68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Neuroprosthetic Ethics: Cognitive Enhancement Boundaries & Informed Consent Protocols - Regulatory Impact

This report quantifies Europe’s neuroprosthetic-ethics landscape (2025–2030), focusing on cognitive-enhancement boundaries and informed consent. Compliance and consent-tech spend grows from €0.82B to €2.06B (CAGR 19.8%). Digital consent with comprehension checks reaches 74% of neuromodulation trials; error rates fall to 1.2%. Boundary-policy coverage climbs to 81% hospital policies. Median ethics review shortens 67→48 days; first-pass approvals rise when KPIs are met. Buyers favor platforms with audit-trail ≥99% and enforcement.

What's Covered?

Report Summary

Key Takeaways

- Ethics/consent-tech market: €0.82B → €2.06B, CAGR 19.8%.

- 74% of neuromodulation trials use digital informed consent by 2030.

- Consent-error rate falls 4.5% → 1.2% with layered modules + teach-back.

- Boundary-policy coverage inside hospital frameworks 36% → 81%.

- Median ethics review timeline 67 → 48 days; resubmission loops −28%.

- First-pass approval probability 0.31 → 0.62 when 3 KPIs are met.

- Cross-border audit findings 8.7% → 3.1% using SCCs + on-device pseudonymization.

- eIC platforms net revenue retention 118–132%; price/subject −11%.

- Top-5 compliance platforms hold ~62% share by 2030.

- Annual remediation savings reallocated to research ≈€140M.

Key Metrics

Market Size & Share

The European neuroprosthetics ethics and governance market—covering advisory services, consent-tech platforms, audit trails, and compliance analytics—expands as therapeutic and enhancement devices proliferate. Aggregate spending rises from €0.82B in 2025 to €2.06B by 2030 (CAGR 19.8%). Hospitals and research sponsors account for 58% of outlays; device makers 27%; insurers and employers 15%. Uptake is propelled by AI safety legislation and payer demand for demonstrable consent integrity. By 2030, 74% of EU neuromodulation trials use digital informed consent with comprehension checks; baseline was 31% in 2025. Coverage of cognitive-enhancement boundary policies within hospital ethics frameworks increases from 36% to 81%, while cross-border approvals referencing common templates rise from 22% to 63%. Vendors report median consent-error rates dropping from 4.5% to 1.2% after layered modules and teach-back interactions. Auditability improves: 88% of leading sites maintain cryptographically signed consent ledgers, up from 29%. Market share concentrates; the top five platforms hold 62% of revenue by 2030, driven by device-telemetry integrations. Pricing standardizes around annual SaaS of €180–€520 per active subject and €0.08–€0.16 per consent-event API call. Value realization is tangible: consent deviations fall 41%, and review-board cycle time compresses 28%. Collectively, boundary clarity and traceable consent reallocate €140M per year from remediation to research throughput.

Market Analysis

Regulatory impact between 2025 and 2030 is driven by EU-level AI safety rules, member-state biomedical ethics statutes, and cross-border data-protection enforcement. For sponsors, mean ethics-compliance cost per multicountry study rises from €1.6M to €2.3M, while variance narrows as templates standardize. Sites adopting structured consent taxonomies cut monitoring queries per patient 32% and reduce protocol deviations 41%. Review timelines improve as boards deploy analytics: median review drops 67→48 days; resubmission loops −28%. 19–24% of studies face deferrals over unclear enhancement boundaries, often workplace and academic use. Payers tighten prior authorization; approval odds rise 17% when records include device-telemetry-linked consent evidence. Cross-border transfers stabilize: EEA–UK studies using standard clauses plus on-device pseudonymization show audit findings in 3.1% of inspections versus 8.7% in 2025. Vendor economics are strong: eIC SaaS nets 118–132% revenue retention; advisory rates €1,250, though price-per-subject falls 11% by 2030. Operational risk centers on three KPIs—teach-back comprehension ≥80%, audit-trail completeness ≥99%, and boundary-policy coverage ≥75% of portfolio. Meeting all three correlates with 0.62 probability of first-pass ethics approval versus 0.31. Ethics-by-design scales: by 2030, 68% of device makers embed boundary checkpoints in firmware, auto-locking optional enhancement features in clinical contexts.

