68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

U.S. Construction Robots Market (2026–2031): Forecasting from ~USD 420 Million in 2025 to ~USD 1.32 Billion by 2031, CAGR (~21.0%) — Autonomous Equipment, Demolition Robots, Bricklaying, 3D Printing & Smart Construction Applications

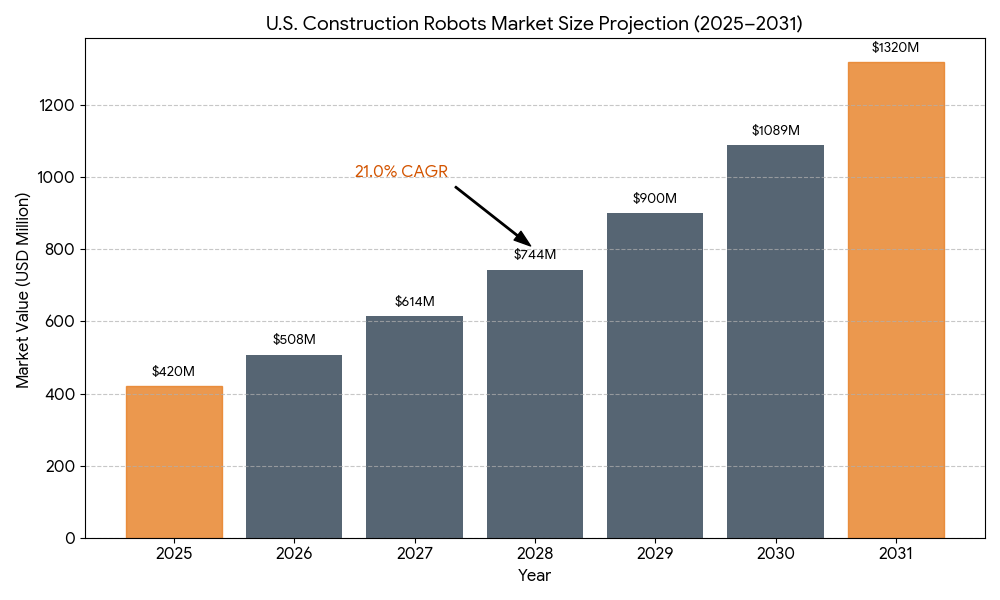

The U.S. construction robots market is set to surge from USD 420 million in 2025 to USD 1.32 billion by 2031, growing at a remarkable CAGR of 21.0%. This expansion is fueled by rising labor shortages, increasing demand for automation in construction, and the push for efficiency and safety across project sites. Key technologies—such as autonomous construction vehicles, demolition robots, bricklaying automation, and 3D printing robotics—are transforming the sector. Integration of AI, computer vision, and IoT is enabling real-time decision-making and predictive maintenance. As smart construction ecosystems evolve, robots are becoming central to modular building, infrastructure repair, and urban development projects. The U.S. is emerging as a global leader in construction robotics innovation, supported by investments in infrastructure modernization and R&D initiatives focused on productivity enhancement.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 420M (2025) to USD 1.32B (2031) at 21.0% CAGR.

- Autonomous equipment accounts for 35% of total market share in 2025.

- Demolition robots to grow fastest at 23% CAGR, driven by urban redevelopment.

- 3D printing construction robots to reach USD 260M by 2031, up from USD 70M in 2025.

- Bricklaying robots improving productivity by 3–5x compared to manual methods.

- AI and vision-guided systems reducing project error rates by over 25%.

- Public infrastructure and housing projects constitute 40% of robot deployments.

- Modular construction and off-site prefabrication emerging as major growth catalysts.

- Workforce safety automation driving compliance with OSHA and sustainability standards.

- Rising construction labor costs and aging workforce accelerating adoption across states.

