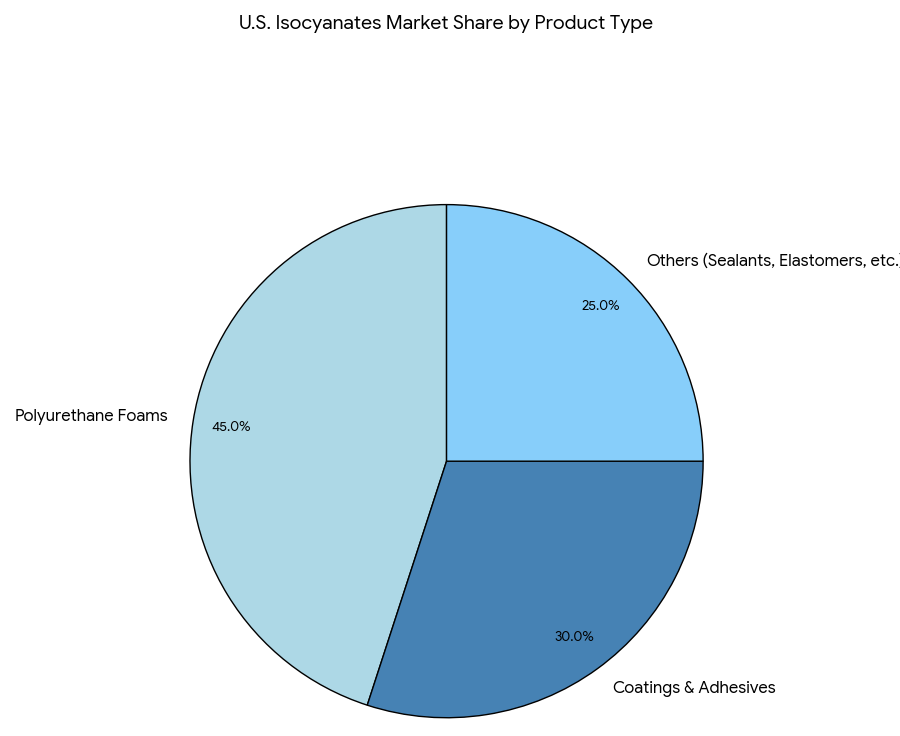

- Polyurethane foams expected to account for 45% of total isocyanate demand.

- Coatings and adhesives will drive 30% of market demand.

- Construction and insulation applications will represent 60% of isocyanate use by 2030.

- Automotive sector to contribute 25% of market share due to demand for adhesives.

- Bio-based isocyanates are projected to capture 15% of the market by 2030.

- Energy-efficient construction driving growth in insulation demand.

- Green chemistry and sustainable practices will influence product development.

- North America and Europe lead demand for polyurethane foams and coatings.

- Increased focus on high-performance coatings for automotive and furniture industries.

Key Metrics

Market Size & Share

The U.S. isocyanates market is forecast to expand from USD 8.62 billion in 2024 to USD 13.41 billion by 2033, driven by increased demand in polyurethane foams, coatings, adhesives, and insulation. Polyurethane foams will dominate, accounting for 45% of the total demand due to their use in energy-efficient insulation. Coatings and adhesives will continue to see strong demand, contributing 30% of the market share, particularly in the automotive and furniture sectors. Insulation applications will represent 60% of demand by 2030, fueled by growing interest in green buildings and eco-friendly construction.

Market Analysis

The U.S. isocyanates market is significantly influenced by the growing demand for polyurethane foams in insulation and energy-efficient applications. As the push for sustainable construction increases, insulation products using isocyanates will gain more prominence. The automotive industry continues to be a strong driver of adhesive and coating demand, while the furniture market benefits from increased demand for high-performance coatings. As sustainability becomes a higher priority, bio-based isocyanates are poised to make up a significant portion of the market by 2030. The market is also being shaped by green chemistry initiatives that encourage the production of non-toxic, eco-friendly isocyanates.

Trends & Insights

- Sustainable Construction: Energy-efficient building materials are driving demand for insulation products using polyurethane foams.

- Bio-Based Isocyanates: As sustainability regulations tighten, bio-based isocyanates are increasingly in demand, offering eco-friendly alternatives.

- Automotive Sector Growth: Coatings and adhesives for automotive applications, particularly vehicle interiors, are expected to grow at 6% CAGR.

- Furniture Demand: The furniture sector is driving growth for high-performance coatings that improve durability and aesthetic appeal.

- Green Chemistry: Non-toxic, sustainable production methods will drive the future of isocyanates production, particularly in the pharmaceutical and coatings industries.

