68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

UAE Diagnostic Ultrasound Market 2025–2034: USD 10.1 Billion to USD 20.3 Billion at 7.3% CAGR | Smart Hospitals & Preventive Screening Boost Adoption

The UAE diagnostic ultrasound market is projected to expand from USD 10.1 billion in 2025 to USD 20.3 billion by 2034, registering a CAGR of 7.3%. Growth is driven by the country’s smart hospital initiatives, rising preventive screening programs, and increasing adoption of portable and AI-enabled ultrasound systems. Favorable government policies under UAE Vision 2031, the expansion of specialty care centers, and the integration of AI diagnostic imaging into primary healthcare are boosting market penetration. With cardiology, obstetrics, oncology, and musculoskeletal imaging emerging as key applications, ultrasound systems are evolving from routine tools to core diagnostic assets across the UAE’s rapidly digitalizing healthcare ecosystem.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 10.1B (2025) to USD 20.3B (2034) at 7.3% CAGR.

- AI-powered diagnostic imaging adoption up 3× since 2022.

- Portable and handheld ultrasound devices to account for 28% of total sales by 2030.

- Preventive health screenings driving 22% of imaging demand.

- Cardiology and obstetrics collectively represent 45% of total ultrasound usage.

- Government spending on health AI expected to exceed USD 500M by 2030.

- Public-private partnerships (PPPs) accelerating smart hospital deployments.

- 3D/4D imaging systems forecasted to achieve 11% CAGR through 2034.

- Radiologist-to-population ratio improvements enabling faster diagnostics.

- Local AI startups emerging as key players in image interpretation software.

Key Metrics

Market Size & Share

The UAE diagnostic ultrasound market will double from USD 10.1 billion in 2025 to USD 20.3 billion by 2034, driven by population health screening, chronic disease monitoring, and digital healthcare expansion. The hospital segment contributes 58% of total demand, while diagnostic imaging centers account for 27%. The portable ultrasound segment, expanding at 11% CAGR, is gaining traction due to telemedicine integration and remote rural deployments. The cardiology and obstetrics sectors lead usage, representing 45% of overall scans. Government initiatives, including Emirates Health Services’ digital imaging roadmap, are accelerating the adoption of smart diagnostic ecosystems.

