68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Automated Parcel Delivery Terminals Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

Between 2025 and 2030, the automated parcel delivery terminals (APDT) market in the United States expands from $1.9B to $5.6B, registering a CAGR of 23.7%. Growth is driven by e-commerce expansion, urban delivery automation, and last-mile efficiency mandates. Deployment of AI-integrated smart lockers, cloud-connected logistics hubs, and contactless parcel authentication accelerates adoption. By 2030, over 240,000 terminals will operate nationwide, reducing delivery costs by 28% and CO₂ emissions by 32%. Retailers and logistics giants such as Amazon, FedEx, and UPS lead deployments across metropolitan and suburban regions.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.9B → $5.6B (CAGR 23.7%).

- 240,000 terminals expected nationwide by 2030.

- Delivery costs reduced by 28% through automation.

- CO₂ emissions drop by 32% from route optimization.

- Urban regions account for 63% of installations.

- AI-enabled lockers increase throughput efficiency by 35%.

- FedEx, UPS, and Amazon control over 70% of market share.

- Average parcel dwell time reduced from 12 to 5 hours.

- Maintenance and software-as-a-service (SaaS) revenues grow 29% annually.

- Retail partnerships drive deployment across shopping centers and campuses.

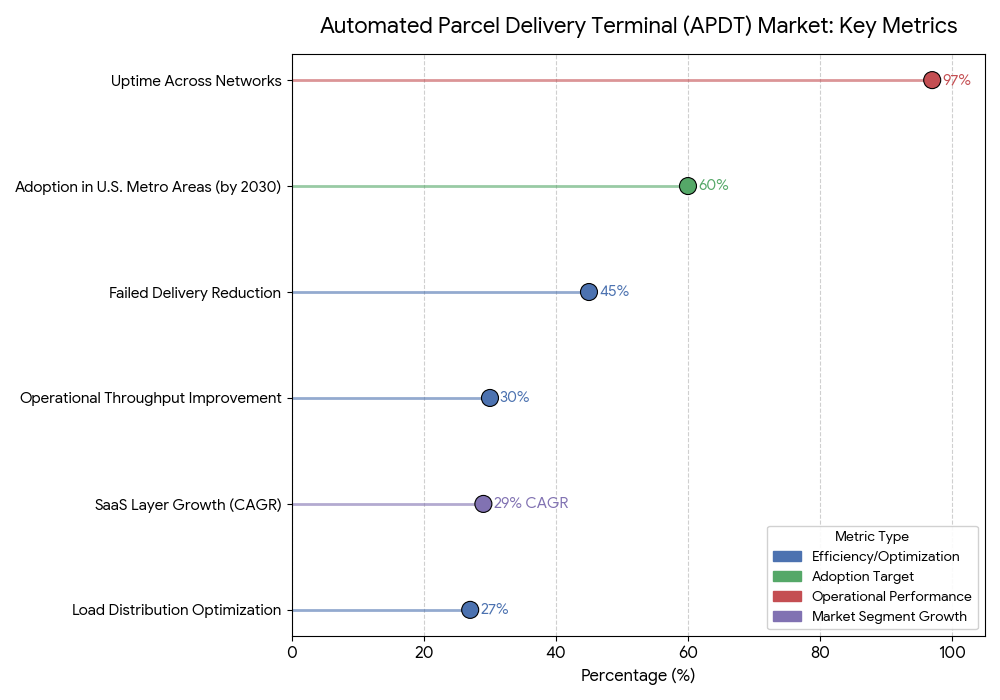

Key Metrics

Market Size & Share

The U.S. automated parcel delivery terminals market grows from $1.9 billion in 2025 to $5.6 billion by 2030, driven by surging e-commerce parcel volumes, which are expected to exceed 42 billion annual deliveries by 2030. Smart locker adoption accelerates across metropolitan centers like New York, Chicago, and Los Angeles, supported by urban density logistics programs. The top three operators—Amazon Hub, FedEx Ship&Go, and UPS Access Point—collectively manage over 70% of total installations, expanding aggressively through retail co-location partnerships. AI-enabled lockers equipped with real-time inventory tracking, dynamic compartment resizing, and contactless pickup authentication improve throughput efficiency by 35%. Meanwhile, delivery cost savings average 28% per shipment, translating to annual savings of $2.3B for logistics operators. Public-private partnerships under the U.S. Smart City Logistics Initiative are financing over $400M in terminal infrastructure to reduce CO₂ emissions by 32% through route consolidation. Retail-driven expansion is equally strong: Walmart, Target, and Best Buy deploy terminals at shopping complexes and suburban hubs, creating 24/7 access points. By 2030, the U.S. will have 240,000 active terminals, with the urban corridor accounting for 63% of deployment. The market’s scalability hinges on continuous AI optimization, SaaS-driven analytics, and multi-carrier integration to meet delivery efficiency and sustainability mandates.

