68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Green Supply Chains: ESG and Sustainability Strategies in European Logistics

The European green supply chain and logistics market is projected to expand from $48.2B in 2025 to $92.7B by 2030 (CAGR 13.6%), led by Germany’s ESG-driven logistics transformation. Decarbonization, digitalization, and circularity initiatives are reshaping logistics across automotive, retail, and manufacturing sectors. Supported by the EU Green Deal and Corporate Sustainability Reporting Directive (CSRD), logistics operators are investing in electric fleets, AI optimization, and renewable-powered warehouses. By 2030, 40% of EU logistics operations will be carbon-neutral, cutting annual emissions by 38% and improving efficiency by 29%.

What's Covered?

Report Summary

Key Takeaways

- Market size: $48.2B → $92.7B (CAGR 13.6%).

- Germany leads with 28% of regional ESG logistics investments.

- Carbon emissions from freight reduced by 38% by 2030.

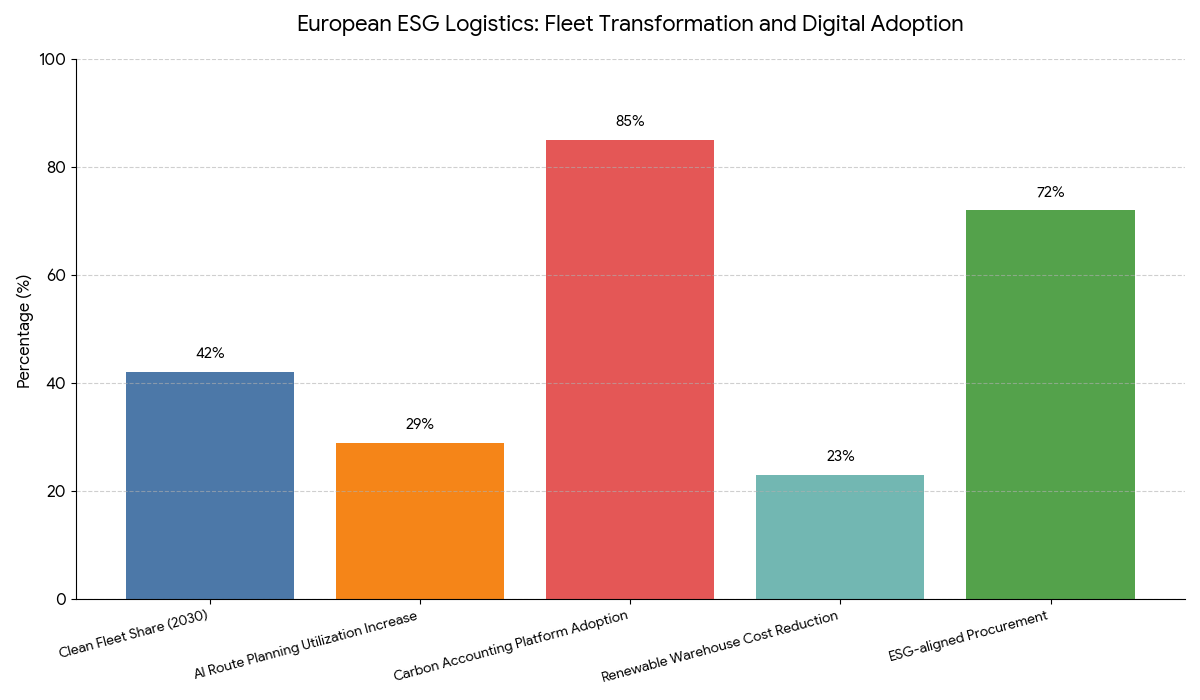

- Electric fleets to represent 42% of logistics vehicles.

- AI route optimization boosts efficiency by 29%.

- Circular packaging programs save $4.1B annually.

- Renewable energy use in warehouses reaches 67%.

- ESG-compliant suppliers account for 72% of procurement value.

- Carbon accounting platforms adoption: 85% of logistics firms.

- Public–private partnerships fund $12.3B in green logistics projects.

Key Metrics

Market Size & Share

The green logistics market in Europe is expected to nearly double, growing from $48.2B in 2025 to $92.7B by 2030, at a CAGR of 13.6%. Germany leads the transition with 28% of total EU green logistics spending, driven by strong ESG mandates, renewable energy adoption, and digital carbon-tracking systems. By 2030, 42% of freight vehicles in Germany and France will operate on electric or hydrogen propulsion, collectively avoiding 12.8 million metric tons of CO₂ annually. AI-powered routing software is projected to reduce idle time and improve transport utilization by 29%. The EU Green Deal’s carbon tax mechanisms will incentivize sustainable fleet renewal and zero-emission warehouse certification. The automotive and retail sectors, accounting for 45% of logistics emissions, are investing heavily in circular logistics networks and renewable packaging. Germany’s Federal Logistics Optimization Framework (2026) is expected to channel $3.8B in public–private capital into sustainable transport corridors, positioning Europe’s logistics industry as a global benchmark for ESG-aligned efficiency.

