68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Asia-Pacific Lithium Chemicals Market (2025–2030): From ~USD 6.50 Billion in 2023 to USD 18.99 Billion by 2030 & CAGR (~17.0%) | Battery Materials, EV Manufacturing, Energy Storage, Cathode Production”

The Asia-Pacific lithium chemicals market is projected to grow from USD 6.50 billion in 2023 to USD 18.99 billion by 2030, at a CAGR of 17.0%. This growth is primarily driven by the increasing demand for lithium chemicals used in battery materials, electric vehicle (EV) manufacturing, energy storage systems (ESS), and cathode production. The region, particularly China, Japan, and South Korea, is at the forefront of EV production and energy storage technologies, creating a substantial demand for lithium compounds such as lithium carbonate and lithium hydroxide. Lithium chemicals are essential for battery performance, particularly in lithium-ion batteries that power EVs and renewable energy storage systems. As governments and private sectors in the region ramp up clean energy and EV infrastructure investments, the market is poised for substantial growth. Additionally, Asia-Pacific is a hub for cathode production, further fueling demand for lithium. The rise of sustainable sourcing and recycling initiatives will also play a pivotal role in the market expansion.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 6.50B (2023) to USD 18.99B (2030) at 17.0% CAGR.

- Battery materials (lithium carbonate and lithium hydroxide) will account for 55% of total demand.

- EV manufacturing will drive 40% of lithium chemicals demand by 2030.

- Energy storage systems to represent 25% of total market share by 2030.

- China, Japan, and South Korea leading the market, contributing 70% of the regional demand.

- Lithium hydroxide will dominate the market, driven by its use in high-energy-density batteries.

- Sustainable sourcing and recycling initiatives will help meet increasing lithium demand.

- South Asia and Southeast Asia markets to grow at 18% CAGR, fueled by increasing EV adoption.

- Electric mobility will be a key driver for lithium consumption, with the EV market growing rapidly.

- Increased cathode production in Asia-Pacific will drive lithium chemical demand for battery production.

Key Metrics

Market Size & Share

The Asia-Pacific lithium chemicals market is forecast to expand from USD 6.50 billion in 2023 to USD 18.99 billion by 2030. Battery materials, including lithium carbonate and lithium hydroxide, will account for 55% of the total market by 2030, driven by demand for high-performance EV batteries and energy storage systems (ESS). EV manufacturing will contribute 40% of the total demand, with China and South Korea being the largest consumers of lithium chemicals. Energy storage systems (ESS) are expected to account for 25% of market share, while lithium hydroxide will dominate due to its role in high-energy-density cathodes.

Market Analysis

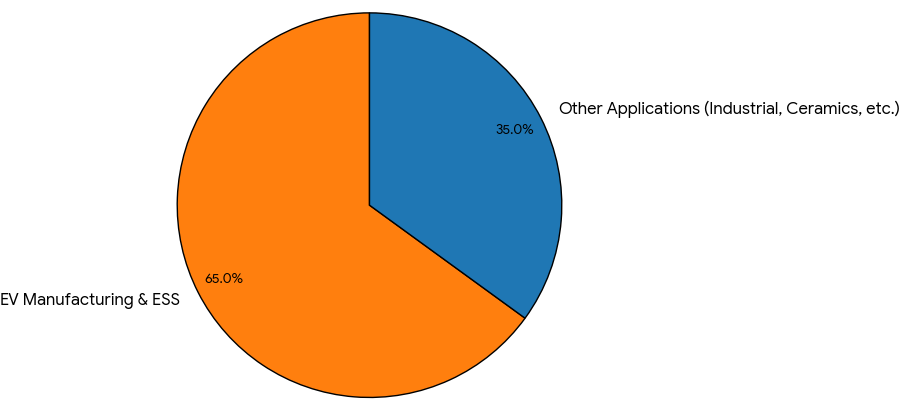

The Asia-Pacific lithium chemicals market is primarily driven by electric vehicle (EV) manufacturing and energy storage systems (ESS), which account for 65% of total demand. Lithium hydroxide remains a critical material for cathode production in EV batteries, while lithium carbonate continues to be in high demand for energy storage solutions. China, South Korea, and Japan are leading markets due to government support for sustainable technologies and electric mobility. The market is also benefiting from sustainable sourcing initiatives and battery recycling efforts, aimed at reducing environmental impact and ensuring a reliable lithium supply.

Trends & Insights

- EV Demand: The rise in electric mobility will drive 40% of market growth, particularly in China, Japan, and South Korea.

