68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

AI-Driven Construction Logistics: Automated Heavy Equipment & Site-to-Site Inventory (USA & Middle East, 2025–2030)

AI is redefining construction logistics through automation, predictive scheduling, and real-time fleet intelligence. Between 2025 and 2030, adoption of AI-enabled equipment and site logistics software across the U.S. and Middle East is expected to grow at a 28% CAGR, reaching $58B in market value. Autonomous heavy equipment, digital twins, and AI-led inventory routing are cutting idle time by 30–40%, reshaping project timelines and cost structures across infrastructure and industrial projects.

What's Covered?

Report Summary

Market Growth Trajectory (2025–2030)

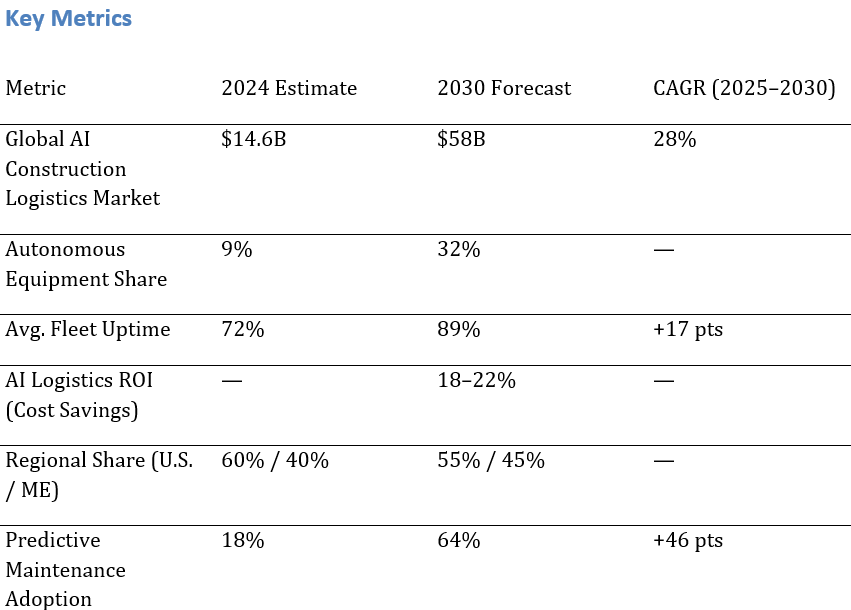

The AI-driven construction logistics market is projected to grow from $14.6B in 2024 to $58B by 2030, expanding at a 28% CAGR. Growth is led by AI-enabled machinery, automated route optimization, and integrated project scheduling tools. The U.S. accounts for 55% of the market, driven by the Infrastructure Investment and Jobs Act and smart city redevelopment. In the Middle East, giga-projects like NEOM, Amaala, and Lusail are embedding AI logistics layers to achieve synchronized material flows across multi-site construction zones.

Heavy Equipment Automation Landscape

Autonomous and semi-autonomous equipment are transforming job site efficiency. By 2030, over 30% of new equipment sold will include embedded AI systems for pathfinding, obstacle detection, and load optimization. OEMs such as Caterpillar, Komatsu, and Volvo CE are deploying integrated LiDAR and computer-vision systems, while startups like Built Robotics and SafeAI retrofit existing fleets. AI reduces idle hours by 25% and fuel consumption by 12%, while remote monitoring enhances operational safety compliance.

Site-to-Site Logistics Optimization

AI logistics platforms now combine drone mapping, IoT sensors, and predictive algorithms to orchestrate material movement between distributed project sites. Machine learning models forecast equipment utilization and route congestion in real time. By 2030, AI-based inventory optimization is expected to reduce material waste by 15–20% and enhance inter-site coordination, particularly in large-scale EPC and PPP projects. Integration with ERP and BIM systems ensures dynamic demand-driven inventory allocation.

