68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

E-Truck Adoption: Market Assessment and Adoption Forecast for E-Trucks in European Road Logistics

Between 2025 and 2030, Europe’s electric truck (E-truck) market is projected to grow from $7.2B to $39.4B (CAGR 40.3%), led by accelerated policy support, decarbonization targets, and total cost of ownership (TCO) parity with diesel vehicles. