68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Energy Storage Chemicals Market (2024–2033): Forecasting from ~USD 130.0 Million in 2024 to USD 500.3 Million by 2033, CAGR (~16.3%) | Lithium-Ion, Sodium-Ion, and Hydrogen Fuel Technologies Drive Growth

The global energy storage chemicals market is projected to surge from USD 130 million in 2024 to USD 500.3 million by 2033, reflecting a robust CAGR of 16.3%. Growth is driven by expanding battery-based energy storage in electric vehicles, renewables, and grid stabilization. Lithium-ion batteries dominate due to high energy density and innovation, while sodium-ion batteries are gaining traction for large-scale, cost-effective solutions. Hydrogen fuel technology is set for increased demand, especially in long-duration storage. The sector’s expansion is further supported by governmental incentives, corporate investments, and R&D efforts, all of which are essential for achieving energy independence, carbon neutrality, and reliable grid systems worldwide.

What's Covered?

Report Summary

Key Takeaways

- Market to expand from USD 130M (2024) to USD 500.3M (2033) at 16.3% CAGR.

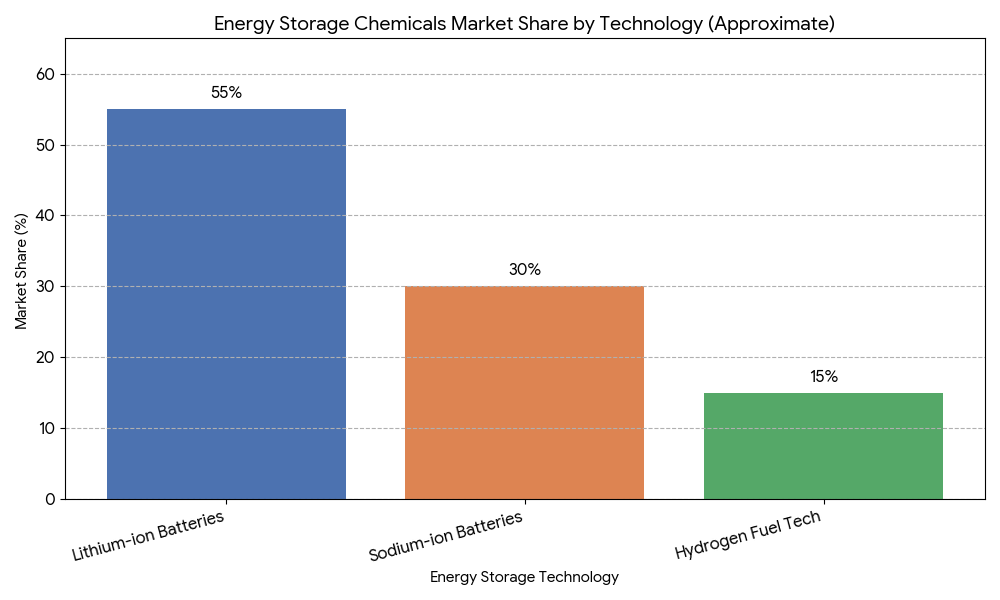

- Lithium-ion batteries will remain the dominant technology, capturing 55% of total market share.

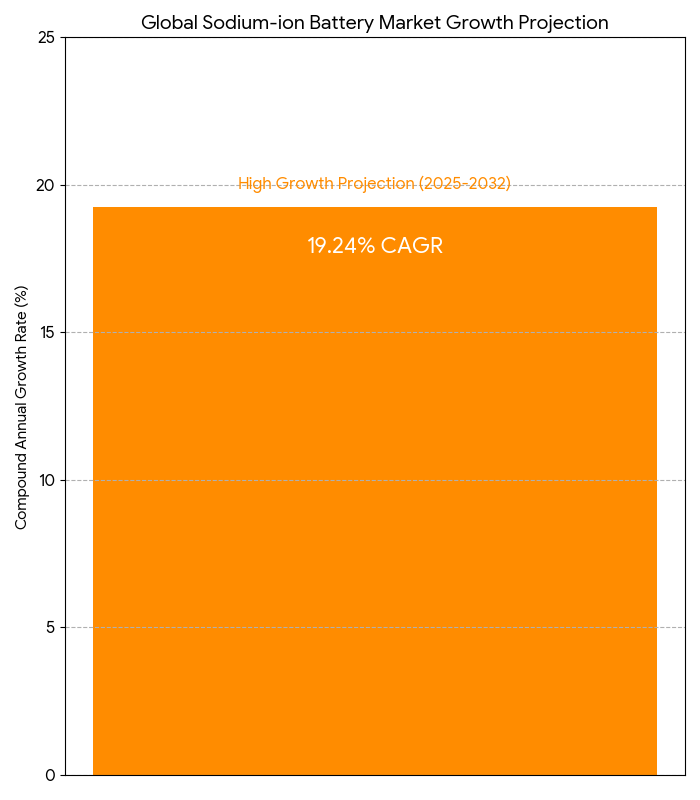

- Sodium-ion technology is expected to grow at 18% CAGR, driven by low-cost and large-scale applications.

- Hydrogen fuel technologies projected to contribute 15% of the market by 2030, with strong growth in long-duration energy storage.

- Renewable energy storage applications will account for 35% of the total market share.

- EV battery production to be the largest end-use sector, driving 60% of demand by 2030.

- Solid-state and high-energy-density lithium-ion technologies to push performance and efficiency.

- Government policies and carbon-neutral targets are significantly boosting investment in energy storage solutions.

- Sodium-ion batteries to gain traction in cost-effective and sustainable storage solutions for grid stabilization.

- Battery recycling and sustainability trends will increase raw material supply and lower production costs.

Key Metrics

Market Size & Share

The energy storage chemicals market is expected to grow from USD 130 million (2024) to USD 500.3 million (2033), with lithium-ion batteries remaining the dominant technology, holding 55% of total market share. Sodium-ion technology is expected to grow at 18% CAGR, driven by its cost-effectiveness for large-scale energy storage solutions. Hydrogen fuel technologies, essential for long-duration energy storage, are forecast to capture 15% of the market by 2030. Renewable energy storage and EV battery production are expected to contribute 60% of total demand by 2030. Solid-state and high-energy-density technologies are advancing lithium-ion battery performance, while sodium-ion will offer more affordable solutions in grid storage applications.

Market Analysis

The demand for energy storage chemicals is largely influenced by the growing adoption of electric vehicles (EVs), renewable energy sources, and grid stabilization technologies. Lithium-ion continues to lead due to its high energy density, but the cost-effectiveness of sodium-ion batteries is driving interest in large-scale energy storage for grid applications. Hydrogen fuel technologies are gaining momentum as long-duration energy storage solutions, especially in industries requiring extended storage times, such as renewable energy integration. The demand for bio-based and sustainable storage solutions is expected to rise as carbon-neutral goals and government policies push for greener energy solutions. Sodium-ion and hydrogen technologies will gradually carve out larger market shares, with a shift towards more sustainable alternatives for energy storage.

Trends & Insights

- Sodium-Ion Adoption: Growing demand for affordable and eco-friendly energy storage solutions.

- Hydrogen Fuel Boom: Increased interest in long-duration storage for grid and industrial uses.

- Lithium-Ion Dominance: Continued lead in EV production and renewable energy storage.

- Solid-State Technology: Lithium-ion advancements focus on solid-state batteries for higher safety and energy efficiency.

- Cost Reduction: Ongoing efforts to reduce the cost of sodium-ion batteries and make them more competitive with lithium-ion.

- Recycling and Sustainability: Strong push for battery recycling and sustainable sourcing of raw materials to meet market demand.

- Global Expansion: Europe, North America, and Asia leading investments in energy storage infrastructure and battery manufacturing.

- Grid Modernization: Expansion of renewable energy sources necessitating energy storage for grid stabilization.

- Government Support: Incentives and policies supporting green energy solutions, boosting the adoption of energy storage chemicals.

- Research and Innovation: Increased R&D in solid-state technologies and hydrogen storage systems to drive long-term growth.

Segment Analysis

The market is segmented by battery type and grade:

- Lithium-ion batteries dominate the market with 55% of total demand, driven by the high energy density and wide application in EVs and ESS.