Cost & Productivity Gains from Automation

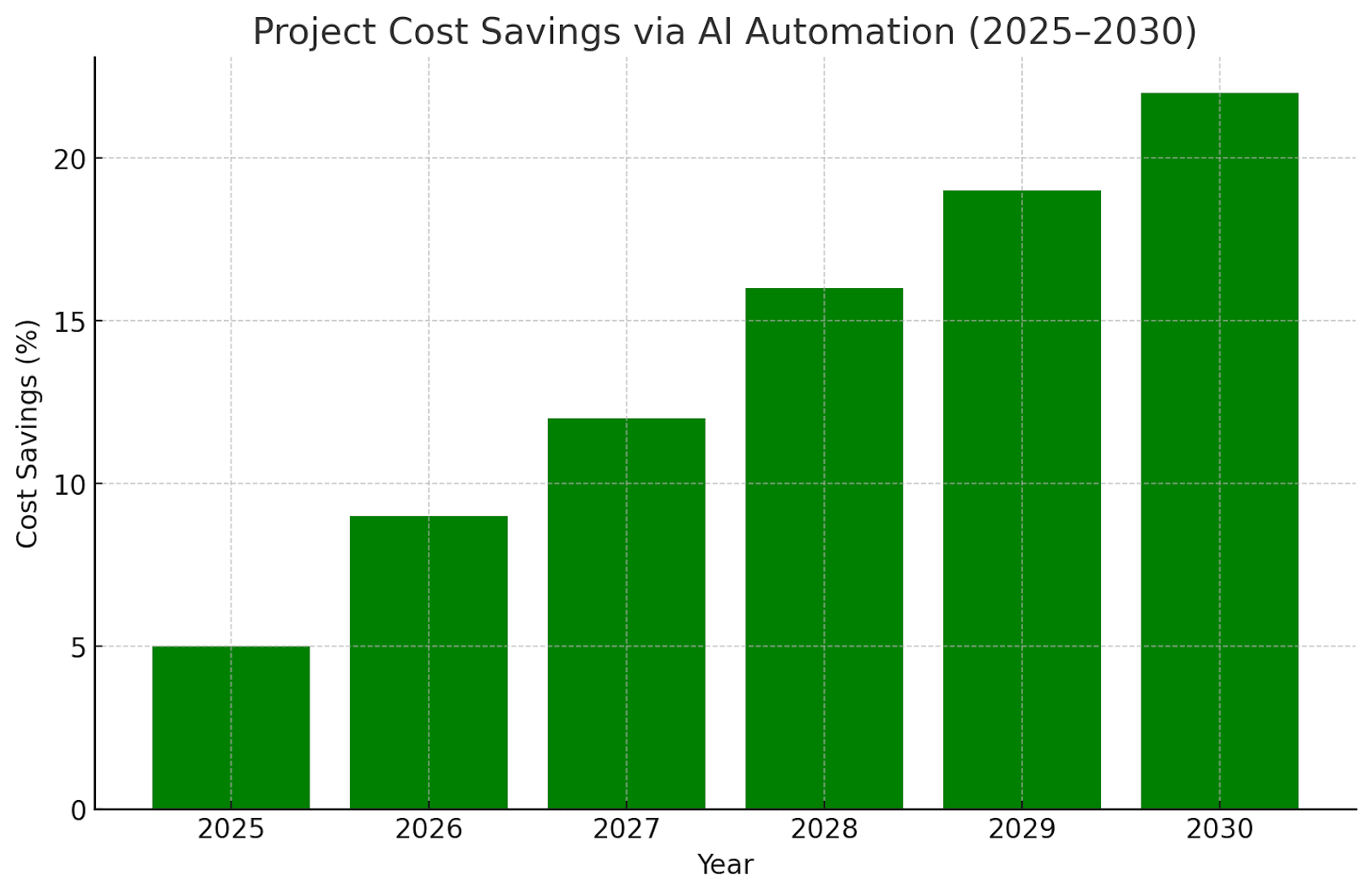

The integration of AI automation yields 18–22% cost savings on large infrastructure projects. Equipment downtime is cut by 35%, while predictive scheduling reduces project delays by 28%. Fleet operators using AI-assisted dispatching and maintenance analytics report ROI within 18–24 months. Middle Eastern projects with high capital intensity gain the most — achieving average cost savings of $3–5M per project through optimized material handling and autonomous transport.

Competitive Landscape

Leading players include Caterpillar, Komatsu, Trimble, Built Robotics, SafeAI, and SAP Construction Cloud. Software integrators like Autodesk and Oracle provide AI logistics modules integrated with digital twins. Regional partnerships — such as Trimble–NEOM and Caterpillar–Saudi Aramco — are setting deployment benchmarks. U.S. firms lead in telematics and predictive analytics, while the Middle East emphasizes heavy fleet automation for remote megaprojects. M&A activity in AI fleet analytics is expected to rise 25% through 2028.

Regional Adoption Comparison

U.S. construction firms prioritize interoperability and safety standards (OSHA-aligned), while Middle Eastern developers emphasize rapid automation scale-up. AI fleet penetration in the U.S. is projected at 36% by 2030, compared to 44% in the Middle East, supported by government mandates in smart city zones. Localized telematics networks and data centers under Vision 2030 frameworks accelerate regional AI deployment across infrastructure, energy, and industrial parks.

