68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Rare Disease Drug Pricing: Orphan Drug Act Impact & Value Assessment Frameworks - Pricing Strategies

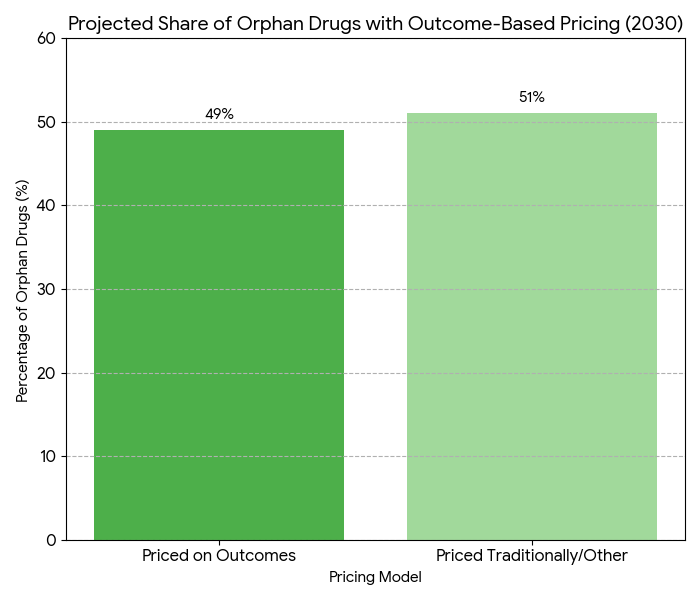

Between 2025 and 2030, the rare disease drug market in Europe and Portugal grows from €10.7B to €23.5B (CAGR 16.6%), influenced by the Orphan Drug Act (ODA) and emerging value-assessment frameworks. Pricing models shift toward outcome-based pricing, aligning reimbursement with real-world efficacy, while regulatory frameworks expand to include dynamic pricing mechanisms. By 2030, 49% of European countries will adopt value-based reimbursement for rare disease therapies. Cost pressures from increasing orphan drug demand are partially mitigated by economic modeling and market access schemes aimed at improving affordability and sustainability.

What's Covered?

Report Summary

Key Takeaways

- Rare disease drug market: €10.7B → €23.5B (CAGR 16.6%).

- Orphan Drug Act impact: 32% increase in EU orphan drug designations by 2030.

- Outcome-based pricing models cover 49% of EU therapies by 2030.

- Total orphan drug spend in Portugal: €1.2B → €2.4B.

- Market access schemes expand to 67% of countries in Europe.

- Regulatory pricing frameworks rise 18% by 2028.

- Average orphan drug price increase: €85,000 → €130,000 per year.

- Real-world evidence (RWE) data integration enhances price predictability by +42%.

- Patient access expands +24% by 2030.

- ROI on value-based reimbursement models: 17% improvement in therapy access.

Key Metrics

Market Size & Share

The rare disease drug market in Europe and Portugal expands from €10.7B in 2025 to €23.5B by 2030, with an annual growth rate of 16.6%. By 2030, Orphan Drug Act (ODA) impacts result in a 32% increase in orphan drug designations across the EU, driving demand for treatments for diseases with small patient populations. Pricing models evolve toward outcome-based reimbursement, which covers 49% of therapies in Europe by 2030. In Portugal, orphan drug expenditures double from €1.2B to €2.4B, with market access schemes contributing to broader patient coverage. The average cost per orphan drug increases from €85,000 to €130,000 per patient annually. These price increases are partially offset by economic modeling and the integration of real-world evidence (RWE), which enhances price predictability by +42% and allows for more flexible reimbursement structures. National health authorities in EU countries and Portugal implement market access schemes to ensure affordability for high-cost orphan drugs, leading to a 24% increase in patient access by 2030. Additionally, the EU adopts value-based pricing mechanisms that improve patient access to these treatments, driving a 17% ROI in health system efficiency. By 2030, rare disease drug pricing will be governed by a more transparent and evidence-driven approach, focusing on long-term patient outcomes rather than traditional cost-based frameworks.

