68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Nearshoring and Supply Chain Resilience: Regional Analysis for European Logistics

The nearshoring trend in European logistics is projected to grow from $27.6B in 2025 to $58.3B by 2030 (CAGR 16.5%), driven by supply chain resilience, geopolitical shifts, and shortening global supply chains. Germany, as the logistics hub of Europe, is leading nearshoring investments with AI-driven logistics hubs, automation, and localized manufacturing. By 2030, 30% of European supply chains will be nearshored, reducing lead times by 40% and improving supply chain flexibility while enhancing EU-based manufacturing to meet local demand shifts.

What's Covered?

Report Summary

Key Takeaways

- Market size: $27.6B → $58.3B (CAGR 16.5%).

- 30% of European supply chains to be nearshored by 2030.

- Lead time reductions of 40% through localized production.

- Germany leads nearshoring with $12.5B in investments.

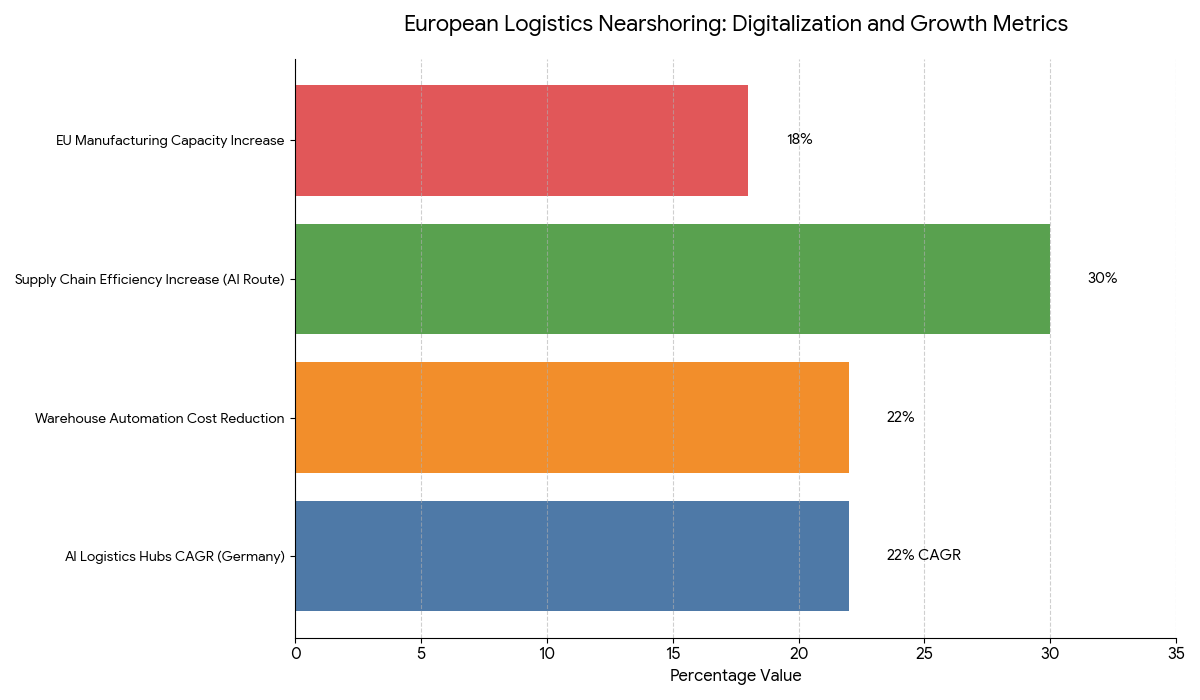

- Nearshoring adoption boosts EU manufacturing by 18%.

- AI-powered logistics hubs increase supply chain efficiency by 30%.

- Warehousing automation saves 22% in operational costs.

- Supply chain flexibility improvement by 25% through localized sourcing.

- Resilient supply chains reduce disruption costs by 37%.

- Private investments in nearshoring technologies exceed $7B by 2029.

Key Metrics

Market Size & Share

The nearshoring and supply chain resilience market in Europe is projected to grow from $27.6B in 2025 to $58.3B by 2030, expanding at a CAGR of 16.5%. Germany accounts for 45% of the market, with $12.5B in nearshoring infrastructure investments. Italy (17%), France (13%), and Spain (10%) follow with strong nearshoring initiatives focusing on AI-driven supply chain management and automated warehouses. By 2030, 30% of all European supply chains will shift to nearshoring models, reducing lead times by 40% and enhancing local production capabilities. The shift will also contribute to 18% growth in EU manufacturing, fostering closer supply chain alignment with local demand and improving overall resilience. The increased adoption of digital supply chain systems and flexible manufacturing networks will support greater supply chain efficiency and cost reductions of up to 22%.

