68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

United States Brain–Computer Interface Market 2025–2034: USD 1.6 Billion Growing to USD 6.3 Billion at 16.4% CAGR | Neural Implants, AI Integration & Assistive Technologies Drive Growth

The U.S. Brain–Computer Interface (BCI) market is forecast to expand from USD 1.6 billion in 2025 to USD 6.3 billion by 2034, registering a CAGR of 16.4%. The market’s acceleration is driven by rapid advances in neural implant technologies, AI-powered decoding algorithms, and assistive neuroprosthetics aimed at improving mobility and cognitive function. With rising investments from both biotech innovators and tech giants such as Neuralink, Synchron, and Meta Reality Labs, the U.S. is leading global BCI commercialization. Government support through NIH and DARPA-funded programs, combined with the FDA’s evolving neurodevice approval frameworks, positions the nation at the forefront of human–AI integration and neurotech scalability.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 1.6B (2025) to USD 6.3B (2034) at 16.4% CAGR.

- Neural implants and invasive BCIs to represent 58% of market revenue by 2034.

- AI-enabled signal decoding to improve accuracy by >35% over legacy systems.

- Assistive BCIs for paralysis and ALS patients driving USD 1.2B annual demand.

- Non-invasive EEG headsets expected to grow at 18% CAGR through 2034.

- Defense and research funding exceeding USD 2.5B under DARPA’s neurotechnology initiatives.

- Clinical trials and FDA clearances for implantable BCIs to double by 2030.

- Neural data privacy regulation frameworks under development by 2027.

- Neurorehabilitation and gaming interfaces to contribute USD 900M by 2034.

- AI–BCI convergence fueling development of real-time cognitive feedback systems.

Key Metrics

Market Size & Share

The U.S. BCI market is projected to grow from USD 1.6 billion in 2025 to USD 6.3 billion by 2034, underpinned by growing adoption in healthcare, research, and defense sectors. Invasive BCIs, led by neural implant developers like Neuralink, Blackrock Neurotech, and Synchron, will contribute 58% of total market revenue. Non-invasive EEG-based BCIs will gain momentum in gaming, education, and neurofeedback training. The healthcare domain—particularly assistive and neurorehabilitation applications will drive USD 1.2B annual demand by 2030. As AI integration enhances decoding fidelity and response latency, the market is transitioning from experimental to commercially scalable solutions.

Market Analysis

The rapid evolution of the U.S. BCI landscape reflects convergence between neuroscience, AI, and biomedical engineering. Between 2025 and 2034, over 40% of R&D investments will target AI-driven neural decoding, electrode miniaturization, and wireless transmission systems. DARPA’s Next-Generation N3 Program and NIH’s BRAIN Initiative are key funding pillars, collectively investing USD 2.5B+ into neurotechnology research. The assistive segment including implantable BCIs for motor restoration and communication will remain dominant, while non-invasive consumer BCIs gain mainstream attention in gaming and AR/VR applications. FDA fast-track pathways for implantable devices are shortening approval times by 30–40%, accelerating commercialization.

Trends & Insights

- Neural Implant Breakthroughs: Fully implantable devices enabling real-time bidirectional brain communication.

- AI Integration: Deep learning models decoding motor intent with >95% precision in clinical trials.

- Wearable EEG Expansion: Consumer-grade BCIs for wellness and neurofeedback training gaining traction.

- Assistive Tech Revolution: BCIs enabling paralyzed users to control prosthetics and digital interfaces.

- Defense Investment Surge: DARPA funding combat-ready cognitive augmentation systems.

- Neurodata Ethics: Emerging “mental privacy” standards to regulate data ownership.

- Neuro-Gaming: Gaming sector adopting BCIs for mind-controlled AR/VR experiences.

- Miniaturization: Advancements in biocompatible electrodes reducing surgical risks.

- Cloud Integration: Real-time neural data synchronization enabling tele-neurology services.

- Interoperability Challenges: Standardization efforts to unify data protocols across BCI systems.

