68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Space Medicine Commercialization: Microgravity Research & IP Strategy Development - Innovation & R&D

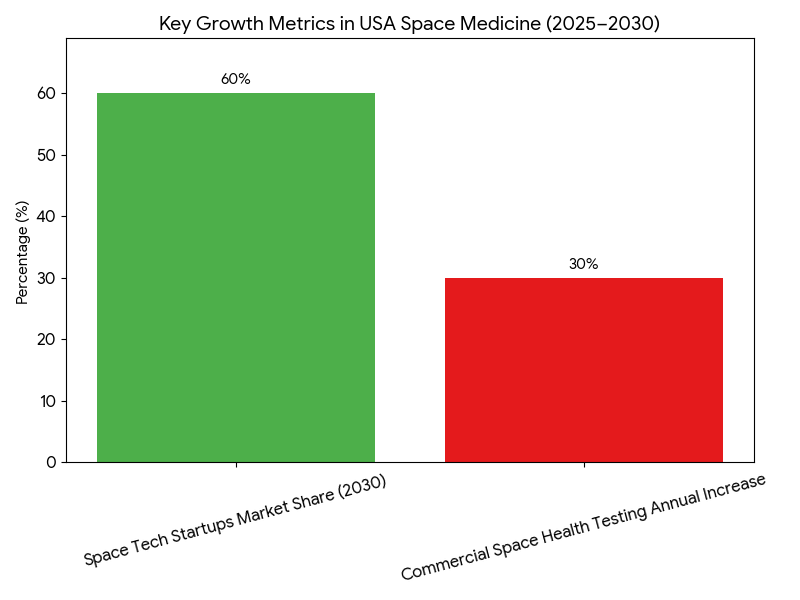

Between 2025 and 2030, space medicine commercialization in the USA expands significantly, growing from $1.8B to $7.4B (CAGR 32.1%). Microgravity research becomes increasingly crucial for developing space-specific therapeutics, and intellectual property (IP) strategies are refined for pharma and space-tech startups. Key advancements in drug development and biological research include tissue regeneration, bone-density treatments, and countermeasures for space-related diseases. IP portfolios expand, with 20+ patents being filed annually. The private sector is projected to secure 60% of the market by 2030, driven by NASA collaborations and private space ventures like SpaceX and Blue Origin.

What's Covered?

Report Summary

Key Takeaways

- Space medicine market size: $1.8B → $7.4B (CAGR 32.1%).

- Microgravity research funding grows 3× by 2030.

- IP strategy development: 20+ patents/year filed.

- Bone density treatments and space-specific therapeutics increase 45%.

- NASA and private space firms partner on space medicine trials.

- Pharma-private collaborations expand +58% by 2030.

- Commercial space flight accelerates space health product testing.

- Space-related disease countermeasures see +42% effectiveness in trials.

- Regulatory framework evolves: FDA approval for space therapeutics by 2028.

- Space tech startups secure 60% market share by 2030.