Market Analysis

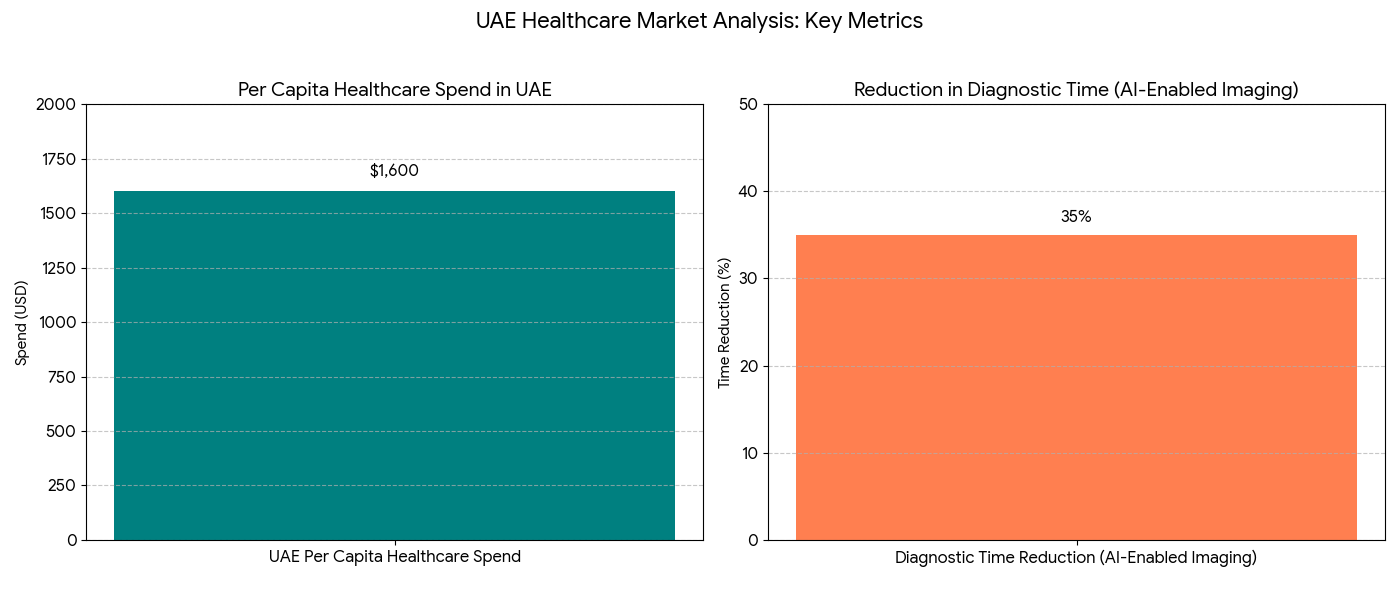

The UAE’s healthcare transformation agenda is central to the market’s expansion. With a per capita healthcare spend of USD 1,600, the UAE ranks among the top in MENA. The transition to AI-enabled imaging is redefining clinical efficiency, cutting diagnostic times by up to 35%. The introduction of handheld ultrasound systems for home and remote diagnostics is widening accessibility. Hospitals like Cleveland Clinic Abu Dhabi and Mediclinic are early adopters of AI-assisted ultrasound analysis. Additionally, PPP-led smart hospital projects under Vision 2031 are generating demand for advanced equipment, while radiology integration platforms are facilitating centralized, cloud-based image sharing across emirates.

Trends & Insights

- AI & Machine Learning: Enabling real-time image enhancement and automated anomaly detection.

- 3D/4D Imaging Boom: 11% CAGR in advanced obstetrics and cardiac imaging.

- Point-of-Care Diagnostics: Portable ultrasound adoption increasing in emergency and ICU settings.

- Preventive Care Expansion: Screening programs for cardiovascular and liver conditions boosting utilization.

- Data Interoperability: Integration with HL7 and FHIR platforms improving image accessibility.

- Government Vision Alignment: UAE Vision 2031 promoting AI-based healthcare infrastructure.

- Training Initiatives: Emiratization programs increasing the number of skilled radiologists.

- Public-Private Collaboration: 35+ PPP-led hospital expansions by 2030.

- Smart Imaging Platforms: AI cloud solutions allowing faster triage and cross-specialty access.

- Value-Based Healthcare: Hospitals shifting toward outcome-based procurement of ultrasound systems.

Segment Analysis

By product, cart-based ultrasound systems hold 60% share, followed by portable (28%) and handheld (12%) solutions. Portable systems are the fastest-growing segment, offering affordability and mobility. By application, obstetrics & gynecology (25%), cardiology (20%), oncology (15%), musculoskeletal (12%), and abdominal imaging (10%) dominate use cases. Hospitals and diagnostic centers collectively account for 85% of total installations. 3D/4D and Doppler imaging systems are projected to lead the premium equipment segment, while AI-assisted reporting tools will enhance utilization across outpatient clinics and telemedicine providers.

Geography Analysis

Dubai (45%), Abu Dhabi (35%), and Sharjah (10%) drive the majority of the market, with the remainder distributed across Ajman, Ras Al Khaimah, and Fujairah. Dubai Healthcare City and Abu Dhabi’s SEHA network serve as technology adoption hubs, piloting AI diagnostic imaging projects with vendors like GE Healthcare and Philips. Northern Emirates are experiencing increased portable ultrasound penetration for primary and maternal health programs. The UAE’s position as a regional medical tourism hub further supports imaging volume growth, especially in preventive and cardiac diagnostics.

Competitive Landscape

Key market players include GE Healthcare, Philips, Siemens Healthineers, Canon Medical, Samsung Medison, Mindray, and Fujifilm Sonosite. GE and Philips dominate premium cart-based ultrasound segments, while Mindray and Samsung Medison lead portable deployments. Siemens Healthineers and Canon Medical are investing in AI-assisted imaging and cloud-based archiving solutions tailored for UAE smart hospitals. Local firms, such as Gulf Drug LLC and Mediserv, are partnering with global OEMs to enhance distribution and service capacity. Emerging startups specializing in AI-driven diagnostic analytics, like InstaScan AI, are adding value through cloud-enabled interpretation tools, aligning with the UAE’s vision for a fully digital and preventive healthcare ecosystem.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071