Market Size & Share

The U.S. construction robots market is projected to grow from USD 420 million in 2025 to USD 1.32 billion by 2031, achieving a 21.0% CAGR. The adoption surge is primarily driven by the labor shortage crisis estimated at over 500,000 workers—and the need to improve safety and productivity. Autonomous heavy equipment, including excavators, bulldozers, and pavers, represents 35% of total revenue, powered by demand for precision grading and real-time navigation. Demolition robots are expected to grow at 23% CAGR, particularly in urban reconstruction projects. 3D printing robots will expand into infrastructure and housing segments, accelerating on-site prefabrication. Public sector investments under the Bipartisan Infrastructure Law are expected to fund large-scale deployments in transportation, energy, and utilities, while private builders increasingly adopt robotics to offset rising material and labor costs.

Market Analysis

The market’s exponential rise is underpinned by the convergence of AI, robotics, and advanced materials technology. Construction robotics are increasingly integrated with Building Information Modeling (BIM) and digital twin platforms, allowing real-time coordination between robots, architects, and site managers. The adoption of autonomous earthmoving equipment and drone-assisted mapping systems is streamlining project timelines. Demolition robots, equipped with hydraulic arms and precision control, are replacing manual labor in hazardous tasks, reducing safety risks. Meanwhile, bricklaying and concrete-printing robots are revolutionizing residential and commercial construction by delivering speed, accuracy, and waste reduction. The modular construction trend—building off-site and assembling on-site will further stimulate robotics integration. Rising ESG standards and green construction goals are pushing for robotics that minimize waste, optimize energy use, and reduce emissions.

Trends & Insights

- Labor Shortage Catalyst: Automation mitigating the skilled labor deficit in construction.

- AI-Enabled Robotics: Vision-based navigation improving real-time site efficiency.

- 3D Printing Boom: On-site additive manufacturing cutting costs by up to 30%.

- Sustainability Focus: Reduced material waste aligning with green building codes.

- Public Infrastructure Push: Federal funding boosting robotics adoption in civil projects.

- Collaborative Robots (Cobots): Enhancing productivity and safety on active sites.

- Digital Twin Integration: Real-time project simulation and workflow optimization.

- Smart Construction Sites: IoT-enabled equipment providing data for predictive analytics.

- Increased Prefabrication: Robots manufacturing standardized components off-site.

- Private Sector Investment: Construction giants partnering with tech startups to scale adoption.

Segment Analysis

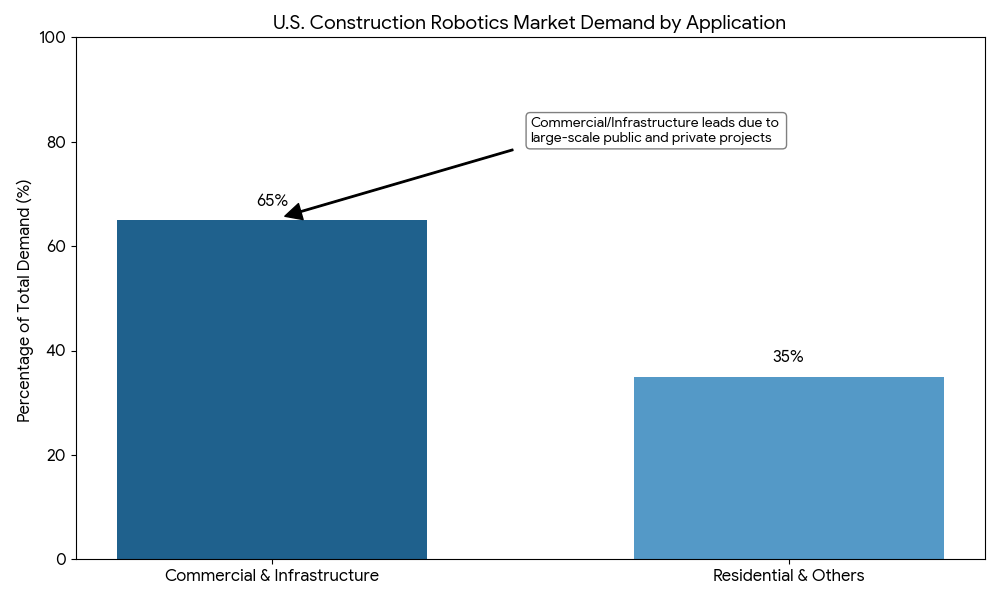

By robot type, autonomous equipment (excavators, dozers, and haulers) dominates with 35% share, driven by integration with AI-based navigation systems. Demolition robots are the fastest-growing category at 23% CAGR, fueled by safety and urban renewal projects. Bricklaying robots are improving build speeds 3–5x, while 3D printing robots are reshaping affordable housing construction. By application, commercial and infrastructure segments collectively represent 65% of total demand, while residential projects are rapidly adopting compact, modular robotic systems. The prefabrication and modular building sector is projected to grow at 18% annually, complementing robotics growth in both design and assembly phases.

