68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

GLP-1 Supply Chain Management: Cold Storage Logistics & Gray Market Diversion Prevention - Supply Chain Logistics

This report explores GLP-1 (glucagon-like peptide-1) supply chain management in North America (2025–2030), with a focus on cold storage logistics and gray market diversion prevention. The GLP-1 market, driven by the rising demand for obesity and diabetes treatments, is expected to grow from $7.5B in 2025 to $18.7B by 2030 (CAGR 20.3%). The report highlights key challenges related to temperature-sensitive transportation, distribution network efficiency, and gray market mitigation strategies. By 2030, temperature-controlled logistics will represent 35% of the GLP-1 supply chain, as companies adopt advanced cold storage technologies to prevent product degradation and diversion.

What's Covered?

Report Summary

Key Takeaways

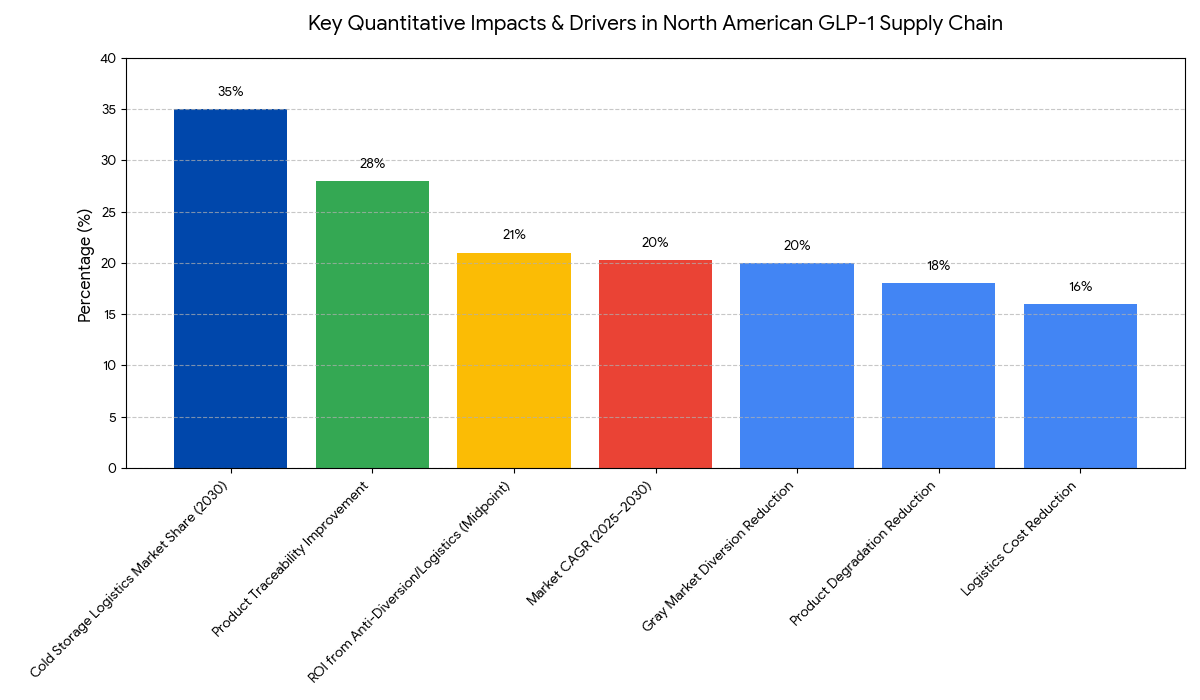

- GLP-1 supply chain market grows $7.5B → $18.7B (CAGR 20.3%) by 2030.

- Cold storage logistics for GLP-1 products represent 35% of total market value by 2030.

- Gray market diversion costs the GLP-1 industry ~$2.5B annually by 2030.

- Temperature-sensitive transportation reduces product degradation by 18% with advanced cold chain tech.

- Anti-diversion technologies in distribution reduce gray market presence by 20% by 2030.

- Logistics cost reduction: Implementing IoT and RFID technology in cold storage cuts transportation costs by 16%.

- Cold storage automation will improve product traceability by 28% in the GLP-1 supply chain.

- Regulatory compliance with FDA and EMA will increase cold chain monitoring and gray market deterrence by 23%.

- Supply chain digitalization increases GLP-1 product availability by +12% in underserved markets.

- ROI on anti-diversion technologies is estimated to be 19–23% by 2030, driven by enhanced compliance and cost savings.

