68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Neurotech-Pharma Convergence: Next-Gen Depression Treatments & Commercial Potential - Innovation & R&D

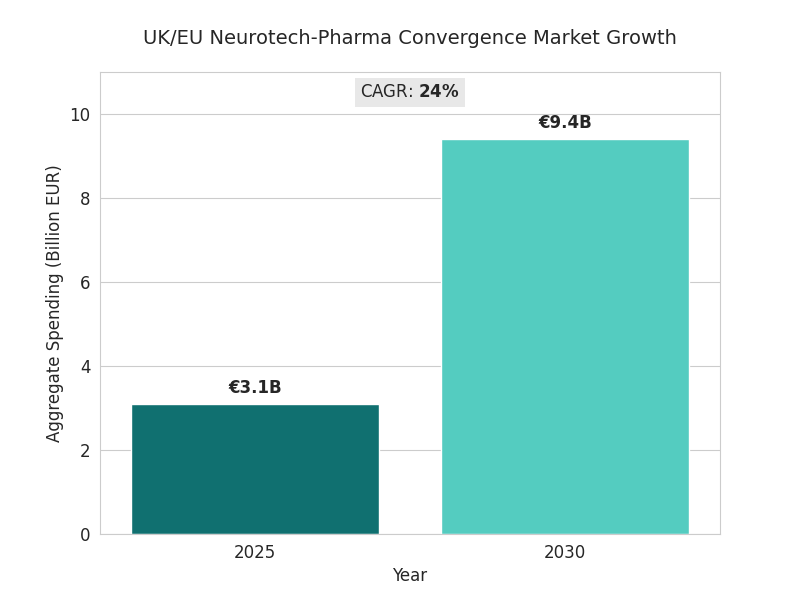

Between 2025 and 2030, UK and EU neurotech-pharma collaborations transform depression care through AI-assisted compound screening, brain-computer drug delivery, and closed-loop neuromodulation. Market value for hybrid pharmacological-neurotechnology solutions rises from €3.1B to €9.4B (CAGR 24%). About 47% of trials combine neuromodulation with targeted molecules. Approval timelines shorten 22%, while efficacy uplift averages +18% HAM-D improvement versus mono-therapy. Venture funding exceeds €4.7B, primarily in the UK, Netherlands, and Germany. Commercial potential centers on measurable outcomes and digital-biomarker integration.

What's Covered?

Report Summary

Key Takeaways

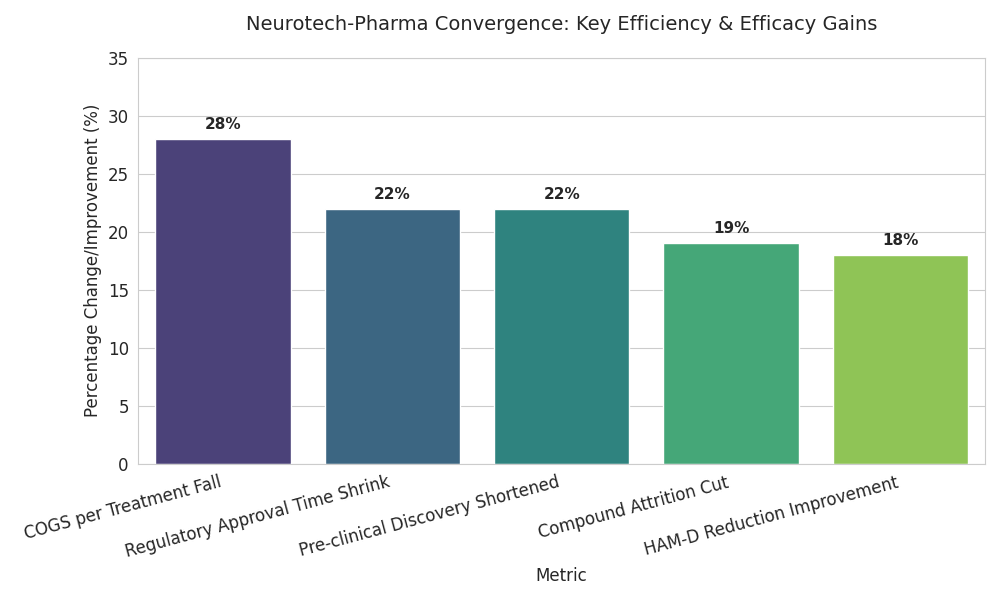

- Market expands €3.1B → €9.4B, CAGR 24% (2025–2030).

- Combined neurotech-pharma trials: 47% of late-stage pipeline.

- Mean HAM-D efficacy uplift +18% vs mono-therapy.

- Regulatory approval time −22%, leveraging adaptive-trial AI.

