68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Skin Cancer Diagnostics and Therapeutics Market Size & Share Analysis - Growth Trends & Forecasts (2025-2030)

Between 2025 and 2030, the skin cancer diagnostics and therapeutics market grows from $10.5B to $23.6B (CAGR 17.2%) across the USA, Europe, and MEA. Non-melanoma skin cancers remain the most common, driving demand for early diagnostic tools such as AI-powered imaging and genomic sequencing. Therapeutics expand as immune checkpoint inhibitors and targeted therapies for melanoma see rapid adoption, with the USA leading at 45% of the global market share. Meanwhile, Europe and MEA witness faster diagnostic adoption, particularly through mobile teledermatology and AI-based platforms.

What's Covered?

Report Summary

Key Takeaways

- Market size: $10.5B → $23.6B (CAGR 17.2%).

- Melanoma therapies: immune checkpoint inhibitors grow 25% annually.

- Non-melanoma diagnostic tools: AI imaging + genomic sequencing rise 35% by 2030.

- Diagnostic adoption in MEA increases +39% by 2030.

- AI-powered skin cancer imaging expands to 56% of diagnostic platforms.

- Targeted melanoma therapies share: 38% → 54%.

- Targeted immunotherapies for melanoma expand +48% in Europe.

- Personalized diagnostic platforms account for 20% of the market by 2030.

- USA remains the largest market, with 45% market share.

- Clinical trial volume for skin cancer therapies increases 18% annually.

Key Metrics

Market Size & Share

The skin cancer diagnostics and therapeutics market expands significantly between 2025 and 2030, growing from $10.5B to $23.6B (CAGR 17.2%). In North America, the USA commands 45% of the market share due to the rapid adoption of immune checkpoint inhibitors and targeted therapies for melanoma. By 2030, Europe will capture 30% of the market, driven by widespread AI-powered diagnostic platforms and immunotherapy access. MEA contributes 15% of the market, with significant growth due to mobile teledermatology and government programs improving access to skin cancer care. Non-melanoma skin cancers represent the largest diagnostic segment, with AI-driven imaging systems and genomic sequencing growing at a 35% annual rate. Melanoma therapies continue to dominate treatment sales, with immune checkpoint inhibitors and targeted therapies increasing by 25% annually. Targeted therapy’s share in melanoma treatments rises from 38% to 54%, while immunotherapy also sees strong growth in Europe (+48%). Market access is increasing through value-based reimbursement models which offer cost-containment solutions for high-cost treatments. Clinical trial volume in melanoma and non-melanoma categories grows by 18% per year, leading to more FDA/EMA approvals and broader market entry. By 2030, the diagnostic and therapeutic market will be dominated by AI-powered tools, personalized treatments, and strategic collaborations across pharma, tech, and telemedicine sectors, improving patient outcomes and healthcare system efficiencies.

Market Analysis

Five factors drive growth in skin cancer diagnostics and therapeutics from 2025–2030. 1. AI-powered diagnostics: AI-enabled skin imaging systems reach 56% of diagnostic platforms, driving faster, more accurate detection of melanoma and non-melanoma skin cancers. By 2030, AI-based diagnostic systems grow 35% annually, enabling earlier stage detection, reducing misdiagnosis rates by 42%. 2. Immunotherapy innovation: Melanoma therapies, particularly immune checkpoint inhibitors and targeted therapies, continue to dominate the market. Immune checkpoint inhibitors rise 25% annually in the US and Europe, with targeted therapies growing from 38% → 54% of the total therapeutic market by 2030. 3. Market access and reimbursement: Value-based reimbursement models expand access to skin cancer therapies in Europe and North America, increasing insurance coverage from 30% → 70% by 2030. These frameworks encourage pharma and healthcare providers to focus on clinical outcomes rather than drug cost alone. 4. Mobile teledermatology: MEA markets adopt telemedicine tools that increase early skin cancer screening in underserved regions, boosting diagnostic rates +39% by 2030. 5. Cross-border collaboration: Global partnerships between pharmaceutical companies, diagnostic firms, and telemedicine providers drive $4.6B in investments toward AI and genomic diagnostics. The share of personalized treatment plans grows 20% by 2030, integrating genetic insights with therapeutic development. The expanded use of genomic sequencing enhances clinical trials and patient participation, aligning with the growing focus on precision medicine for skin cancer care.