Market Analysis

The APDT market represents a pivotal innovation in last-mile logistics, bridging cost-efficiency and sustainability. By 2030, over 60% of parcels in U.S. metro areas will interact with automated terminals at some stage of delivery. AI-powered predictive allocation systems are transforming delivery workflows, optimizing load distribution by 27% and reducing failed delivery attempts by 45%. Terminals equipped with IoT sensors and cloud-based tracking enhance real-time visibility, allowing carriers to maintain >97% uptime across networks. Capital costs per unit, averaging $16,000–$22,000, are offset by annual operating savings of $4,500–$6,000 per terminal. FedEx and UPS have initiated autonomous parcel loading pilots that improve operational throughput by 30%, while Amazon’s AI logistics stack dynamically assigns lockers based on delivery probability scoring. The SaaS layer—including predictive maintenance, analytics dashboards, and API-based routing—represents a fast-growing segment, expanding at 29% CAGR. Urban policy incentives, especially in California, Texas, and New York, are accelerating terminal zoning and energy-efficient infrastructure credits. By 2030, the integration of AI, robotics, and renewable energy-powered lockers will redefine last-mile delivery efficiency, positioning automated terminals as the backbone of the U.S. e-commerce logistics ecosystem.

Trends & Insights

Key trends defining the U.S. APDT market evolution include:

(1) E-commerce Expansion: U.S. parcel volume grows 12% annually, driving terminal demand.

(2) AI Locker Management: Predictive systems enhance dynamic routing, reducing idle locker time by 41%.

(3) Energy Efficiency: Solar-powered smart terminals reduce electricity consumption by 22% per unit.

(4) Retail Integration: Over 54% of new installations occur at retail centers, creating omnichannel pickup hubs.

(5) Autonomous Delivery Synergy: Integration with drone and AGV systems improves cross-platform efficiency.

(6) Data Monetization: Locker networks generate valuable consumer behavior data, projected at $300M annual analytics revenue.

(7) Multi-Carrier Standardization: APIs unify FedEx, UPS, and USPS access through shared smart terminals.

(8) Subscription Models: Retailers adopt locker-as-a-service contracts, reducing upfront CAPEX by 40%.

(9) Security Enhancements: Biometric verification adoption increases 36%, reducing parcel theft incidents.

(10) Sustainability Regulations: Federal mandates encourage zero-emission delivery infrastructure, fostering long-term terminal deployment growth. Collectively, these trends position automated parcel terminals as the core infrastructure for sustainable, data-driven last-mile logistics in the United States.