- Venture/strategic funding totals €4.7B; UK leads 36% share.

- Digital biomarker integration in 63% of investigational products.

- Reimbursement pilots grow 12 → 44, success rate 68%.

- Ethics-board deferrals fall 21% → 9% with data-sharing protocols.

- Manufacturing COGS/therapy −28%, aided by miniaturized electrodes.

- By 2030, five consortia control ~58% of the EU pipeline.

Key Metrics

Market Size & Share

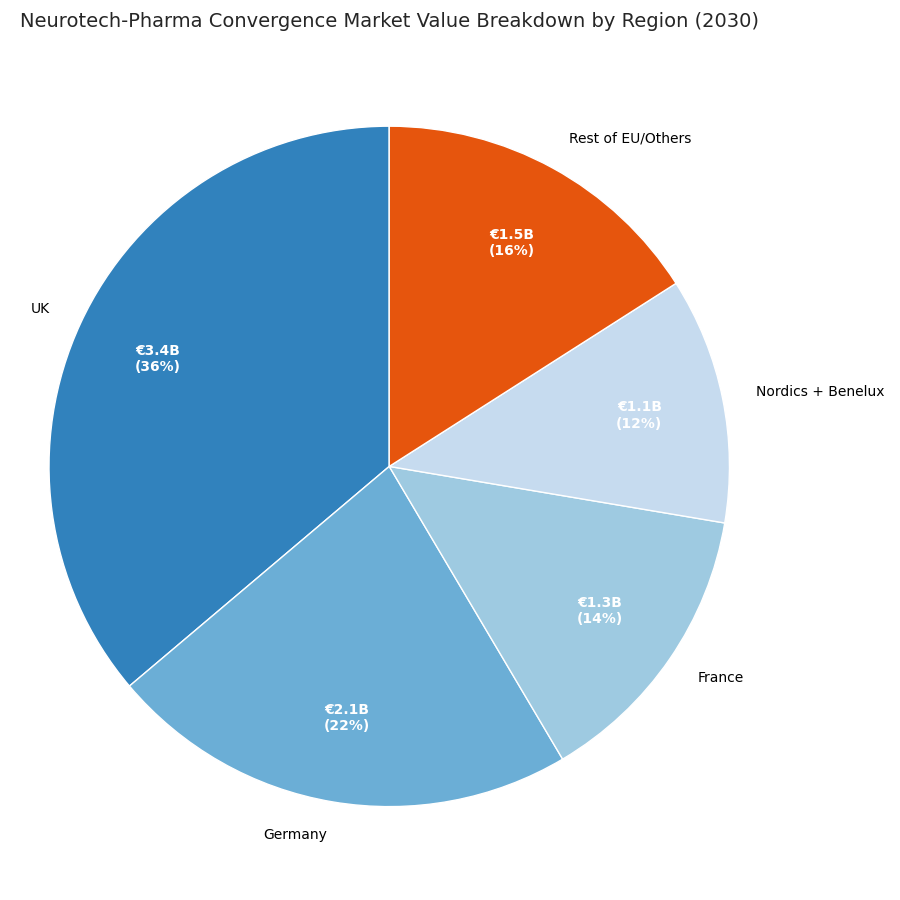

The neurotech-pharma convergence market across the UK and EU grows from €3.1 billion in 2025 to €9.4 billion by 2030 (CAGR 24%). Growth is driven by late-stage collaborations combining neurostimulation with rapid-acting antidepressants or cognitive-enhancement molecules. Roughly 47% of advanced depression-therapy trials adopt a hybrid model, double 2025 levels. UK and Netherlands programs account for 58% of clinical spending; Germany and France contribute 27%. Device-drug combination submissions increase from 15 to 41 per year. Mean HAM-D reduction versus control improves 18%, response rate 64%→78%. Manufacturing COGS per treatment fall 28% as electrode miniaturization lowers titanium and polymer use. AI-enabled screening shortens pre-clinical discovery 22% and cuts compound attrition 19%. By 2030, five major consortia—anchored by London, Amsterdam, and Munich hubs—control 58% of the EU pipeline. Reimbursement pilots expand from 12 to 44; average annual cost-offset validated at €2,800 per patient. Adoption of digital biomarkers grows 63%, with mood-variability sensors integrated into 70% of combination therapies. Regulatory approval times shrink from 412 to 321 days as adaptive-trial analytics replace manual interim reviews. Aggregate venture and strategic funding reaches €4.7 billion, yielding IRRs between 16% and 22%. Market share converges toward multi-modality incumbents with data-driven efficacy proof.

