68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

SEPA Instant & European Real-Time Payments: Cost Savings, Interoperability & Revenue Models

This research explores SEPA Instant Payments and European real-time payments from 2025 to 2030, focusing on cost savings, interoperability, and revenue models. The report highlights how instant payment systems enhance cross-border transactions, reduce costs, and foster greater financial inclusion. It examines payment infrastructure, regulatory challenges, and the evolving revenue models associated with real-time payments. The study provides insights into how financial institutions, payment service providers, and merchants can leverage instant payments to improve operational efficiency and optimize revenue streams.

What's Covered?

Report Summary

Key Takeaways

- SEPA Instant Payments market in Europe projected to grow from €1.3 billion in 2025 to €7.5 billion by 2030, CAGR 43%.

- Cost savings from SEPA Instant Payments projected to reach €3 billion annually by 2030, driven by reduced transaction processing costs.

- Real-time payments adoption in Europe expected to cover 60% of transactions by 2030, up from 30% in 2025.

- Cross-border interoperability of real-time payment systems expected to improve by 40% by 2030.

- Revenue models based on instant payments will generate €1.5 billion annually by 2030 through transaction fees, merchant services, and premium services.

- Instant payment transactions expected to reduce payment processing time by 80% by 2030.

- Payment service providers (PSPs) will experience 30% reduction in operating costs by adopting SEPA Instant Payments.

- Mobile payments are expected to make up 40% of real-time transactions by 2030, driven by consumer demand for faster, more convenient payment methods.

- Institutional adoption of SEPA Instant payments is projected to account for 70% of market share by 2030.

- ROI from real-time payment systems expected to be 15–20% by 2030, driven by efficiency and revenue generation.

Key Metrics

Market Size & Share

The SEPA Instant Payments market in Europe is projected to grow from €1.3 billion in 2025 to €7.5 billion by 2030, with a CAGR of 43%. The real-time payment adoption in Europe is expected to cover 60% of transactions by 2030, up from 30% in 2025, driven by increasing demand for faster and more secure payment methods. SEPA Instant Payments will significantly reduce transaction processing costs, generating €3 billion annually in cost savings for financial institutions by 2030. Cross-border interoperability of real-time payment systems is projected to improve by 40%, helping to streamline payments across multiple EU jurisdictions and boost financial inclusion. Revenue models based on instant payments, such as transaction fees and merchant services, are expected to generate €1.5 billion annually by 2030. Payment service providers (PSPs) will reduce operating costs by 30% by integrating SEPA Instant Payments into their offerings. Transaction processing time is projected to be reduced by 80%, making real-time payments significantly faster and more efficient than traditional payment methods. Institutional adoption will drive the bulk of the market, with 70% of market share expected to be captured by financial institutions by 2030. Overall, SEPA Instant Payments will revolutionize the European payment landscape, driving substantial growth in the market.

.png)

Market Analysis

The real-time payments market in Europe is projected to expand rapidly, with SEPA Instant Payments growing from €1.3 billion in 2025 to €7.5 billion by 2030, reflecting a CAGR of 43%. By 2030, 60% of all transactions in Europe will be processed through instant payments, offering faster, more secure, and cost-efficient solutions. SEPA Instant Payments will create significant cost savings for financial institutions, with €3 billion annually saved in transaction processing costs. Cross-border interoperability between payment systems will improve by 40% by 2030, enabling seamless integration of instant payment solutions across EU jurisdictions. Revenue models will evolve with SEPA Instant Payments, generating €1.5 billion annually from transaction fees, merchant services, and premium services. Mobile payments will account for 40% of real-time transactions by 2030, driven by the rise of consumer demand for faster payment options and mobile-first solutions. Financial institutions will adopt real-time payment systems to reduce operational costs by 30%, enabling more efficient payment processing. Institutional adoption is expected to account for 70% of market share by 2030, with banks and PSPs leading the way in SEPA Instant Payment integration. Overall, real-time payments will provide significant ROI for the industry, improving transaction speed, reducing costs, and driving cross-border collaboration.