Segment Analysis

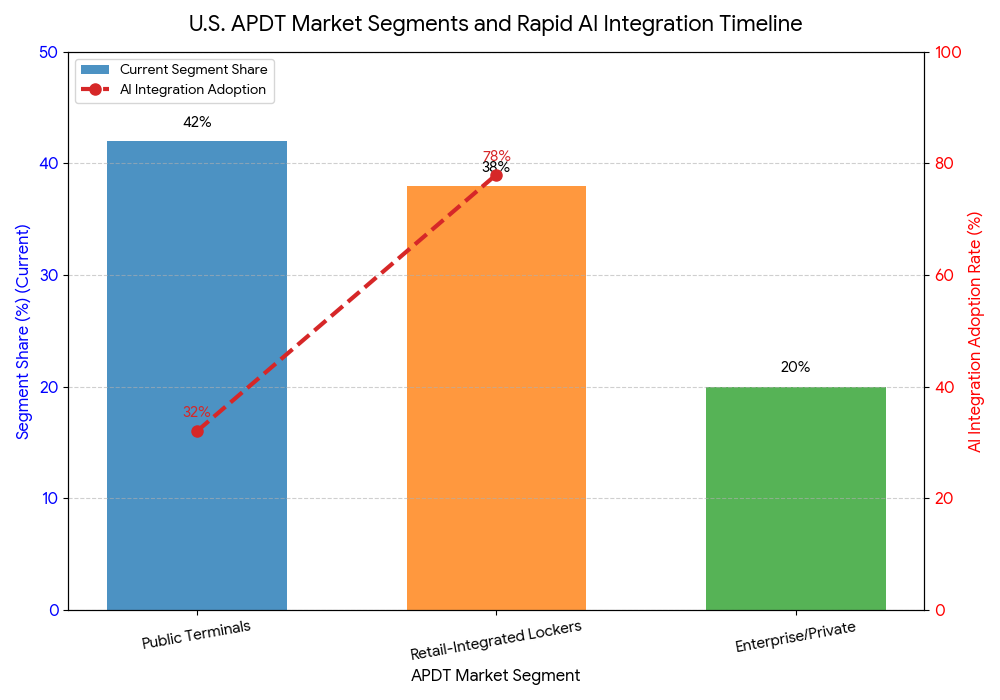

The APDT market in the U.S. is segmented into public terminals, retail-integrated lockers, and enterprise/private installations. Public terminals, representing 42% of installations, are primarily located at transport hubs and post offices, serving high-frequency parcel networks. Retail-integrated terminals account for 38%, driven by partnerships with Walmart, Target, and Amazon Fresh, offering convenience and 24-hour access. Enterprise/private terminals represent 20%, used in corporate campuses, universities, and residential complexes for secure last-mile access. In 2025, AI-integrated terminals comprise 32% of installations, rising to 78% by 2030, as real-time routing and predictive analytics become standard. The urban corridor (New York–Los Angeles–Chicago) remains the fastest-growing subsegment at CAGR 25.1%, while suburban regions adopt terminals through public-private co-investment programs. The hardware-software ecosystem—including sensors, analytics dashboards, and automated loaders—now constitutes 40% of total market value. By 2030, hybrid smart terminals integrating robotic arms for parcel sorting will manage 30% of daily shipments, solidifying their position as essential logistics infrastructure for U.S. urban economies.

Geography Analysis

The U.S. automated parcel terminal market is concentrated across urban megaregions, with California (21%), Texas (14%), and New York (12%) leading adoption. California spearheads smart terminal deployment under the Green Logistics 2030 program, focusing on solar-integrated lockers and EV-powered delivery fleets. Midwestern states—notably Illinois and Ohio—benefit from logistics warehousing proximity, contributing 16% of installations. Southern states (Florida, Georgia) are emerging markets, supported by retail partnerships and tourism-driven parcel volumes. Rural adoption remains slower, representing under 10%, limited by ROI challenges and delivery density. However, federal sustainability grants and USPS collaboration are closing accessibility gaps through mobile terminals. The West Coast corridor accounts for over 35% of total parcel transactions, driven by e-commerce penetration and AI logistics infrastructure investments. By 2030, nationwide coverage will surpass 85% population accessibility, with interoperable multi-carrier terminals becoming standard. These hubs will play a critical role in achieving the U.S. logistics sector’s goal of 40% CO₂ reduction, fostering cost-efficient, customer-centric last-mile delivery.