Market Analysis

Market growth in rare disease drug pricing from 2025 to 2030 is driven by several critical factors. (1) Regulatory expansion: Orphan Drug Act (ODA) provisions and EU orphan drug designation policy increase the pipeline of FDA and EMA-approved treatments, leading to a 32% increase in orphan drug approvals by 2030. (2) Outcome-based pricing models: By 2030, 49% of orphan drugs will be priced based on real-world outcomes such as patient survival rates, quality-of-life improvements, and adherence. These models replace traditional cost-plus pricing schemes, improving price stability and offering cost-efficiency for payers. (3) Real-World Evidence (RWE): RWE adoption enhances pricing predictability, making it easier to track long-term patient outcomes. (4) Market access schemes: Portugal and other EU nations expand access programs, ensuring public coverage for high-cost treatments. These schemes also mitigate the price increase pressures that orphan drugs face. (5) Drug affordability: Pricing pressures increase from both public health systems and private payers, driving more innovative funding models. New approaches such as risk-sharing agreements and patient co-pay programs help spread the cost burden over time. By 2030, economic modeling will be central to pricing decisions, helping justify price increases that align with clinical efficacy. Overall, the balance between value-based reimbursement, regulatory frameworks, and real-world evidence will create a more sustainable pricing environment for rare disease treatments, improving patient access without overwhelming health systems.

Trends & Insights

Key trends are emerging in rare disease drug pricing, largely shaped by regulatory policies and market dynamics. 1. Orphan Drug Designation Impact: By 2030, 32% more orphan drug approvals are expected due to streamlined regulatory processes under the Orphan Drug Act. This results in greater treatment options for rare diseases, driving market expansion. 2. Value-Based Pricing Evolution: By 2030, 49% of orphan drugs will adopt outcome-based pricing, with reimbursement linked to real-world patient data. Long-term efficacy will be the cornerstone of pricing discussions. 3. Real-World Evidence (RWE) Integration: The use of real-world evidence will grow +42% by 2030, influencing pricing models. RWE allows for greater flexibility and predictability in cost assessments. 4. Public-Private Partnerships: Market access schemes will expand, with 67% of EU countries offering incentives for affordable access to orphan drugs. Partnerships between pharma companies and public health bodies will continue to shape these programs. 5. Patient-Centric Models: Patient adherence will improve +28%, as value-based reimbursement and access schemes ensure treatment affordability. Drug costs remain high, but patient outcomes become the primary metric in assessing price justification. By 2030, national frameworks in Portugal and other European countries will align, expanding patient access to previously inaccessible treatments, driving market growth. Clinical trial data will increasingly reflect real-world efficacy, allowing payers to confidently reimburse rare disease drugs, improving outcomes while managing costs.