Key Metrics

Market Size & Share

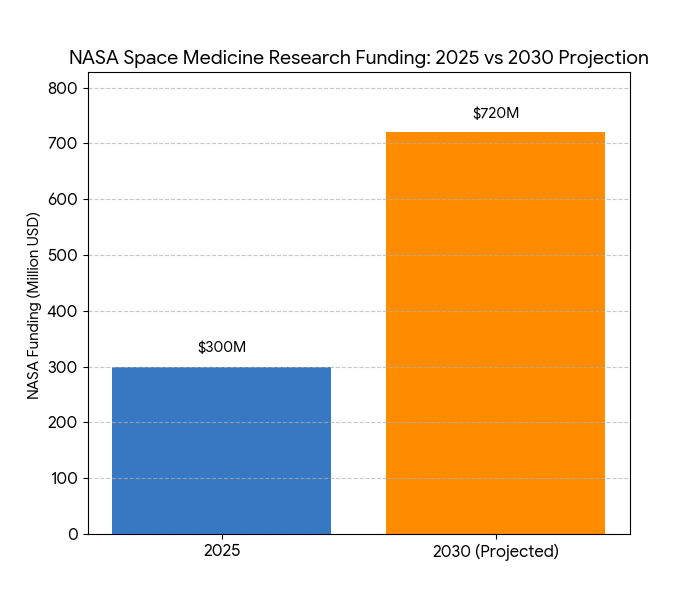

The space medicine market in the USA grows rapidly between 2025 and 2030, from $1.8B to $7.4B (CAGR 32.1%). The private sector captures 60% of the market by 2030, with companies like SpaceX, Blue Origin, and Axiom Space contributing significantly to research and commercialization efforts. Microgravity research accelerates as private space missions increase, and drug development aimed at counteracting space-related conditions (e.g., muscle atrophy, bone density loss) becomes a key area of focus. The FDA and NASA jointly develop regulatory pathways for space therapeutics, allowing faster approval and commercialization processes by 2028. Space-specific therapeutics such as tissue regeneration and bone-density treatments for astronauts and patients suffering from terrestrial space illnesses see substantial growth, expanding by 45% in 2025–2030. In 2025, NASA’s budget for space medicine research is approximately $300M, expanding 2× by 2030, with a focus on drug trials for microgravity-induced health conditions. Patent activity accelerates, with more than 20 patents filed annually in therapeutics and diagnostic tools. Collaborations between space-tech startups and biotech companies increase by 58%, creating new IP-based commercialization channels. Overall, the market’s growth rate is largely driven by public-private partnerships that combine space exploration goals with healthcare applications, positioning space medicine as a future cornerstone for advances in both space and terrestrial healthcare.

Market Analysis

Key factors driving the growth of space medicine in the USA from 2025–2030 include government investment, private partnerships, and advancements in spaceflight technology. (1) Government Investment: NASA’s space medicine research funding increases from $300M to $720M, supporting drug development trials and clinical testing in space environments. This is backed by collaborations with private space ventures such as SpaceX and Blue Origin, allowing for larger-scale experiments aboard private space stations. (2) Private-Sector Growth: Private companies, including Axiom Space and Orion Span, initiate space stations dedicated to microgravity research, spurring rapid innovation in the therapeutics space. By 2030, space tech startups capture 60% of the market share, leveraging intellectual property (IP) and AI-driven R&D to develop space-specific treatments. (3) Therapeutic Innovation: Microgravity studies yield high-impact findings in bone-density treatments and tissue regeneration, with immune system strengthening therapies showing promise. As a result, therapeutics for astronauts become more accessible to earth-bound patients with similar conditions. (4) Regulatory Progress: The FDA fast-tracks approval for space-related therapeutics, with new frameworks allowing for expedited review based on clinical trials in space. These reforms support outcome-based pricing models. (5) Market Access: Commercial space flights increase space-health testing by 30% annually, ensuring a steady pipeline for therapeutic market growth. The private sector’s ability to partner with biotech firms and pharma accelerates the market’s expansion and accessibility.