Segment Analysis

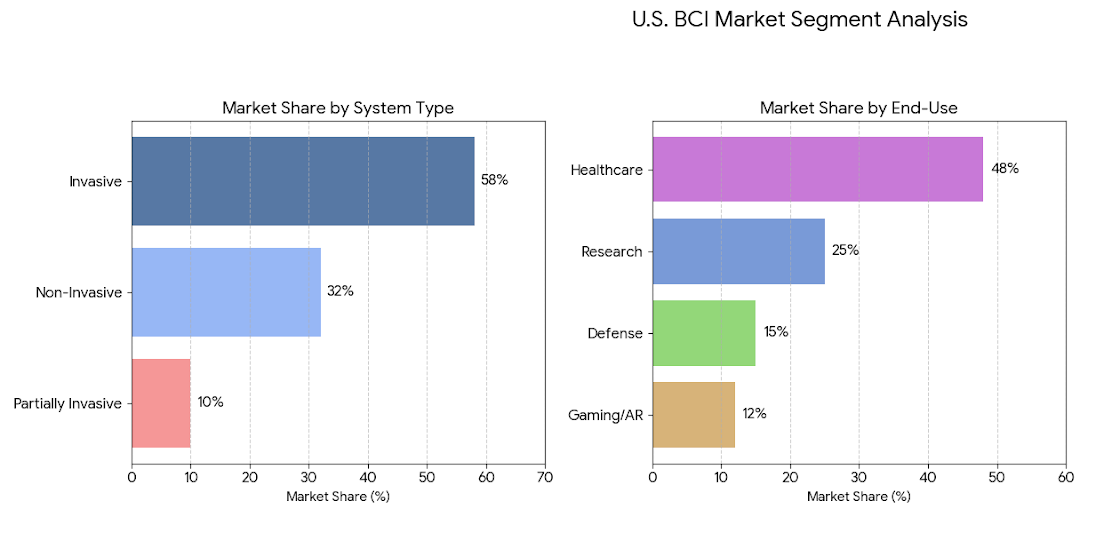

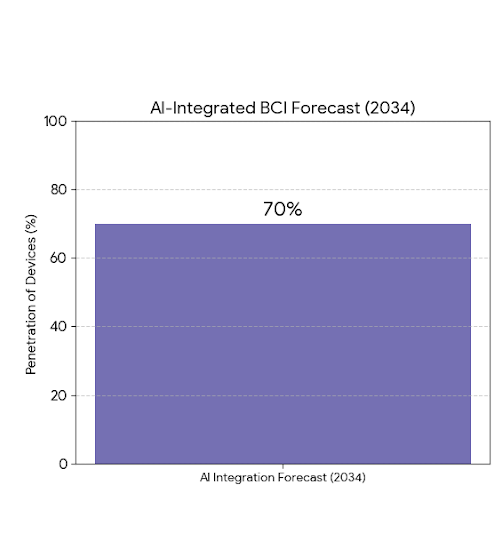

The U.S. BCI market divides into invasive, partially invasive, and non-invasive systems. Invasive BCIs (58%) dominate due to their superior signal quality and therapeutic relevance, particularly in motor rehabilitation and sensory restoration. Non-invasive BCIs (32%), mainly EEG and fNIRS-based, are expanding in consumer and research applications, while partially invasive systems (10%) serve clinical testing and hybrid interfaces. By end-use, healthcare (48%) leads, followed by research (25%), defense (15%), and gaming/AR (12%). AI-integrated BCIs, expected to represent 70% of devices by 2034, will blur the lines between neural decoding, cloud analytics, and behavioral prediction.

Geography Analysis

Within the U.S., California, Massachusetts, and Texas dominate due to concentrated R&D ecosystems. California leads, housing Neuralink, Paradromics, and Synchron’s U.S. base, contributing nearly 38% of national investment. Boston and Houston remain hubs for academic neuroengineering research through MIT, Harvard, and Rice University collaborations. Federal programs under NIH and DARPA allocate over USD 1B annually across academic and defense innovation centers. As FDA-approved trials expand nationwide, Midwestern states like Illinois and Minnesota are emerging in neurodevice manufacturing, supporting large-scale commercialization and export capability.

Competitive Landscape

Major players include Neuralink, Synchron, Blackrock Neurotech, Kernel, Paradromics, NextMind, Emotiv, and Cognixion. Neuralink leads with deep-implantable electrodes for high-bandwidth brain–machine communication, while Synchron pioneers minimally invasive stentrode implants. Blackrock Neurotech dominates research-grade implants, and Kernel focuses on non-invasive neuroimaging BCIs. Emotiv and NextMind cater to consumer EEG systems, bridging entertainment and neurofeedback markets. Big tech entities like Meta, Apple, and Google are investing in neural signal interpretation and AR/VR integration. Competitive strategies center on AI training datasets, FDA fast-tracking, and miniaturization, setting the stage for the U.S. to lead the global neurotech commercialization wave through 2034.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071