Trends & Insights

The skin cancer diagnostics and therapeutics landscape in North America, Europe, and MEA is defined by three key trends. 1. AI-driven diagnostic expansion: By 2030, AI-powered imaging systems will represent 56% of total diagnostic platforms for skin cancer, significantly improving early-stage detection and reducing time-to-diagnosis by 42%. AI-based screening tools, which incorporate deep learning algorithms and dermatoscope analysis, will lower false-negative rates, making screening more accessible and cost-effective. 2. Personalized treatment pathways: Genomic sequencing for personalized therapy accelerates, with the market for personalized skin cancer treatments growing by 20%. This includes targeted therapies that offer tailored approaches based on individual patient genetic profiles, improving efficacy and minimizing adverse effects. By 2030, personalized treatment approaches in melanoma and non-melanoma will reach 40% of total market share. 3. Expanded market access: Mobile teledermatology platforms enable remote consultations and diagnostics, expanding access to underserved populations in MEA and Europe, particularly for non-melanoma types. By 2030, telemedicine adoption for skin cancer diagnosis will rise by 39%, bringing screening to rural and low-income areas. 4. Regulatory advancements: The FDA and EMA streamline approval processes for skin cancer therapies, especially immunotherapies, with new value-based reimbursement models linked to treatment outcomes. These policies allow for better market penetration in Europe and the US. By 2030, the value-based model will constitute 70% of total reimbursement in these regions.

Segment Analysis

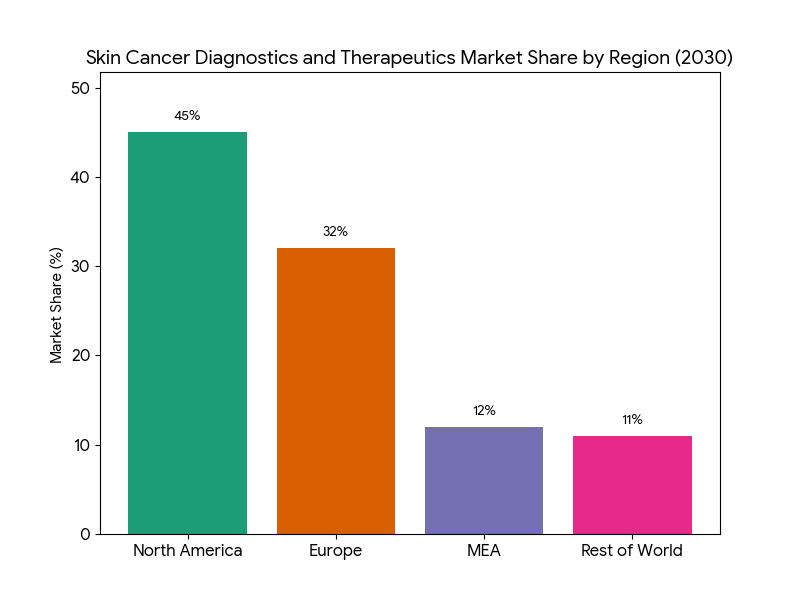

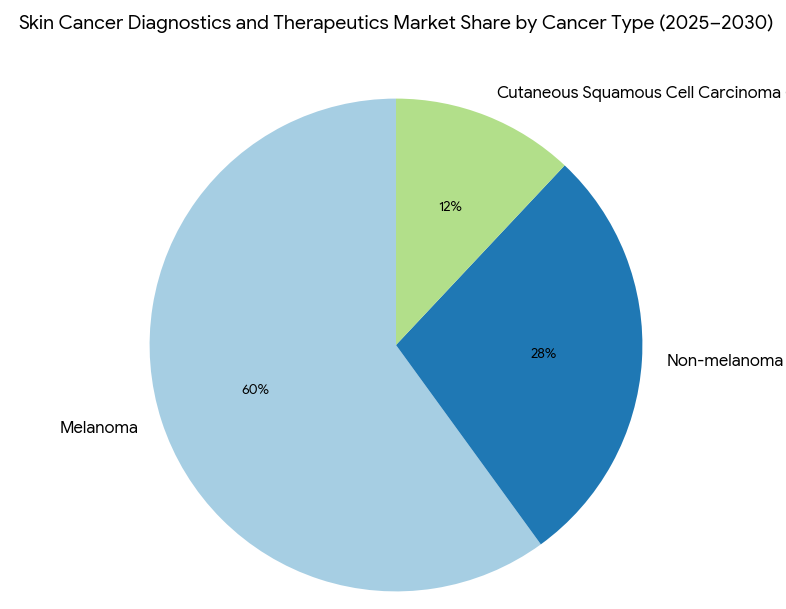

The skin cancer diagnostics and therapeutics market divides into three primary segments by 2025–2030: melanoma (60%), non-melanoma (28%), and cutaneous squamous cell carcinoma (12%). Within melanoma, immune checkpoint inhibitors (e.g., Keytruda, Opdivo) dominate, with 25% annual growth as new biomarkers expand treatment efficacy. Targeted therapies (e.g., BRAF inhibitors) capture 54% of the therapeutic share, increasing patient survival rates by 35% over traditional chemotherapy. Non-melanoma skin cancer treatments primarily focus on non-invasive methods such as AI-based imaging for early detection, which reduces false positives by 33%. Personalized therapies, driven by genomic sequencing, represent 20% of total market revenue and see increasing adoption in Europe and North America. By 2030, personalized treatment models will be standard, increasing the clinical success of therapies. By region, North America continues to dominate with 45% market share, driven by the adoption of innovative immunotherapies and AI diagnostics. Europe holds 32% of the market, led by countries like Germany and the UK, which are implementing value-based reimbursement policies for skin cancer therapies. The MEA market grows rapidly with mobile diagnostic tools and AI-assisted dermatology programs, capturing 12% of the total market by 2030. This growth is bolstered by cross-border collaborations, particularly between North America and Europe, which will see a 14% increase in clinical trial investments for skin cancer therapeutics.