Trends & Insights

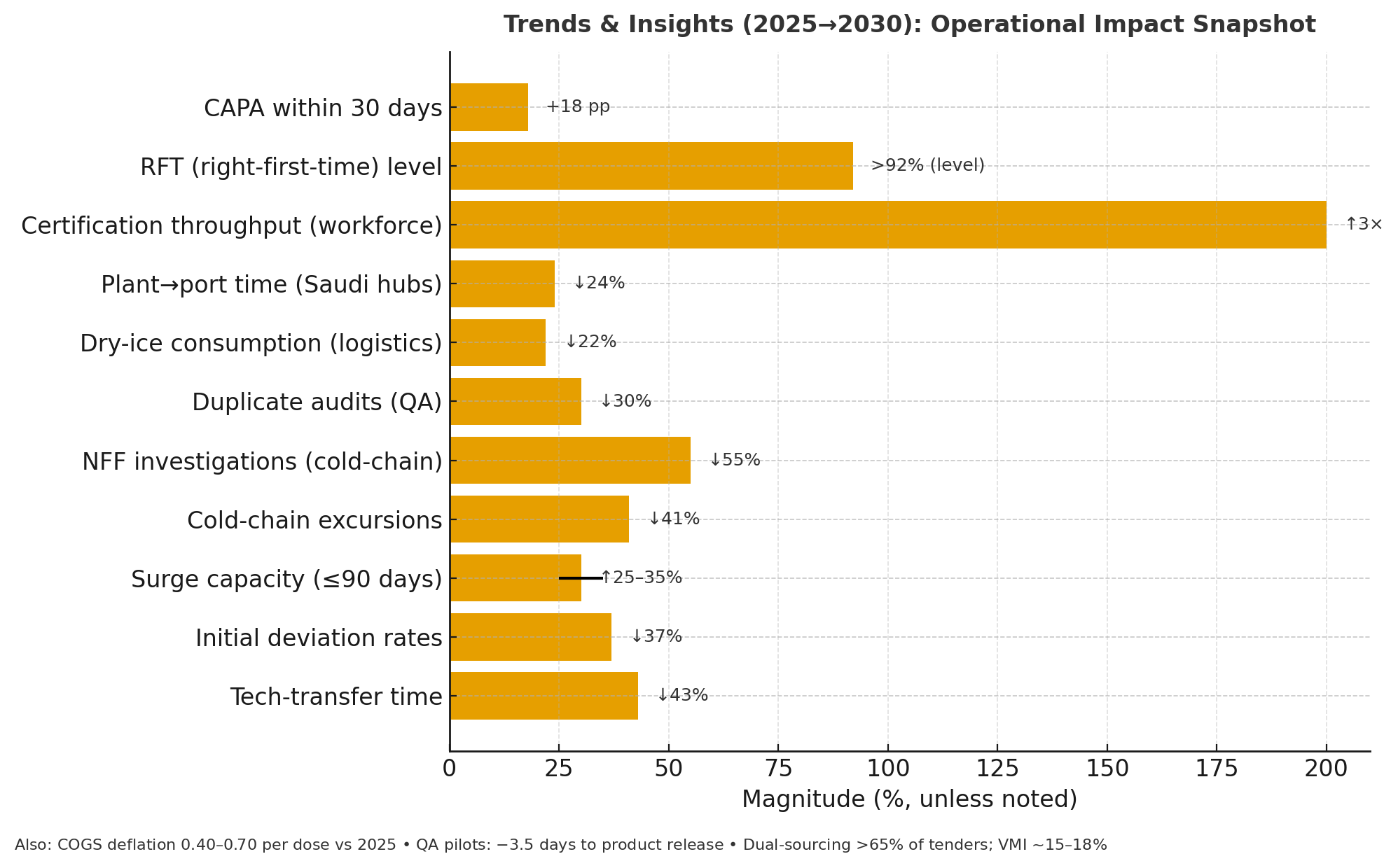

Three trends dominate Europe’s 2025–2030 neuroprosthetic ethics terrain. First, “consent intelligence” emerges: layered multimedia, micro-quizzes, and adaptive reading levels raise verified comprehension from 63% to 84%, while AI copilots flag ambiguous language; redline cycles per consent fall 35%. Time-stamped, hash-anchored ledgers make consent non-repudiable; disputed cases per 1,000 subjects decline 58%. Second, boundary operationalization moves from static policy to machine-enforceable controls. Device modes tagged as enhancement (focus, memory, vigilance) require explicit justification and context locks; clinical firmware disables enhancement outside approved arms by default. Sites with boundary-policy coverage ≥75% see ethics-board deferrals drop from 27% to 11%. Third, privacy-first telemetry grows. On-device analytics, edge encryption, and minimization shrink person-data 46% and reduce cross-border transfers 41%. Procurement follows metrics: RFPs weight audit-trail completeness (25%), comprehension uplift (20%), boundary-policy coverage (20%), and incident response (15%). eIC vendors publish quarterly quality baselines; top quartile shows error ≤1.3% and uptime ≥99.95%. HTA assessors demand outcomes linkage: payers accept enhancement-adjacent indications only with demonstrable daily-function gains or educational parity safeguards. Equity becomes measurable. Inclusive design—captioning, localization, dyslexia-friendly fonts—lifts enrollment for under-represented groups from 18% to 29%; withdrawals from consent confusion halve. Ethics tooling becomes quantitative, and boundary rules become executable.