- Sodium-ion batteries are projected to grow at 18% CAGR, driven by demand in large-scale, cost-efficient storage applications.

- Hydrogen fuel technologies are expanding, especially for long-duration energy storage in industrial and grid applications, and will represent 15% of total market share by 2030.

- By grade, battery-grade lithium-ion additives will account for 65% of the total, while technical-grade will serve industrial uses in ceramics and glass applications.

Geography Analysis

The U.S. and Europe lead the market, with North America accounting for 40% and Europe capturing 35% of the demand due to strong electric vehicle adoption and renewable energy integration. The Asia Pacific region is expected to experience significant growth, especially in China and India, driven by government incentives for electric mobility and energy storage infrastructure. Middle East investments in sustainable energy will also drive demand, particularly in Saudi Arabia and UAE, both of which are building large-scale lithium-ion battery plants to meet regional EV and ESS demand.

Competitive Landscape

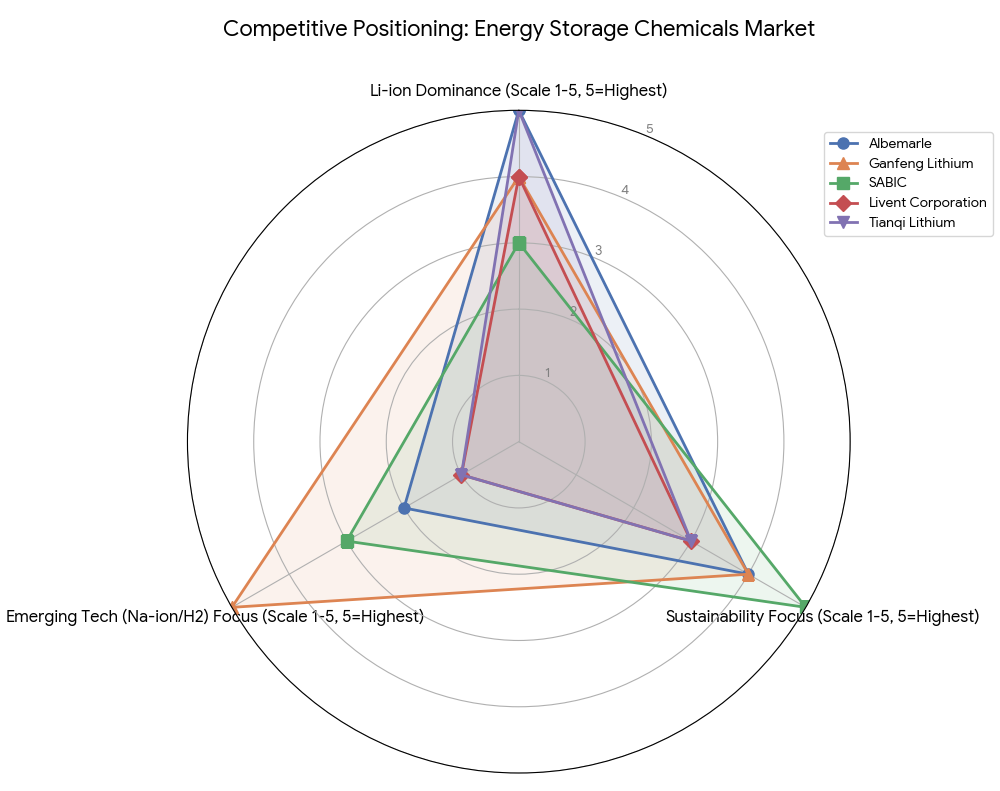

Key players in the global energy storage chemicals market include Albemarle Corporation, SABIC, Tianqi Lithium, Livent Corporation, and Ganfeng Lithium. Albemarle and SABIC are major players in lithium-ion battery additives, with a strong presence in North America and Europe. Livent Corporation and Tianqi Lithium focus on high-purity lithium production, while Ganfeng Lithium is a leading player in sodium-ion and hydrogen fuel storage technologies. Partnerships between battery manufacturers and chemical companies are crucial in advancing sustainable energy storage solutions, with increased R&D efforts targeting cost reduction and product performance improvements.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071