Trends & Insights

The SEPA Instant Payments market in Europe is projected to grow rapidly, from €1.3 billion in 2025 to €7.5 billion by 2030, with a CAGR of 43%. Key trends driving this growth include increasing adoption of real-time payments, with 60% of all transactions in Europe expected to be processed via instant payments by 2030. SEPA Instant Payments will generate €3 billion in annual cost savings for financial institutions by reducing transaction processing costs and improving efficiency. The growing demand for faster payments, coupled with cross-border interoperability, will drive real-time payments adoption, improving payment systems across the EU. Revenue models will evolve, with €1.5 billion annually generated from transaction fees, merchant services, and premium services by 2030. Mobile payments will account for 40% of transactions by 2030, further accelerating the adoption of real-time payments in consumer markets. PSPs are projected to reduce operating costs by 30% through SEPA Instant Payments integration. Cross-border compliance will improve by 40%, enabling greater financial security across the EU. Institutional investors will drive 70% of market share by 2030, reflecting the increasing adoption of instant payment systems by large financial institutions. ROI for these solutions is expected to be 15–20% by 2030, as operational costs decline and payment processing speeds improve.

.png)

Segment Analysis

The SEPA Instant Payments market in Europe is segmented by institution type, payment processing method, and geography. Financial institutions, particularly banks, fintech firms, and payment service providers (PSPs), will drive adoption, accounting for 70% of the market share by 2030. Banks will lead adoption of SEPA Instant Payments, particularly for cross-border transactions, as interoperability between payment systems improves by 40%. Transaction fees, merchant services, and premium services will generate €1.5 billion annually by 2030, providing new revenue streams for financial institutions. The segment of mobile payments will grow rapidly, accounting for 40% of all real-time transactions by 2030, driven by consumer demand for instant payment capabilities via smartphones. Transaction processing time will reduce by 80%, improving payment efficiency and customer satisfaction. Cost savings from SEPA Instant Payments will reach €3 billion annually by 2030, reducing the operational burden on financial institutions. The ROI for RegTech-enabled real-time payments is projected at 15–20% by 2030, driven by lower costs, faster transactions, and more seamless payment experiences across the EU. Institutional investors will be the major adopters of SEPA Instant Payments as the technology matures.