Competitive Landscape

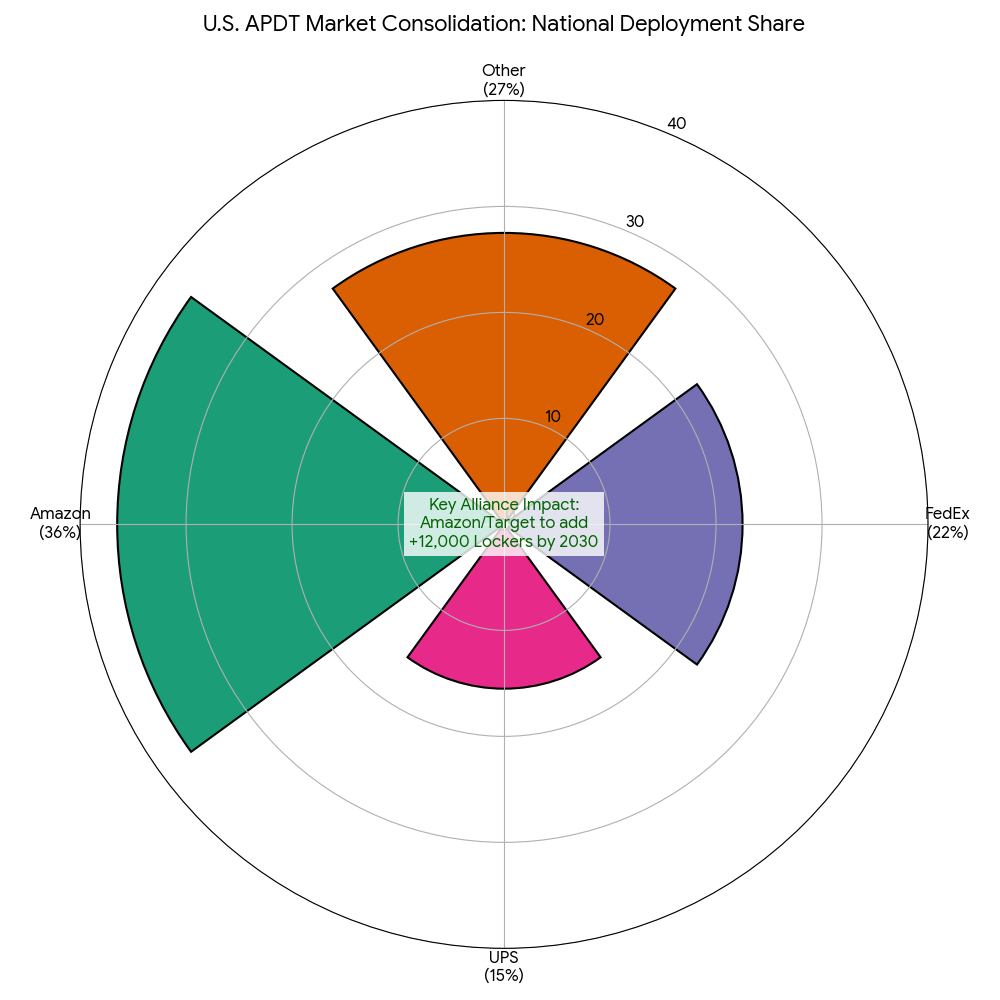

The U.S. APDT market is highly consolidated, with Amazon (36%), FedEx (22%), and UPS (15%) leading national deployment. Smart locker manufacturers such as Cleveron, Quadient, and TZ Limited supply modular hardware for both commercial and government projects. Tech providers like Google Cloud, IBM Watson, and Oracle Logistics Cloud power the AI and predictive routing engines behind network optimization. Regional players—Luxer One, Parcel Pending by Quadient, and Pitney Bowes—dominate the property and multi-family delivery niche. Strategic alliances between retailers and carriers have accelerated deployment: Amazon and Target’s 2029 agreement is expected to add 12,000 lockers nationwide. SaaS platforms for locker management are rapidly evolving, led by Parcel Hive, offering predictive maintenance dashboards and fleet optimization analytics. M&A activity in 2028–2030 is expected to consolidate software-first providers into carrier networks. The competitive advantage now lies in AI algorithm sophistication, hardware scalability, and API interoperability, as logistics leaders move toward autonomous, carbon-efficient, last-mile delivery ecosystems powered by next-generation parcel terminal infrastructure.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071