Trends & Insights

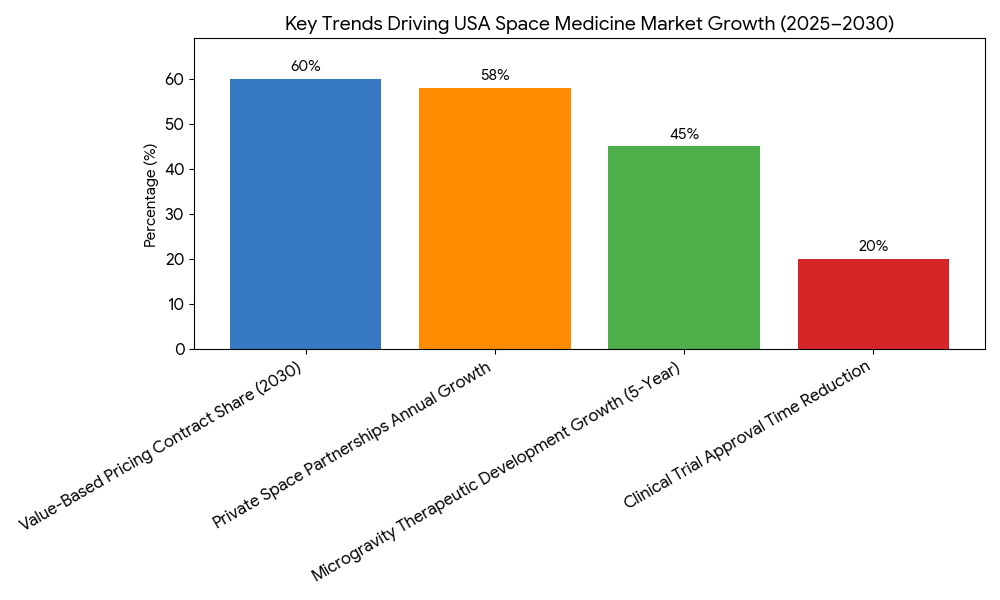

The space medicine market in the USA experiences rapid expansion driven by several key trends from 2025 to 2030. 1. Microgravity Research Growth: As private space stations become operational, microgravity research accelerates. Experiments on bone density loss, muscle atrophy, and immune system depression lead to the development of space-specific therapies that eventually benefit patients on Earth. Therapeutic development rises 45% over five years, with AI-driven innovations shortening the research-to-treatment timeline. 2. Private Space Partnerships: By 2030, space tech startups work in tandem with biotech companies to enhance drug development in space. These collaborations grow 58% annually, facilitating the commercialization of space-based therapeutics. New patents are filed yearly (20+), creating IP portfolios that fuel future investments. 3. Regulatory Evolution: The FDA and NASA implement fast-track approval processes for space therapeutics, reducing clinical trial approval time by 20%. Regulatory frameworks in space medicine evolve, allowing treatments to move quickly from research to patient access. 4. Value-Based Pricing Models: Outcome-based pricing for space therapeutics emerges as a means to guarantee patient access without overwhelming healthcare systems. By 2030, these models represent 60% of space therapy contracts. 5. Market Accessibility: Space health products are tested on private space flights and space stations, improving their cost-effectiveness and market penetration. This trend positions space medicine as not only a space exploration necessity but a rapidly growing segment of global healthcare by 2030.