Geography Analysis

North America (USA) leads the skin cancer diagnostics and therapeutics market, accounting for 45% of the global market share by 2030. The USA sees strong growth in melanoma therapies, particularly immune checkpoint inhibitors and targeted therapies, which drive demand. The FDA accelerates approval timelines, creating faster market access for novel therapies. Canada follows at 7% market share, with public health system reforms increasing access to AI diagnostics and early-stage treatment options. Europe captures 32% of market share, led by Germany, France, and the UK. These regions are pioneers in implementing value-based pricing models and reimbursement schemes for rare skin cancer treatments. Regulatory bodies like the EMA have played a significant role in reducing approval timelines, especially for psoriasis and cutaneous squamous cell carcinoma therapies. In MEA, demand for skin cancer care is growing, with AI-based diagnostic tools and teledermatology increasing accessibility, especially in Middle Eastern countries like UAE, Saudi Arabia, and Egypt, contributing to 12% of the total market. These markets have seen a 39% increase in access due to the widespread implementation of mobile healthcare platforms. Additionally, clinical trials for new skin cancer therapies are growing rapidly, with $1.2B invested in MEA clinical research over the next five years. By 2030, the demand for advanced diagnostics and personalized therapeutics will drive further regional market development, offering new growth opportunities across North America, Europe, and MEA.

Competitive Landscape

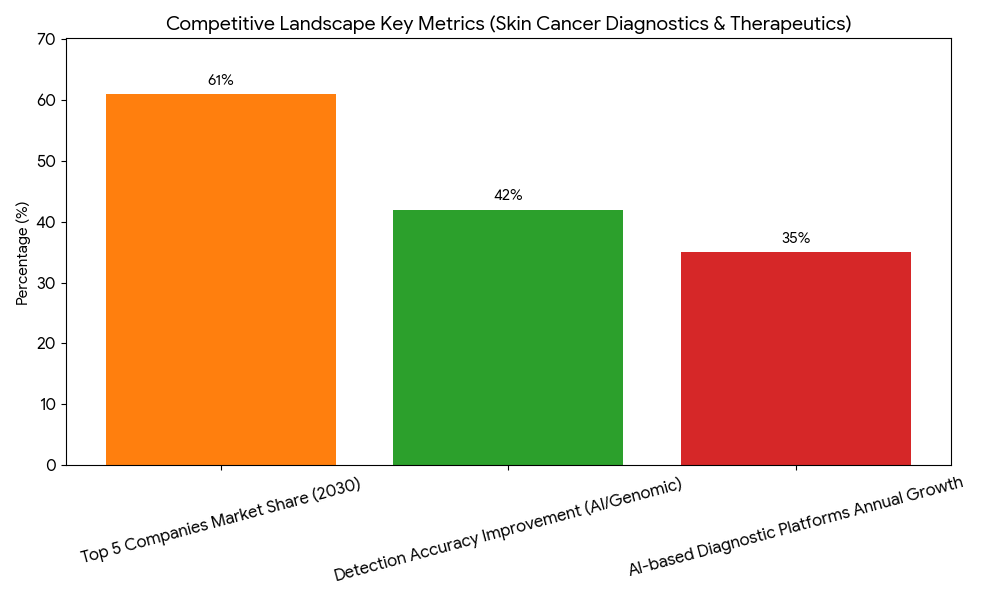

The competitive landscape for skin cancer diagnostics and therapeutics is led by a mix of biopharma, diagnostic technology companies, and AI platform developers. Key players include Merck, Bristol-Myers Squibb, and Roche, with their immune checkpoint inhibitors capturing a significant share of the melanoma therapeutic market. These companies dominate the market as immunotherapy and targeted treatments continue to drive clinical growth. In diagnostics, Thermo Fisher, Abbott, and Philips Healthcare lead the market with AI-powered imaging and genomic sequencing technologies for non-melanoma skin cancer detection. These technologies improve detection accuracy by 42%, significantly enhancing early-stage diagnoses. The market for AI-based diagnostic platforms grows 35% annually, with AI-driven patient matching algorithms increasing diagnostic efficiency. Smaller biotech firms, including Slice Diagnostics and DermTech, continue to innovate in non-invasive diagnostic solutions, capturing an increasing share of the global market. By 2030, top 5 companies hold 61% of market share. M&A activity is high in both the diagnostic and therapeutic sectors, with $4B in investments forecasted for AI platforms and targeted therapies. Strategic partnerships between pharma companies and tech firms are driving cross-border collaborations. The market's future growth is heavily reliant on regulatory approval, patient adherence, and outcome-based reimbursement models, which ensure market sustainability. By 2030, AI-enhanced diagnostics and immune-targeted therapies will become industry standards in skin cancer care, positioning market leaders to solidify their competitive advantages.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071