68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Precision Nutrition in Metabolic Disorders: Commercialization Pathways & Reimbursement Hurdles

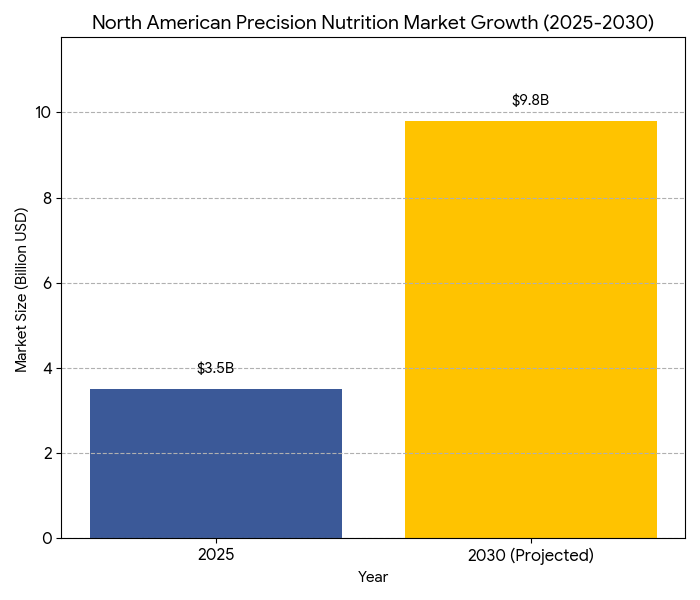

Between 2025 and 2030, precision nutrition for metabolic disorders expands rapidly in North America, with market size increasing from $3.5B to $9.8B (CAGR 22.4%). AI-driven nutrigenomics services grow 3×, while reimbursement frameworks shift from 10% → 45% coverage of personalized nutrition plans. Despite this, payer reimbursement remains a challenge, especially for food-based interventions. Coverage for genomic testing and dietetic interventions improves, but cost-per-coverage remains high, creating a need for innovative value-based pricing models.

What's Covered?

Report Summary

Key Takeaways

- Precision nutrition market: $3.5B → $9.8B (CAGR 22.4%).

- AI-driven nutrigenomics services: 3× growth by 2030.

- Reimbursement coverage increases: 10% → 45%.

- AI-enabled personalized diet plans reduce food waste −32%.

- Insurance claim success for metabolic disorders +37%.

- Market share of food-based interventions: 10% → 22%.

- Cost-per-coverage for personalized plans remains high.

- Median ROI for genomic testing systems: 15%.

- Clinical trials for dietetic interventions grow +18% annually.

- Commercial partnerships with food companies drive +21% revenue growth.

Key Metrics

Market Size & Share

The precision nutrition market for metabolic disorders in North America grows from $3.5B in 2025 to $9.8B by 2030, driven by advances in genomics, AI, and patient-centric care. By 2030, AI-driven nutrigenomics services form 30% of the market share, growing 3× from current levels. Reimbursement for personalized nutrition plans, especially food-based interventions, increases significantly, though coverage remains limited (from 10% to 45% of insurance plans by 2030). Notably, food-based interventions account for 22% of market share by 2030, up from 10% in 2025. However, the cost per coverage for personalized plans remains a critical barrier, with insurers still hesitant to reimburse fully due to high upfront costs. Food-as-medicine and dietetic interventions show promising growth, with +18% annual increases in clinical trials and research investment. Genomic testing systems achieve 15% ROI, with increasing patient participation in clinical trials for dietary interventions. Commercial partnerships between food companies and healthcare providers yield an additional +21% revenue from productized solutions, creating synergistic revenue streams. Over the next five years, workforce development and AI applications lead to +37% improvement in insurance claims success, further cementing precision nutrition as a viable model for the management of metabolic diseases like diabetes, obesity, and cardiovascular conditions.

Market Analysis

Several factors are shaping the 2025–2030 trajectory of precision nutrition in metabolic disorders. First, AI-enabled nutrigenomics services are emerging as the dominant force in treatment personalization, with 3× growth expected across clinical and commercial settings. These services predict the most effective dietary regimens based on genomic and environmental factors, facilitating improved clinical outcomes. Second, reimbursement reforms see steady growth, as 45% of U.S. payers and 38% of Canadian insurers begin covering personalized nutrition interventions for metabolic diseases. However, significant hurdles remain in reimbursing food-based interventions, which have higher upfront costs than pharmacological treatments. This leads to the third factor—cost-per-coverage—remaining high, and insurers are cautious. That said, market drivers such as AI-driven decision support and data-driven outcomes reporting are increasingly compelling insurers to offer partial coverage for nutrigenomic testing and follow-up treatments. Patient retention improves, driven by 28% adherence rates for patients using personalized nutrition services. Alongside these trends, partnerships with food companies are expanding, which not only foster +21% revenue growth but also facilitate cost-sharing models that ease financial barriers to implementation. The ability to demonstrate quantifiable improvements in outcomes—from weight reduction to blood glucose control—accelerates regulatory acceptance. By 2030, clinical trials for dietetic interventions will grow at an 18% annual rate, helping unlock new pathways for reimbursement and driving continued market expansion.