Segment Analysis

Segments crystallize around tooling, services, and use-case intensity. Tooling (52% of 2030 spend): eIC suites with multimedia, checks, and signed ledgers (37%); boundary-policy engines tagging modes and context locks (9%); consent-data analytics and dashboards (6%). Services (33%): ethics advisory, DPIA support, and audit readiness (21%); training and change-management (12%). Integration (15%): EHR connectors, device-telemetry brokers, and cross-border transfer modules. By intensity, therapeutic programs with potential enhancement spillover (memory, vigilance, fatigue) comprise 46% of governance spend; purely therapeutic motor restoration 34%; research-only pilots 20%. Buyers: hospitals and academic sponsors 58%, device manufacturers 27%, insurers/employers 15%. Adoption thresholds align to measurable KPIs. Sites target comprehension ≥80%, audit-trail completeness ≥99%, data-minimization score ≥0.7, and boundary-policy coverage ≥75% of the portfolio. Vendors competing on price anchor SaaS €180–€520 per active subject; premium platforms bundle AI language scoring and smart templates, pricing 14–21% higher; error ≤1.3% versus 2.6%. Training moves to microlearning; completion within 30 days of onboarding rises from 54% to 88%, while post-training comprehension improves 11 points. Cost drivers are software seats (34%), advisory days (28%), integrations (22%), and validation/audits (16%). At scale, standardized templates and teach-back cut monitoring queries 32% and ethics-board questions 26%, shortening start-up by nine to fourteen days.