- Lithium Hydroxide Growth: Lithium hydroxide demand is expected to dominate, driven by EV battery production and cathode materials.

- Energy Storage Systems: Growing solar and wind energy adoption will increase demand for lithium chemicals used in ESS.

- Sustainability and Recycling: Lithium recycling is expected to grow at 12% CAGR, helping meet future lithium demand.

- Government Incentives: China, India, and Japan are ramping up EV infrastructure investments, boosting lithium chemicals demand.

- Technological Innovations: Advancements in battery technology will improve the efficiency and energy density of lithium-based batteries.

- R&D in Lithium Extraction: Innovations in sustainable lithium extraction technologies will shape the future of the market.

- Market Expansion in Southeast Asia: Countries like Thailand and Vietnam are emerging as key players in lithium-ion battery manufacturing.

- Green Energy Integration: The push for renewable energy systems will further increase demand for lithium chemicals in energy storage solutions.

- Supply Chain Stability: Regional lithium production is expanding to meet growing demand while mitigating supply chain risks.

Segment Analysis

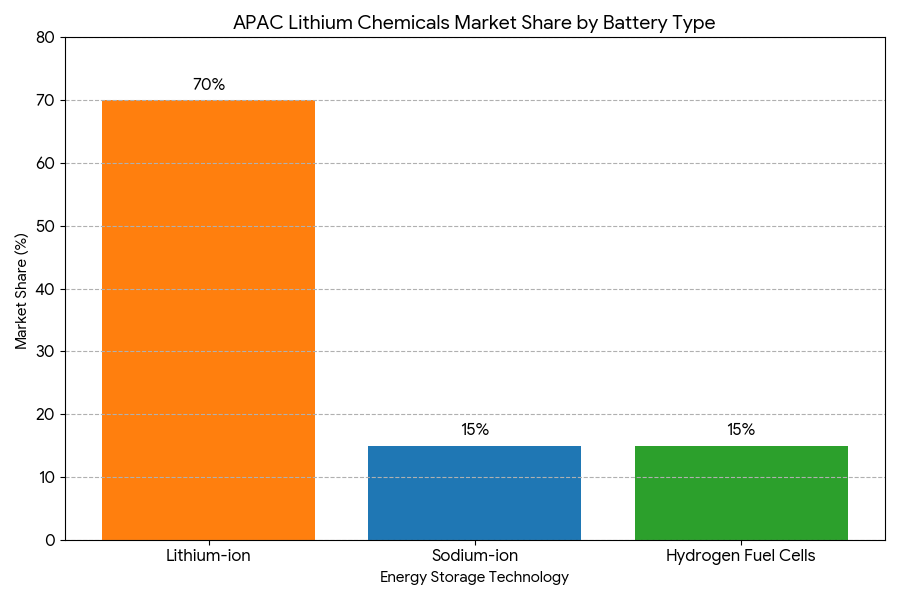

The Asia-Pacific lithium chemicals market is segmented by battery type: lithium-ion (70%), sodium-ion (15%), and hydrogen fuel cells (15%). Lithium-ion batteries will continue to dominate the market due to their widespread use in electric vehicles (EVs) and energy storage systems. Sodium-ion and hydrogen fuel cell technologies are emerging as alternative storage solutions, particularly for grid storage and industrial applications. By grade, the market is divided into battery-grade (80%) and technical-grade (20%) lithium chemicals, with battery-grade chemicals driving the market, particularly in cathode production and battery manufacturing.

Geography Analysis

China, Japan, and South Korea will continue to lead the Asia-Pacific lithium chemicals market, contributing to 70% of the market share due to their dominance in electric vehicle production, battery manufacturing, and energy storage system integration. India is also emerging as a significant player, with the government's focus on clean energy technologies and electric vehicle adoption. Southeast Asia, particularly Vietnam, Thailand, and Indonesia, is expected to grow rapidly at 18% CAGR, driven by industrialization, battery production, and renewable energy projects.

Competitive Landscape

The Asia-Pacific lithium chemicals market is competitive, with global players such as Albemarle Corporation, Ganfeng Lithium, Tianqi Lithium, SQM, and LG Chem dominating the market. Albemarle Corporation leads in lithium production and is focused on expanding its footprint in the Asia-Pacific region. Ganfeng Lithium and Tianqi Lithium are major producers in China, with investments in lithium refining and battery materials. SQM and LG Chem are expanding their partnerships and R&D efforts in sustainable lithium extraction and recycling. Smaller regional players are also increasing their presence, focusing on local production to meet growing demand for sustainable lithium chemicals.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071