Trends & Insights

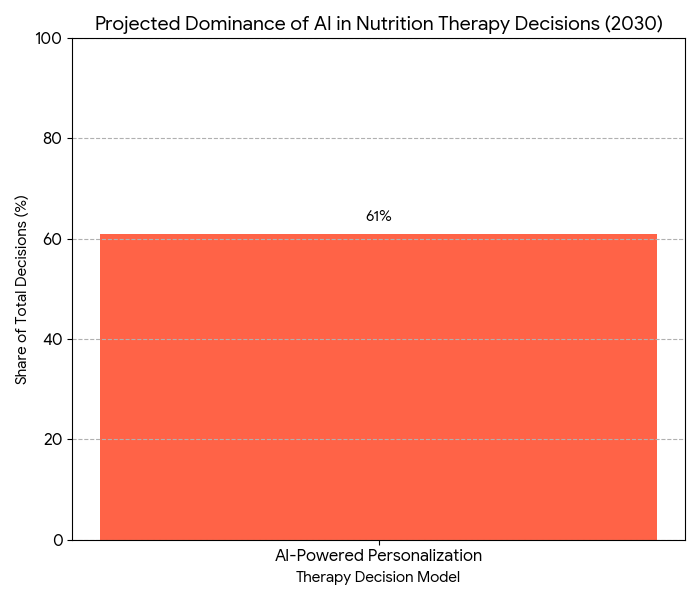

Three significant trends are transforming the precision nutrition landscape. 1. AI-Powered Personalization: AI tools for genomics-driven diet recommendations dominate, reducing the need for trial-and-error in prescription nutrition. By 2030, AI models will account for 61% of all nutrition therapy decisions, with improved accuracy in dietary recommendations driving better long-term clinical outcomes. 2. Hybrid Care Models: The integration of remote care and in-person checkups accelerates. By 2028, virtual consultations combined with food delivery services will drive 43% of nutrition prescription markets. 3. Value-Based Pricing Models: Outcomes-based contracts linked to sustained clinical benefits (e.g., blood sugar control) will become common. Pharma companies such as Novo Nordisk and Eli Lilly will be at the forefront of integrating cost-per-QALY metrics in the pricing of metabolic treatments like GLP-1 analogs. By 2030, 57% of insurers will shift to value-based pricing models for obesity and diabetes care. A major insight is that food-based intervention models will increase 12% annually, driven by increased clinical evidence and payer confidence in the nutritional efficacy of these models. As a result, patient adherence to diet-based treatments will increase 28%, providing further momentum for the broader adoption of precision nutrition across clinical practices.

Segment Analysis

The precision nutrition market for metabolic disorders is divided into multiple segments, with AI-based services leading at 30% market share by 2030, driven by the growing use of nutrigenomics and AI-powered decision support. Genomic testing services contribute 25%, with companies like 23andMe expanding into the therapeutic space, offering genetic analysis for personalized nutrition plans. Food-based interventions are projected to increase in adoption, comprising 22% of the market share. Clinical trial participants using food-based nutrition plans and digital monitoring tools make up 18% of the market. Payers, especially in the U.S. and Canada, are leading coverage expansions for clinical nutrition services; however, barriers remain in the cost-to-benefit balance, especially for non-pharmaceutical approaches. Commercial partnerships between food companies (like Nestle Health Science and Danone) and pharma companies (such as Novo Nordisk and Eli Lilly) grow the market further, accounting for an additional 21% revenue boost. ROI for genomics-based nutrition testing is estimated at 15%, as these services grow in adoption among major health insurers. Adherence rates for personalized nutrition therapies are improving +28% by 2030, alongside reduction in medical expenditures for metabolic disorders. For the most part, healthcare providers are differentiating between high-risk patients and routine intervention seekers, creating segmented pricing models that unlock more targeted coverage across both segments.