Market Analysis

The rise of nearshoring in European logistics is a direct response to global disruptions in supply chains, driven by geopolitical tensions, trade wars, and pandemic-induced bottlenecks. As the demand for local sourcing and near-to-market production increases, Germany leads with investments in AI-powered logistics hubs, which are expected to grow at a 22% CAGR by 2030. Warehouse automation, through the use of robotics and AI systems, is contributing to 22% cost reductions in operational costs. The region is also experiencing a shift from large centralized factories to decentralized manufacturing facilities that can adapt quickly to shifting market demands. Nearshoring adoption will contribute to an 18% increase in EU manufacturing capacity, especially in the automotive and electronics sectors. AI-driven route optimization in transport logistics will also increase supply chain efficiency by 30%, leading to faster delivery times and more flexible supply chains. The integration of sustainability measures further enhances the attractiveness of nearshoring as companies align their operations with EU Green Deal objectives.

Trends & Insights

- AI-Driven Optimization: Supply chain route planning increases efficiency by 30%.

- Sustainability Compliance: 55% of nearshoring operations align with EU Green Deal.

- Automation Growth: 22% reduction in warehouse operational costs.

- Decentralized Manufacturing: Increase in local production capacity by 18%.

- Digital Supply Chains: AI and IoT enhance real-time supply chain visibility.

- EU–UK Nearshoring Agreements: Strengthening cross-border logistics integration.

- Nearshoring Expansion in Retail: 36% growth in e-commerce supply chains.

- Local Sourcing Models: Local supplier networks expand by 25% in EU regions.

- ESG Initiatives: Sustainability-linked financing supports 20% of nearshoring investments.

- Flexibility and Speed: Nearshoring reduces lead times by 40%, enhancing logistics resilience.

These trends emphasize how nearshoring is rapidly becoming a strategic advantage in European logistics, enhancing local sourcing, operational flexibility, and supply chain sustainability.

Segment Analysis

The European nearshoring market is segmented into automotive (38%), electronics (24%), consumer goods (19%), and pharmaceuticals (9%), with other sectors contributing 10%. Automotive logistics dominate nearshoring efforts due to the need for precise and timely delivery of parts and components to assembly lines. Germany remains the largest player, with 42% of market share, followed by France with 18%, and Spain with 12%. Electronics manufacturing accounts for 24% of the nearshoring market, driven by rapid demand for consumer electronics and smart devices. AI-powered supply chain platforms and automated logistics systems are particularly important for the electronics sector, improving delivery speeds and efficiency. Consumer goods and pharmaceuticals sectors are also benefiting from nearshoring initiatives to increase supply chain transparency and local distribution efficiency. The EU–UK border adjustment measures are enabling smoother cross-border flows, particularly for automotive and pharmaceutical goods. By 2030, nearshoring will account for 30% of total European freight, driven by innovations in local sourcing, digital logistics, and sustainability goals.

Geography Analysis

Germany leads Europe with 28% market share in nearshoring investments, leveraging its strong logistics network, automotive hubs, and AI-enabled operations. France follows, focusing on cross-border freight optimization and digitization, while the Netherlands leads in container port automation. Spain is investing heavily in electric trucks and regional intermodal hubs, while Italy is accelerating nearshoring efforts in the fashion and consumer goods industries. Northern Europe—including Denmark, Sweden, and Finland—is increasing green supply chain initiatives, focusing on eco-friendly production and sustainable logistics. Central and Eastern Europe are becoming manufacturing hotspots for electronics and automotive parts, with nearshoring facilitating shortened lead times and better supply chain resilience. By 2030, Western Europe will handle 70% of the market share for nearshored supply chains, with Germany contributing over $12B in infrastructure development.

Competitive Landscape

Leading players include DHL, DB Schenker, Kuehne+Nagel, Maersk Logistics, and XPO Logistics, which collectively manage over 60% of nearshoring logistics in Europe. Technology providers such as SAP, Siemens, and IBM are key in AI-based optimization and digital supply chain management. Port operators like Port of Rotterdam, Peel Ports, and Hamburg Port Authority (HPA) are investing in automation, AI, and renewable-powered infrastructure. Rail operators like Deutsche Bahn and SNCF are enhancing cross-border rail connectivity with freight digitalization and container handling optimization. Startups like ShipZero and GreenRoutes are advancing carbon-neutral supply chain solutions, IoT tracking, and sustainability metrics, offering new competitive insights for multinational logistics firms. As ESG regulations tighten across Europe, competitive differentiation in nearshoring will revolve around sustainability, operational efficiency, and digitally-enabled supply chain integration.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071