Market Analysis

Europe’s shift toward ESG-aligned logistics is accelerating through regulatory enforcement, corporate commitments, and clean transport innovation. Germany, France, and the Netherlands are at the forefront, combining AI-based fleet optimization and IoT-driven sustainability audits. Electric and hydrogen trucks now account for 18% of active fleets, expected to reach 42% by 2030. Carbon accounting platforms, such as SAP Sustainability Control Tower and Emitwise, are adopted by 85% of logistics companies to monitor scope 1–3 emissions. Renewable-powered warehouses, using solar and geothermal energy, are reducing operational costs by 23%. The EU Emissions Trading System (ETS) expansion will increase compliance costs by $10 per ton of CO₂ for non-green logistics firms, accelerating the sustainability transition. AI route planning, pioneered by DHL and DB Schenker, enhances utilization by 29%, cutting 900,000 tons of emissions annually. Meanwhile, blockchain transparency tools are integrating supplier ESG validation, ensuring 72% of procurement meets sustainability thresholds. The logistics sector’s combined ESG investment—expected to exceed $12.3B by 2030—signals a profound transformation toward a data-driven, low-carbon European transport ecosystem.

Trends & Insights

- AI in Logistics: 29% improvement in route efficiency via predictive route planning.

- Fleet Electrification: 42% of road freight powered by electric or hydrogen vehicles by 2030.

- Carbon Accounting Platforms: Adopted by 85% of logistics operators for CSRD reporting.

- Renewable Warehousing: 67% of European storage facilities powered by solar or wind.

- Circular Packaging Models: Saving $4.1B annually across FMCG and retail sectors.

- Green Corridors: 48 pan-European sustainable freight corridors under development.

- Hydrogen Infrastructure: 600+ refueling stations operational across EU by 2030.

- Smart Grid Integration: Enables 20% lower warehouse electricity costs.

- Carbon Pricing Pressure: ETS expansion raises non-compliance costs to $10/ton CO₂.

- Sustainability Audits: 92% of top logistics firms now publish annual ESG impact reports.

These trends reflect Europe’s integration of data, energy, and ESG policy into the logistics backbone.

Segment Analysis

The European green logistics market divides into road freight (43%), warehousing & storage (29%), rail & intermodal (17%), and maritime logistics (11%). Road freight dominates due to extensive infrastructure and fleet electrification, expected to grow at 14.2% CAGR. Warehousing is undergoing rapid decarbonization, with 67% powered by renewables and AI-driven inventory management cutting waste by 18%. Rail logistics, backed by $2.6B in EU infrastructure investments, offers carbon reductions of 90% per ton-kilometer. Maritime logistics, led by Germany, Netherlands, and Spain, is shifting to shore-powered hybrid vessels. By 2030, Germany’s green logistics market alone will reach $26B, bolstered by ESG-linked financing and low-emission fleet deployment. Integration of digital supply chain twins is expected to optimize inventory flows and reduce emissions by 28%, ensuring long-term operational sustainability across sectors.

Geography Analysis

Germany leads the European green logistics landscape with 28% of market share, propelled by its National Climate Logistics Framework and Hydrogen Corridor Initiative. France and the Netherlands follow, emphasizing fleet electrification and multimodal connectivity. Northern Europe, particularly Denmark and Sweden, has achieved 65% warehouse decarbonization, aided by renewable district grids. Southern Europe, including Spain, Italy, and Portugal, is investing $1.8B in EV-ready ports and rail logistics modernization. Central Europe’s cross-border corridors, especially Germany–Poland–Czech Republic, are vital to ESG logistics scalability. By 2030, Western Europe will account for 75% of the region’s green logistics value, establishing a continent-wide decarbonized supply chain network that supports both economic growth and environmental compliance.

Competitive Landscape

The competitive landscape features DHL Group, DB Schenker, Kuehne+Nagel, Maersk Logistics, and DSV, controlling over 60% of Europe’s green logistics market. DHL’s GoGreen Plus program aims for net-zero logistics by 2050, with $7B investment in sustainable technologies. DB Schenker leads AI route optimization and hydrogen truck trials across Germany. Maersk is deploying biofuel-powered vessels for intermodal logistics across Northern Europe. Technology partners like SAP, Siemens, and IBM enable ESG data traceability across operations. Startups such as ShipZero and GreenRoutes are innovating in carbon intelligence and digital fleet analytics. As ESG reporting becomes mandatory under CSRD, competitive differentiation will hinge on transparency, renewable integration, and AI-enabled emissions management, cementing Germany’s leadership in sustainable logistics transformation.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071