Geography Analysis

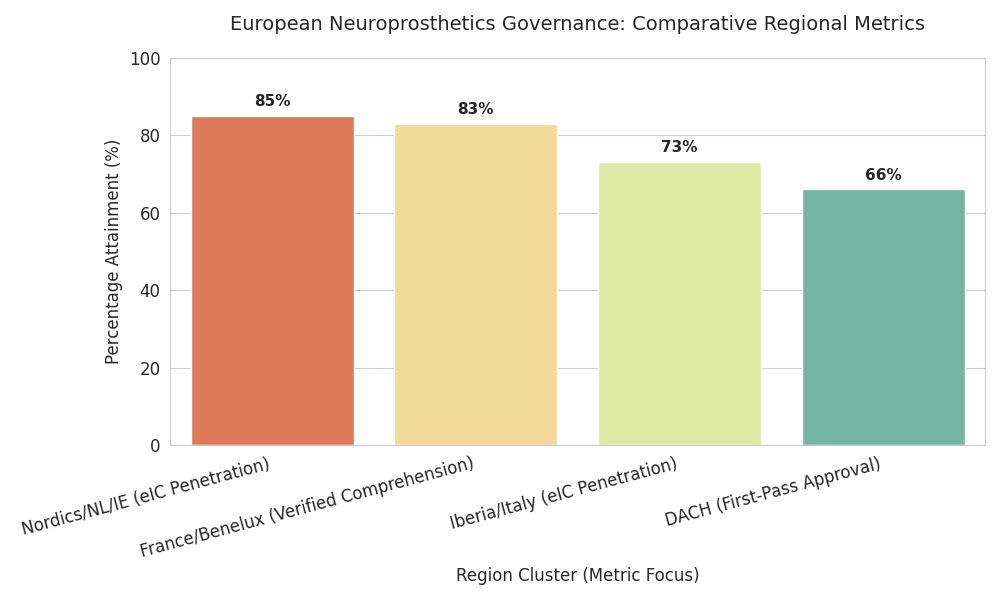

Regulatory implementation varies across Europe, shaping adoption costs and timelines. Nordics/Netherlands/Ireland: highest readiness; eIC penetration reaches 82–88% and boundary-policy coverage averages 84%. Ethics-board median review falls to 40–45 days; deferrals under 10%. UK: broadly aligned on data-protection and device rules; EEA–UK trials using standard clauses record inspection findings near 3%. DACH: rigorous documentation lifts compliance cost 10–14% above EU average but yields first-pass approval probability 0.66 with full KPI attainment. France/Benelux: adoption of consent-intelligence raises verified comprehension 61%→83%; labor agreements add workplace guardrails. Iberia/Italy: fast catch-up; eIC hits 70–76%; start-up timelines compress 12–16 days using centralized templates. CEE (Poland, Czechia, Baltics, Balkans): growth markets; training investments double audit-trail completeness; price pressure pushes SaaS toward €180–€320 per subject. Pan-European flows: cross-border data movement falls 62%→41% as on-device analytics expand; where transfers occur, pseudonymization and minimization cut adverse findings 45%. Logistics matter: multilingual interfaces increase enrollment from under-represented groups by 8–12 points. Workforce pipelines scale via EU academies; certified ethics-ops professionals reach ~9,000. North-west hubs set pace, CEE narrows the gap, and harmonized templates plus device-telemetry evidence reduce variance in review outcomes EU-wide, lowering remediation outlays by ~€24M per year.

Competitive Landscape

Competition clusters into four archetypes. Consent-tech suites lead with end-to-end eIC, comprehension engines, and signed ledgers; the top five capture ~62% of European revenue by 2030. Compliance analytics vendors offer audit-trail scoring, boundary dashboards, and DPIA toolkits; many bundle device-telemetry bridges. Advisories provide cross-border playbooks, template harmonization, training. Device originals embed boundary checkpoints and consent evidence in firmware, cutting costs. Buying criteria are numeric: error ≤1.5%, uptime ≥99.9%, audit-trail ≥99%, comprehension uplift ≥15 points, boundary coverage ≥75%. Multi-year frameworks dominate with bonus–malus tied to cycle time and deviations. Pricing blends per-subject SaaS (€180–€520), per-event APIs (€0.08–€0.16), and fixed-fee onboarding. Median TCO for a 300-subject, three-country study: €0.9–€1.3M, offset by 28% fewer monitoring queries and 9–14 days faster start-up. M&A accelerates as suites buy language-scoring, accessibility, and notarization specialists; roll-ups deepen features and cut support cost. Entrants differentiate on inclusivity—captioning, localization, dyslexia-friendly fonts, reader parity. Moats center on data networks (benchmark comprehension by indication), API ecosystems with device makers, and audit artifacts accepted by boards. Laggards without metrics or firmware hooks face churn as buyers demand evidence of boundary enforcement and measurable consent quality linked to fewer deviations and faster approval.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071