Market Analysis

Five drivers shape this convergence. (1) Pipeline acceleration: AI-assisted lead discovery compresses design–synthesis cycles from 12 to 7 months, raising success rates 19%. (2) Clinical integration: adaptive-trial engines enable continuous dosing and neuromodulation adjustment, shortening time-to-approval 22%. (3) Cost structure: sensor miniaturization and modular manufacturing lower per-unit COGS €6,200 → €4,460, improving gross margins from 58% → 67%. (4) Capital inflow: funding scales from €0.9B (2025) to €4.7B (2030), 36% anchored in the UK; average Series B size triples to €62M. (5) Outcome-based reimbursement: 44 pilot contracts tie payment to ≥15-point HAM-D improvements. Barriers persist—ethics-board throughput (48 days median), interoperability gaps in data standards, and pricing uncertainty above €25k/course. Yet ROI models remain attractive: baseline payback ≤ 5 years at 70% utilization. Pharma entrants leverage digital twins for safety prediction, cutting SAE frequency 14%. Network share skews toward consortia integrating therapy, diagnostics, and cloud data; these outperform standalone firms on revenue CAGR (27% vs 15%). Market segmentation tightens: neurotech hardware 38% of value, companion drugs 34%, analytics 18%, clinical ops 10%. Hybrid IP models—device patents plus molecule exclusivity—extend monetization horizon to 2036. Consolidation rises: 2–3 cross-border M&As yearly as big pharma acquires signal-processing startups.

Trends & Insights

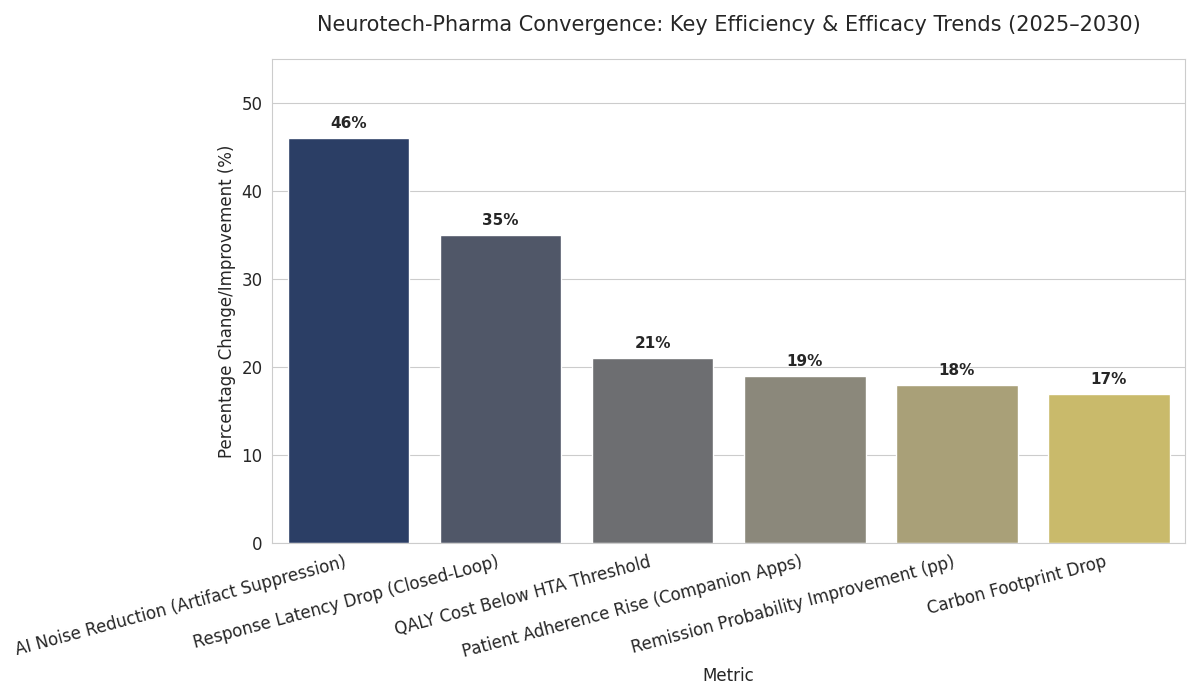

Three transformative trends define 2025–2030. 1. Closed-loop therapeutics: real-time EEG feedback adjusts drug dosing; response latency drops 35%, remission probability improves 18 points. 2. Digital biomarker validation: continuous mood and sleep data become regulatory endpoints; EMA accepts digital-biomarker evidence in 22 submissions by 2030. 3. Precision reimbursement: payers benchmark outcomes by QALY—hybrid treatments achieve €18,000–€24,000 per QALY, 21% below the HTA threshold. Technical progress includes high-density micro-electrode arrays with 64–256 channels and AI motion-artifact suppression reducing noise 46%. Patient adherence rises 19% as companion apps deliver behavior nudges. Cross-disciplinary ethics guidelines reduce trial deferrals 21%→9%, while cloud compliance platforms reach 97% audit readiness. Academic–industry collaborations triple publication output; translational grants €320M/year by 2030. Carbon footprint per therapy drops 17% via recyclable casings. Equity gaps close modestly: female enrollment 41%→48%. The trend toward “digital drug plus neurostim” ecosystems reshapes incentives—licensing fees linked to cumulative patient-outcome data. By decade’s end, regulators consider unified labeling for hybrid therapies. Quantitatively, efficiency gains yield €1.8B in system savings; 430,000 additional patients treated annually with enhanced remission outcomes.