- Sustainability Focus: The shift towards low-VOC and environmentally friendly coatings will push isocyanates towards bio-based solutions.

- Regulatory Pressure: Stricter environmental regulations will force manufacturers to innovate and improve supply chain efficiency.

- Technological Innovations: Ongoing advancements in polyurethane chemistry will create high-performance materials with lower environmental impact.

- Supply Chain Resilience: Sourcing challenges for raw materials in the isocyanates market will push for localized production and better supply chain management.

- Consumer Trends: Increased consumer preference for eco-friendly furniture and automotive materials will continue to influence coatings and adhesives demand.

Segment Analysis

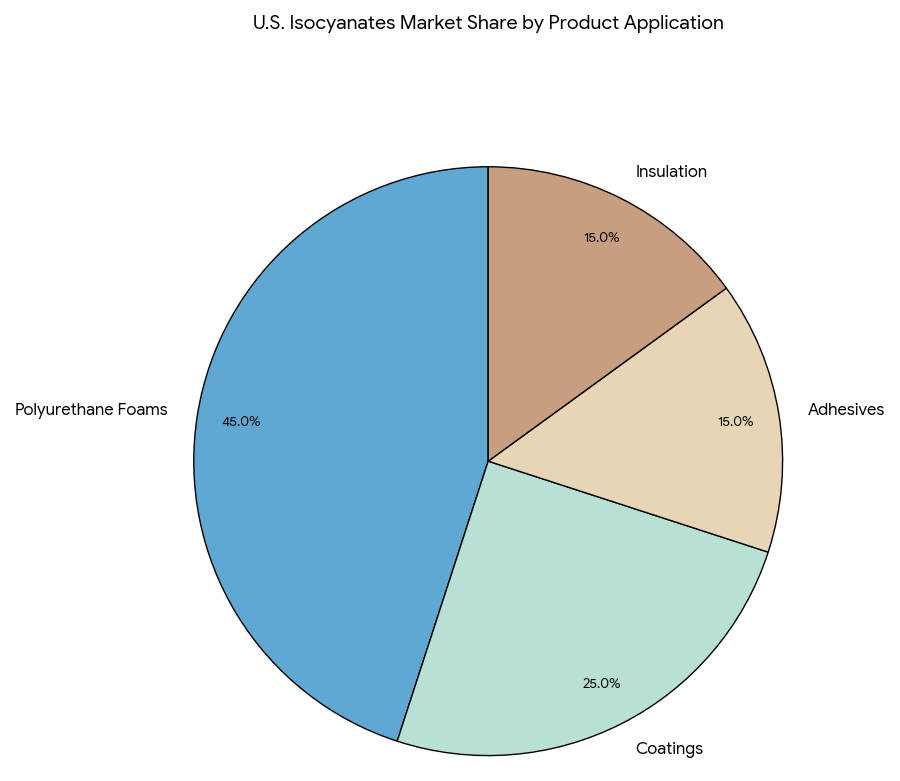

The isocyanates market is segmented by product application: polyurethane foams (45%), coatings (25%), adhesives (15%), and insulation (15%). Polyurethane foams are the largest segment, primarily driven by insulation needs in buildings, homes, and electrical systems. Coatings represent a significant share, particularly in automotive and furniture sectors, where high-performance coatings are in demand. The adhesives segment will see steady growth, driven by applications in automotive manufacturing, electronics, and furniture production. The insulation segment will grow due to demand for green building materials.

Geography Analysis

North America and Europe will continue to lead the isocyanates market, accounting for 55% of total market share. North America, particularly the U.S., remains the largest consumer due to high automotive production and demand for energy-efficient building materials. Europe follows closely due to strong regulations promoting sustainability and the adoption of green chemistry. Asia-Pacific, especially China and India, will witness the highest growth at 9% CAGR, driven by industrialization, automotive demand, and growing construction activities. Latin America is expected to grow moderately, with key demand coming from automotive and construction sectors.

Competitive Landscape

Key players in the U.S. isocyanates market include BASF, Covestro, Huntsman Corporation, Dow Chemical, and Wanhua Chemical Group. BASF leads the market with high-performance isocyanates used in automotive coatings and flame retardants. Covestro focuses on the production of bio-based isocyanates, catering to the growing demand for sustainable chemicals. Huntsman and Dow lead in the polyurethane and adhesive applications, while Wanhua Chemical focuses on cost-effective, large-scale production. Smaller regional players are increasingly focusing on localized production to meet the demand for green, eco-friendly materials.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071