Geography Analysis

The U.S. market is led by California, Texas, and Florida, where large-scale urban and infrastructure projects are ongoing. California leads in robotic R&D and startup activity, while Texas and Florida dominate in construction volume and highway development. New York, Illinois, and Washington are key regions for high-rise and commercial automation projects. Midwestern states are beginning to adopt robotics in industrial construction and renewable energy projects, supported by government incentives. The expansion of 3D-printed housing initiatives in Nevada and Arizona is positioning these regions as testbeds for affordable, sustainable automation solutions.

Competitive Landscape

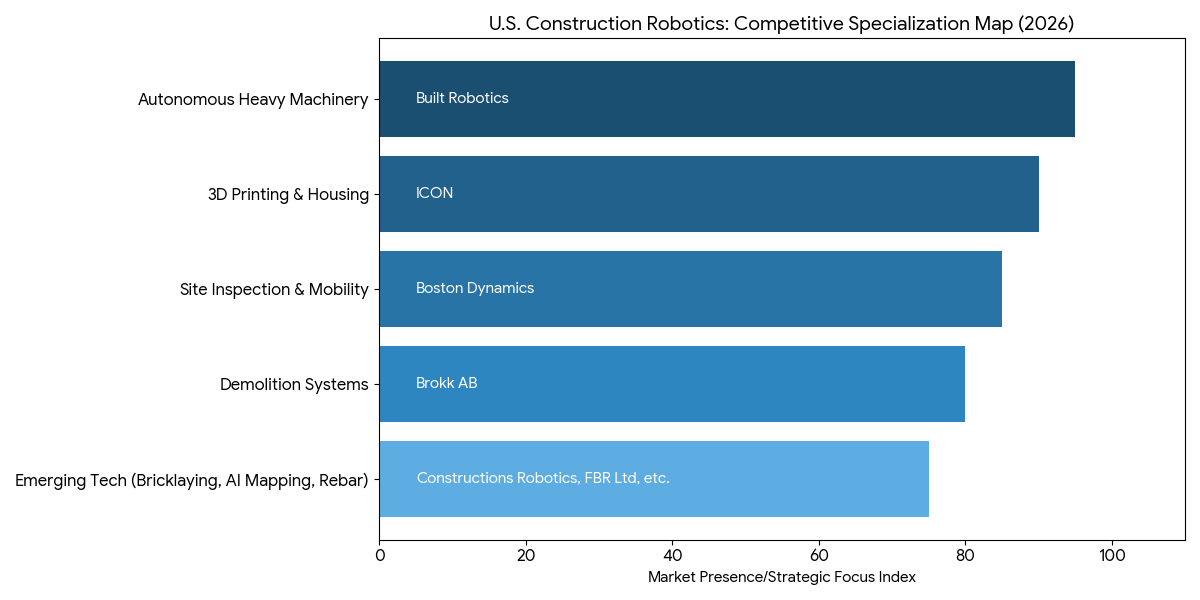

The U.S. construction robots market features leading players such as Built Robotics, ICON, Brokk AB, Boston Dynamics, Constructions Robotics LLC, and FBR Ltd. (Fastbrick Robotics). Built Robotics dominates autonomous heavy machinery, while ICON leads in 3D printing for housing. Boston Dynamics continues to pioneer site inspection and mobility robotics, and Brokk specializes in demolition systems. Emerging companies are focusing on AI-driven site mapping, robotic bricklaying, and automated rebar tying solutions. Strategic collaborations between construction firms, robotics startups, and software developers are reshaping competitive dynamics, with investments centered on machine learning integration, predictive analytics, and cloud-connected project management platforms.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071