Predictive Maintenance & Telematics Impact

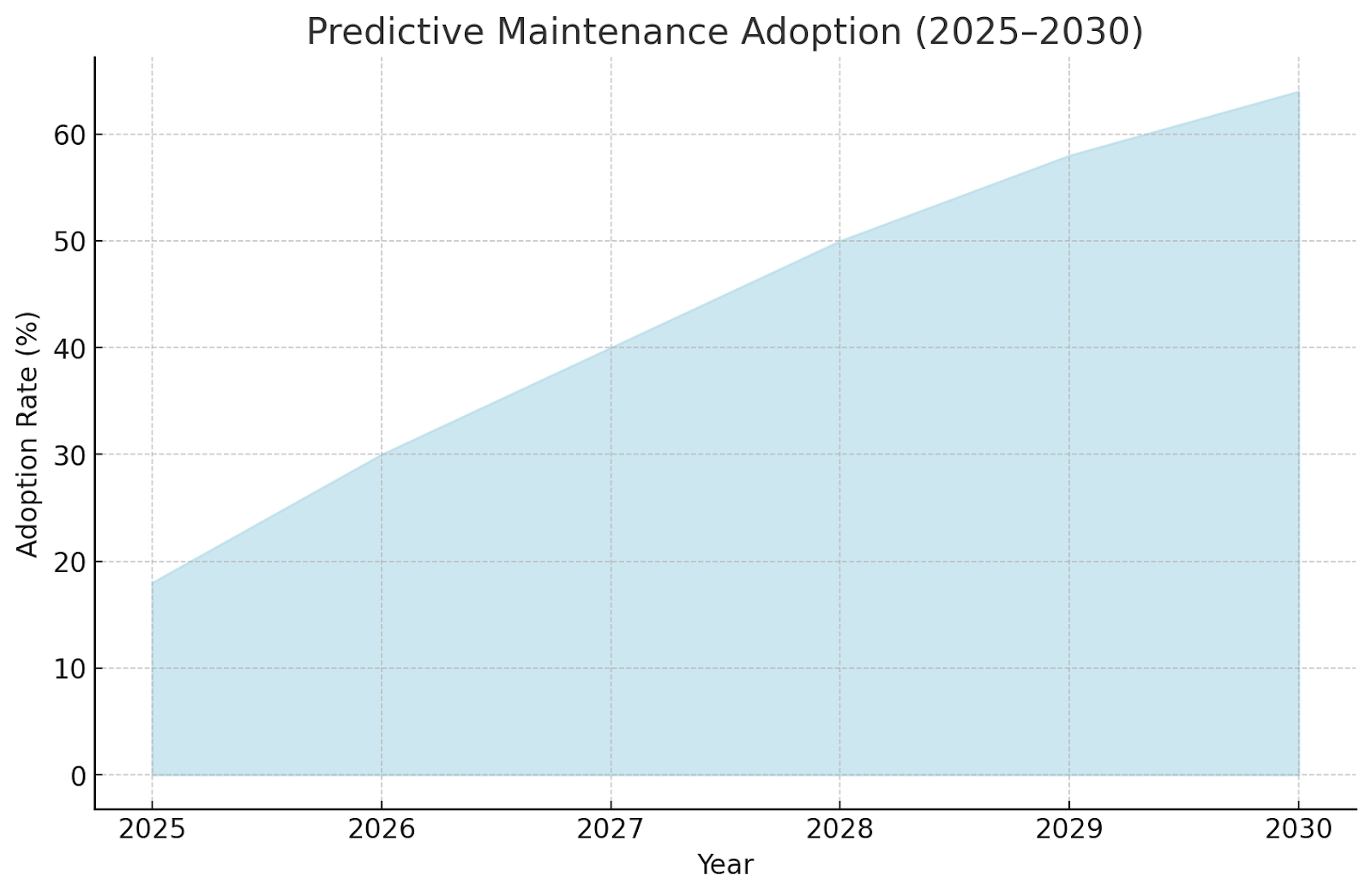

Predictive maintenance adoption across AI-enabled fleets will rise from 18% (2024) to 64% by 2030. AI-based analytics identify anomalies in hydraulic pressure, vibration, and temperature, preventing equipment downtime. Fleet uptime improves from 72% to 89%, extending asset life cycles by 15–20%.

Integration with BIM, ERP & Digital Twins

AI logistics systems are converging with digital twin technologies for synchronized site modeling. Integrations with SAP, Oracle, and Autodesk platforms enable predictive scheduling and resource reallocation. BIM-integrated AI forecasts construction delays with 88% accuracy, while digital twins allow real-time route optimization. These integrations are redefining how project managers visualize site progress and control operational risks across multiple geographies.

Adoption Barriers & Risks

The primary adoption barriers are high CAPEX for autonomous fleet upgrades, limited AI-trained workforce, and fragmented data ecosystems. Smaller contractors often face integration hurdles with legacy ERP and fleet systems. Regulatory approval for unmanned heavy equipment remains pending in several U.S. states and GCC jurisdictions. However, public-private partnerships and OEM financing models are expected to ease adoption by 2027–2028, accelerating ecosystem maturity.

Roadmap for Full AI Autonomy (2025–2030)

By 2030, over 45% of heavy equipment tasks will be automated or AI-assisted. The next wave of innovation includes self-learning dispatch systems, site-to-site swarm logistics, and drone-supervised fleet orchestration. The U.S. is expected to lead in AI logistics software exports, while the Middle East pioneers full-scale autonomous job sites by 2029 through government-led innovation zones.

Key Takeaways

- $58B market size by 2030, up from $14.6B in 2024 (28% CAGR).

- Autonomous & semi-autonomous heavy equipment to reach 32% of total fleet deployments.

- AI-driven site logistics to reduce average project material delays by 35%.

- Predictive maintenance & telematics improve asset uptime from 72% → 89%.

- Middle East adoption accelerated by giga-projects (NEOM, Red Sea, Lusail).

- U.S. infrastructure modernization drives demand for AI-integrated OEM fleets (Caterpillar, Komatsu, Trimble).

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071