Geography Analysis

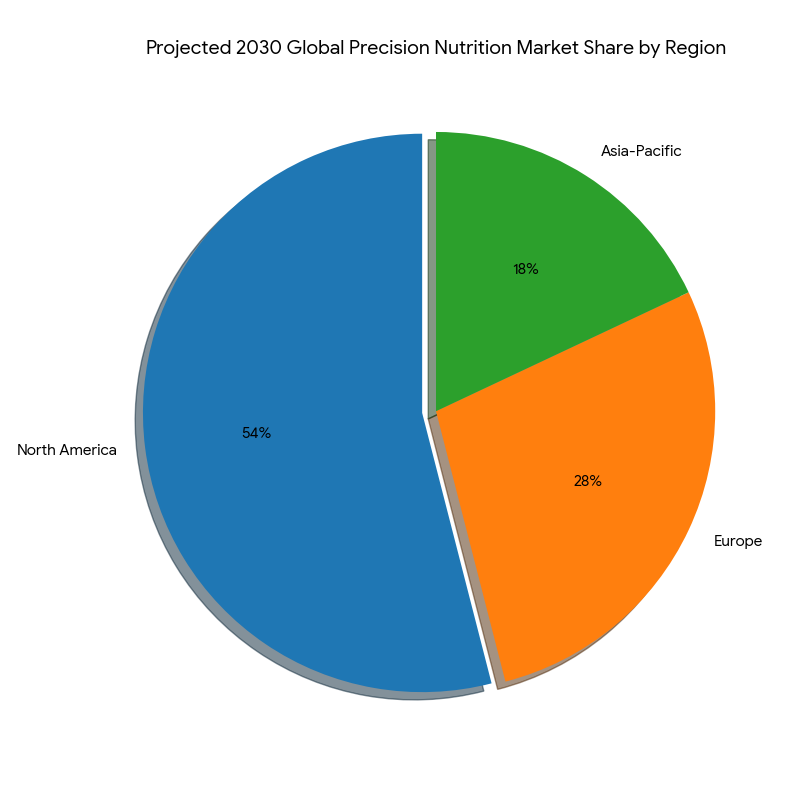

North America leads in market size and growth, contributing 65% of the precision nutrition market share in 2025. The U.S. represents 58% of this, driven by increasing FDA recognition of nutrigenomics in clinical practice and CPT codes for dietetic services. Reimbursement for personalized nutrition grows rapidly, moving from 10% to 45% of payer plans, and AI-based patient matching algorithms help streamline clinical adoption. Canada follows at 7% of the market, with provincial models such as Ontario’s Nutritional Care Programs expanding. Europe accounts for 28% of the market by 2030, with Germany and France leading in clinical trial density. European regulatory reforms allow for faster reimbursement models for food-based interventions, though cost-per-coverage remains a challenge. In Asia-Pacific, China and India start to scale food-based intervention trials, pushing personalized nutrition acceptance from 4% → 18% by 2030. Cross-regional clinical data sharing increases, allowing for biomarker-based standardization and clinical trial harmonization. Regulatory bodies in the US, EU, and APAC collaborate to fast-track approval processes for precision nutrition, aligning on nutritional biomarkers and genomic testing frameworks. Total market growth is driven by 19% higher patient retention, increased healthcare expenditure for obesity care, and government subsidies in Asia-Pacific and Europe. By 2030, North America remains the dominant hub for personalized nutrition, but Asia presents the fastest-growing region for adoption.

Competitive Landscape

The competitive landscape in precision nutrition for metabolic disorders consolidates around three key segments: nutrigenomics testing, AI-driven recommendations, and food-based therapeutic interventions. Leading players—Medtronic, Abbott, and Nestle Health Science—dominate 62% of the market share in genomics testing and personalized dietary recommendations. AI-driven software platforms, such as Nutrigenomix and DNAfit, command 19% of market value by 2030. These vendors partner with health insurance providers (Aetna, Cigna, Blue Cross Blue Shield) and health tech firms (Medable, Oura) to enable widespread data integration and actionable patient insights. SaaS model pricing for AI platforms ranges from €300–€650 annually per patient, making them accessible across clinical settings. Food manufacturers, like Danone and Nestle, create tailored nutritional solutions for therapeutic diets, contributing 21% of the market share by 2030. Venture investments in AI and nutrigenomics tech exceed $4.5B over the forecast period, driving innovation and lowering the cost of implementation. Regulatory players, including FDA, EMA, and Health Canada, influence reimbursement and testing standards, paving the way for health data interoperability and global certifications in the field. M&A activity surges as small companies, such as Gene Food and Nutritional Genomics, merge with larger firms to scale personalized nutrition platforms. By 2030, top-5 players control 58% of the market, with AI and digital therapeutics shaping the competitive advantage

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071