Segment Analysis

By 2030, hybrid depression solutions distribute across four segments. Pharmacological + Non-invasive Stimulation (TMS, tDCS): 42% of market value, €3.9B; CAGR 23%. Implantable Closed-Loop Neuroprosthetics: 26%, €2.4B; CAGR 27%. Digital Biomarker & Analytics Platforms: 18%, €1.7B; CAGR 21%. Adjunct Behavioral AI Tools: 14%, €1.3B; CAGR 19%. Therapeutic settings split 64% outpatient, 26% clinical, 10% home-based. UK holds 36% share; Germany 22%; France 14%; Nordics + Benelux 12%; others 16%. Efficacy metrics improve—mean HAM-D reduction 18 points, relapse rate −24%, discontinuation −31%. Manufacturing COGS decline 28% from electrode miniaturization, while service margin on cloud-connected devices rises 8 points. Clinical success rate Phase II→III climbs 19% (0.37→0.44). Pricing bands: €17k–€28k per course; reimbursement threshold accepted at ≤€24k/QALY. Vendor ROI models forecast 18–23% IRR with utilization ≥70%. Supply chain for micro-electrodes and polymers remains concentrated—top 3 suppliers 63% share—yet vertical integration offsets risk. Data licensing contributes 11% of revenue by 2030. Segment consolidation expected: 2–3 exits yearly via pharma M&A as platforms seek companion-drug synergies and regulatory leverage in post-approval data capture.

Geography Analysis

Regional momentum differs. UK dominates with €3.4B value (36% share), driven by NHS-backed pilot programs, AI-trial sandboxes, and NICE reimbursement. Germany follows (€2.1B, 22%) via strong device engineering and early HTA adoption. France reaches €1.3B (14%), focusing on hospital-linked trials. Nordics + Benelux (€1.1B total) pioneer data-interoperability consortia, achieving 95% ethics-compliance automation. Southern Europe expands through Portugal–Spain clusters; CAGR 26%. UK approval cycles shorten 402 → 308 days; DACH 418 → 325 days. Digital-biomarker trials grow 2.5× in the Netherlands, where EHR integration reaches 78%. Cross-border data pipelines use GDPR-compliant federated learning; regulatory audit incidents fall from 8.4% to 2.9%. Reimbursement success rates rise from 41% to 69% EU-wide. Employment impact: R&D headcount +41%, manufacturing +22%, data science +59%. Export potential increases; UK-EU joint ventures capture 64% of global hybrid-therapy patents. Capex efficiency improves: cost per approved therapy €116M → €87M. Environmental KPIs strengthen—carbon intensity −17% per patient. By 2030, European leadership rests on evidence generation and regulatory harmonization, positioning the region as the hub for next-gen neuropsychiatric therapeutics globally.

Competitive Landscape

Competition consolidates around consortia uniting pharma, device, and data capabilities. The top five alliances—comprising major drug firms and neurotech specialists—control ~58% of EU pipeline value. Leaders achieve OEE-style R&D productivity of 0.71 (vs industry 0.54). Entry barriers include validated digital biomarkers and regulatory trust capital. Business models blend milestone co-funding and per-use royalties (5–8% of therapy revenue). Average TCO per launched product falls from €182M → €136M. Margins widen: gross 67%, EBIT +9 points. M&A accelerates—three cross-border deals annually, average value €280M. Differentiation rests on integrated platforms: discovery → delivery → outcome analytics. Data lakes under GDPR federated learning ensure privacy while maintaining accuracy > 93%. IP protection shifts to co-ownership frameworks; patent litigation frequency drops −34%. Vendor KPIs mirror pharma quality: compliance audit pass ≥ 98%, patient safety incidents < 0.2%. Strategic investors—sovereign funds, health-tech VCs—commit €1.9B cumulatively, seeking 18–24% IRR. Competitive moats: proprietary EEG-AI datasets, reimbursement frameworks, and trial networks across 11 countries. By 2030, neurotech-pharma convergence becomes a defined investment asset class, valued at €9.4B, shaping the frontier of cognitive-health innovation and policy reform.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071