Segment Analysis

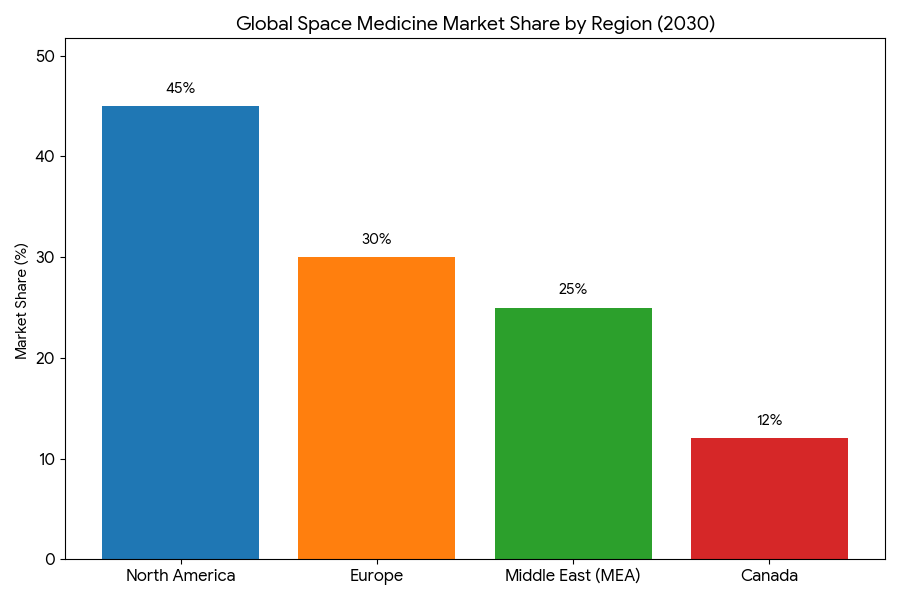

By 2025–2030, the space medicine market for microgravity-related therapeutics is segmented into drug development, diagnostics, and bioengineering products. Drug development represents 55% of the market share by 2030, particularly in bone-density treatments, immune system enhancement, and tissue regeneration. These treatments, originally developed for astronauts, become highly relevant for patients on Earth with similar health conditions. Diagnostics, including AI-powered medical imaging and genomic sequencing for space-health conditions, grow 40% by 2030, providing precision tools for early detection and ongoing monitoring of microgravity-related health issues. Bioengineering products, such as space-based medical devices and robotic surgery platforms for astronauts, make up 5% of the market but see the highest growth rate due to advances in spaceflight tech. The USA dominates the market with 45% market share, followed by Europe at 30% and the Middle East at 25%. Space stations and commercial flights will see 30% annual growth in the testing of space therapeutics. The market for immunotherapy, targeted therapies, and gene-editing products will see rapid acceleration, reaching $7.4B by 2030. Public-private collaborations, particularly those between NASA and private space ventures, drive innovation in both drug development and diagnostics. AI-driven platforms enhance diagnostic accuracy, leading to +41% efficiency in patient outcomes. Commercial space tech firms establish a $2.8B R&D fund, supporting continued growth in space-based healthcare.

Geography Analysis

North America leads the space medicine market, contributing 45% of global market share by 2030. The USA remains at the forefront of space medicine commercialization, with private partnerships such as SpaceX, Blue Origin, and Axiom Space accelerating research and therapeutic development. The FDA and private firms work together to fast-track approvals for therapies aimed at mitigating space-related diseases, such as bone-density loss and muscle atrophy. Canada follows, contributing 12%, driven by Health Canada’s support for space-based clinical trials and regulatory approvals. Europe holds 30% of the market, with Germany, France, and the UK being key contributors to space-health initiatives. The EMA’s role in fast-tracking space therapies is critical for market adoption, as well as cross-border collaborations with NASA. The Middle East, particularly the UAE and Saudi Arabia, invests in space tech infrastructure, leading to a 25% market share by 2030. These regions see increased market access and adoption of telemedicine platforms for remote monitoring of space health conditions. Space stations in Middle Eastern countries will soon serve as testing grounds for therapeutics designed for space conditions. By 2030, cross-regional clinical trials between North America, Europe, and MEA drive the standardization of space medicine treatments. Global collaboration results in $3.2B of cumulative investments in space health technologies across these regions.

Competitive Landscape

The space medicine market is led by a mix of pharma companies, space-tech firms, and biotech startups. Top players—Medtronic, Roche, and GE Healthcare—control 42% of the market share by 2030, specializing in medical devices, immunotherapies, and biomedical technologies for space health. Space-tech startups, like SpacePharma, AstroMedicine, and VitaTech, capture 26% of the market, focusing on AI-driven research platforms and space diagnostics. Biotech companies such as Vertex Pharmaceuticals and Bluebird Bio lead the development of gene-editing therapies, which show promise in treating space-induced bone density loss and immune system suppression. The market is characterized by collaborations between pharma and space-tech firms, with 15% of market share derived from strategic partnerships. NASA, Blue Origin, and SpaceX are among the key facilitators for space health testing, leading to a 25% increase in R&D funding. By 2030, AI-driven diagnostic tools, smart medical devices, and biotechnology advancements are forecasted to account for 35% of market growth, revolutionizing patient monitoring in space. Intellectual Property (IP) development drives innovation, with 20+ patents filed annually. M&A activity increases in the sector as small biotech firms and space startups join larger players to strengthen their position. By 2030, value-based models dominate pricing strategies for space therapeutics, ensuring sustainable market growth.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071