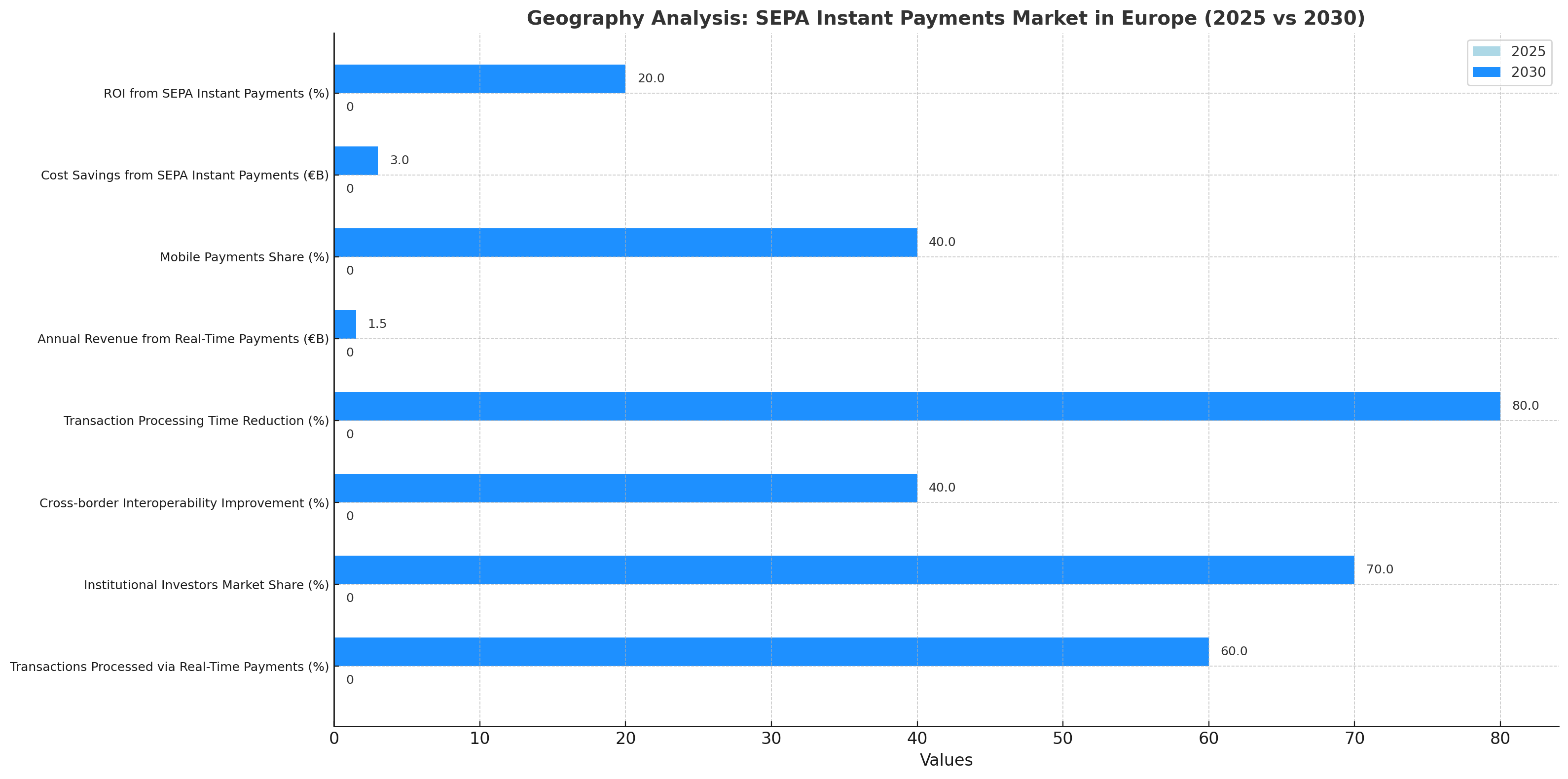

Geography Analysis

The SEPA Instant Payments market in Europe is projected to expand rapidly, with 60% of all transactions in Europe processed through real-time payments by 2030. Germany, France, and the UK will be the key markets for adoption, with institutional investors driving 70% of market share by 2030. Cross-border interoperability will improve by 40%, enabling seamless integration of instant payment systems across EU jurisdictions. Transaction processing time will be reduced by 80%, making SEPA Instant Payments an attractive option for both financial institutions and merchants. Revenue models based on real-time payments, including transaction fees and merchant services, are projected to generate €1.5 billion annually by 2030. Mobile payments will account for 40% of transactions in Europe by 2030, as consumers increasingly adopt instant payment solutions via smartphones. Cost savings from SEPA Instant Payments will amount to €3 billion annually by 2030, as operational costs are reduced. ROI from SEPA Instant Payments adoption is expected to reach 15–20% by 2030, driven by improved operational efficiency, faster payment processing, and increased customer satisfaction.

Competitive Landscape

The SEPA Instant Payments market in Europe is highly competitive, with major players including Finastra, Aci Worldwide, and SWIFT providing payment processing solutions for banks and payment service providers (PSPs). These companies will continue to dominate the market, as they enable instant payments, cross-border interoperability, and real-time transaction processing. Financial institutions, fintech companies, and large banks will account for 70% of the market share by 2030, as SEPA Instant Payments drive down transaction costs and increase operational efficiency. Revenue models for instant payments, including transaction fees and merchant services, are expected to generate €1.5 billion annually by 2030. The ROI for SEPA Instant Payments adoption is expected to be 15–20% by 2030, driven by cost reductions, increased revenue streams, and faster, more efficient transactions. Mobile payments will play an increasing role, with 40% of transactions being processed via mobile devices by 2030. Cost savings from SEPA Instant Payments are projected to total €3 billion annually, providing institutions with more resources for investment and innovation. Partnerships between fintechs and traditional financial institutions will fuel the next phase of innovation in real-time payment systems.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071