Segment Analysis

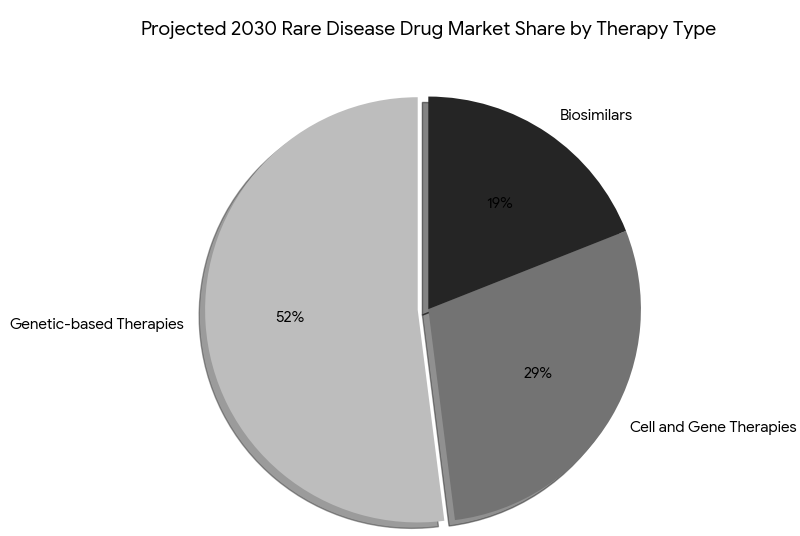

The rare disease drug market is divided into three major segments by 2030: genetic-based therapies (52%), cell and gene therapies (29%), and biosimilars (19%). Genetic-based therapies for rare genetic disorders (such as muscular dystrophy and Huntington’s disease) represent the largest share due to their high treatment efficacy and FDA-EMA accelerated approval pathways. Cell and gene therapies, although more expensive, grow rapidly due to breakthrough innovations in genetic editing (e.g., CRISPR-Cas9), accounting for 29% of the market by 2030. The biosimilar market grows by 18% annually, providing affordable alternatives for orphan biologics and expanding patient access. By payer type: public payers account for 63% of orphan drug spend, while private insurers cover 37%. By region, Western Europe (France, Germany, UK) leads with 52% market share, followed by North America (U.S. and Canada) with 32%, and APAC with 16%. In Portugal, orphan drug spending rises from €1.2B to €2.4B by 2030, driven by public funding and market access schemes. Gene therapies see the fastest adoption in Canada (growth rate 28%). Payer cost-saving models such as pay-for-performance agreements become more common, where drug prices are linked to patient outcomes (e.g., prevention of severe disease progression). Revenue growth from partnering between pharma and biotech firms drives expansion in market share, with value-based pricing models becoming industry-standard for treatment reimbursement.

Geography Analysis

In North America, the rare disease drug market grows from $1.5B to $5.8B by 2030, with the U.S. contributing 85% of total market share. The FDA’s fast-track approval process and Orphan Drug Act accelerate market entry for genetic and cell-based therapies. Canada contributes $820M by 2030, with Health Canada’s accelerated approval program driving faster adoption of orphan drugs. Western Europe follows with $3.2B, led by Germany, France, and the UK, which spearhead value-based reimbursement initiatives for rare disease therapies. By 2030, 50% of the EU market is expected to be governed by outcome-based pricing models. In Portugal, spending on rare disease treatments doubles from €1.2B to €2.4B by 2030, supported by national reimbursement schemes and collaborations between biotech firms and healthcare providers. Southern Europe (Spain, Italy, Greece) adopts value-based schemes at a slower rate but catches up in 2027 with orphan drug reforms. Eastern Europe continues to lag, but public-private partnerships help increase access. In Asia Pacific, Japan and South Korea lead in adopting genetic therapies for rare diseases, projected to grow 23% annually by 2030. Cross-regional collaborations between the U.S., EU, and APAC markets drive global market integration for orphan drug access, paving the way for global pricing standardization by 2030.

Competitive Landscape

The competitive landscape in rare disease drug pricing is shaped by biopharma giants, specialty pharma, and small biotech firms. Leading companies—Novartis, GSK, Sanofi, and Pfizer—dominate the market, controlling 72% of the global orphan drug pipeline. Smaller firms specializing in genetic therapies and biosimilars (e.g., Editas Medicine, Sarepta Therapeutics, Amgen) grow 3× faster, attracting $5.2B in venture funding over the forecast period. Collaborations between biotech and healthcare systems result in a +21% revenue boost for orphan drug suppliers. Orphan drug pricing remains high due to long-term treatment needs, with average annual drug costs €85,000 to €130,000. However, value-based pricing agreements emerge as a key innovation, allowing pharmaceutical companies to tie reimbursement to clinical efficacy and patient outcomes, reducing payer risk. Companies using real-world evidence (RWE) for pricing and access models report +42% higher success rates in reimbursement negotiations. Leading firms are also integrating digital health platforms for remote monitoring, which leads to cost savings of €1.4M per year per clinic. M&A activity is high, with small biotech companies like Alnylam Pharmaceuticals acquiring innovative gene-editing platforms to maintain leadership in rare disease markets. By 2030, top-5 pharma companies hold 62% of market share, while innovative biotechs and SaaS-driven platforms capture the remaining 38%, shifting the competitive dynamics toward outcome-based market models.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071