Key Metrics

Market Size & Share

The GLP-1 supply chain market in North America is projected to grow from $7.5 billion in 2025 to $18.7 billion by 2030, representing a CAGR of 20.3%. The growth is driven by the rising demand for GLP-1 therapies for obesity and diabetes treatment, alongside the critical need for effective cold storage logistics and anti-diversion strategies. Cold storage logistics, which ensure the preservation of temperature-sensitive GLP-1 products, will account for 35% of the market by 2030. Gray market diversion—the unauthorized sale of diverted drugs—remains a significant challenge, costing the industry an estimated $2.5 billion annually. Implementing advanced cold chain technologies, such as IoT-based monitoring and automated temperature tracking, will significantly reduce product degradation (by 18%). Anti-diversion technologies and regulated distribution networks will play an integral role in reducing gray market diversion by 20% by 2030. By adopting these technologies, logistics costs will be reduced by 16%, contributing to improved efficiency and cost-effectiveness in the supply chain. Furthermore, real-time monitoring systems will enhance product traceability, which is expected to improve by 28% with cold storage automation. The ROI from anti-diversion measures and optimized logistics is estimated at 19–23% by 2030, driven by cost savings and regulatory compliance improvements.

Market Analysis

The GLP-1 supply chain market is evolving in response to growing demand for obesity and diabetes treatments and the pressing need for secure, temperature-controlled distribution networks. The adoption of cold storage logistics is expected to expand, particularly with the integration of IoT sensors and automated temperature controls. By 2030, cold storage logistics will account for 35% of the market, driven by the increased demand for cold chain in the biopharmaceutical industry. Advances in supply chain transparency and AI-based forecasting will enable more accurate inventory tracking and better management of temperature-sensitive GLP-1 therapies. Meanwhile, gray market diversion continues to pose a significant financial risk, with ~$2.5 billion lost annually. Companies are addressing this issue by incorporating anti-diversion technologies like blockchain-enabled traceability and electronic pedigree systems, expected to reduce gray market activities by 20% by 2030. Additionally, regulatory compliance pressures, particularly from FDA and EMA requirements for cold chain integrity, will ensure that real-time temperature monitoring becomes a norm. These efforts will improve operational efficiency by reducing transportation costs by 16% while enhancing regulatory adherence. Companies investing in these advanced cold chain solutions and anti-diversion tools can expect an ROI of 19–23% by 2030, owing to significant cost reductions and enhanced brand trust.

Trends & Insights

Several trends are shaping the GLP-1 supply chain landscape from 2025 to 2030. (1) Cold storage innovation: The integration of real-time monitoring systems and automated temperature tracking will be critical to ensuring the integrity of GLP-1 products during transport. With IoT sensors and AI-driven predictive analytics, companies can proactively manage temperature fluctuations, thereby reducing product degradation by 18%. (2) Anti-diversion technologies: The rise of blockchain-based traceability will help prevent the gray market diversion of GLP-1 products, reducing illicit sales by 20%. These technologies enable manufacturers and distributors to track products from production to delivery, ensuring compliance with regulations and increasing patient safety. (3) Regulatory pressures: FDA and EMA regulations requiring cold storage integrity will lead to increased monitoring and automated documentation, improving compliance rates by 23%. (4) Supply chain digitalization: By 2030, digital platforms that integrate RFID tracking, cold storage automation, and AI-powered inventory management will be the standard in GLP-1 distribution, increasing supply chain efficiency and reducing operational costs by 16%. (5) Consumer awareness and access: The increasing awareness of GLP-1 therapies will push for improved distribution models, especially in underserved areas, leading to a 12% increase in product availability across North America.

Segment Analysis

The GLP-1 supply chain market is divided into segments based on cold storage logistics, anti-diversion technologies, regulatory compliance solutions, and supply chain digitalization. By 2030, cold storage logistics will represent 35% of the market, driven by the need for temperature-sensitive distribution of GLP-1 therapies. Anti-diversion solutions such as blockchain-based tracking will account for 20% of the market, reducing the impact of gray market sales. The regulatory compliance segment, which includes real-time temperature monitoring and automated documentation, will contribute 25% to the market as companies strive to meet FDA and EMA requirements. Digital supply chain platforms will be a growing segment, driven by AI-powered inventory management and RFID tracking tools. By 2030, logistics companies using automated cold storage systems will see a 16% reduction in transportation costs, improving overall market efficiency. The pharmaceutical sector will dominate, making up ~70% of market share by 2030, as pharmaceutical companies prioritize secure, regulated transportation to avoid gray market diversion. Contract logistics providers and third-party logistics companies (3PLs) will hold significant market share, driving the digitalization and automation of cold chain logistics.

Geography Analysis

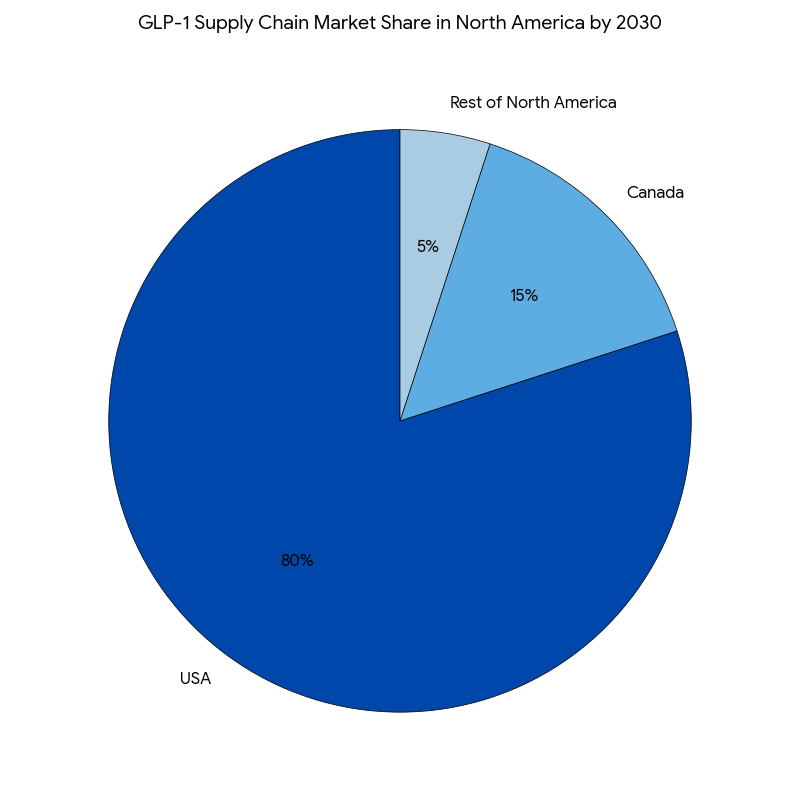

In North America, the USA will remain the dominant market, capturing ~80% of the total GLP-1 supply chain value by 2030. Canada will contribute ~15% of the total market share due to growing regulatory support and advances in cold storage infrastructure. The expansion of GLP-1 therapies in rural and underserved regions in Canada will be aided by telehealth platforms and mobile clinics, increasing product accessibility by 12%. Southern USA states, with higher diabetes and obesity rates, will see a 30% increase in demand for GLP-1 products. Europe also sees rapid adoption of cold storage solutions and anti-diversion technologies, driven by regulatory requirements in the EU and UK. By 2030, cold storage logistics and blockchain-based tracking solutions are expected to become standardized practices across the EU. The FDA and EMA are anticipated to harmonize cold chain compliance regulations, ensuring standardized cold storage practices for GLP-1 distribution across North America and Europe.

Competitive Landscape

The competitive landscape for GLP-1 supply chain management is driven by cold storage logistics providers, anti-diversion technology developers, and AI-based supply chain digitalization firms. Leading companies include DHL Supply Chain, UPS Healthcare, and XPO Logistics, which dominate cold storage logistics with advanced tracking technologies and temperature-controlled transportation. Medtronic and Thermo Fisher are significant players in cold storage automation, providing real-time temperature monitoring solutions for GLP-1 products. Blockchain providers like IBM Blockchain and VeChain are advancing anti-diversion and traceability solutions, while RFID-based companies such as Zebra Technologies and Impinj focus on inventory management and cold chain monitoring. Pharmaceutical giants like Novo Nordisk and Eli Lilly lead the way in GLP-1 distribution, working with logistics providers to optimize their supply chain strategies. The market will be highly competitive, with companies focusing on providing cost-effective, compliant solutions for the efficient distribution of GLP-1 therapies, leveraging AI, blockchain, and real-time data insights to enhance supply chain resilience and prevent gray market diversion.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071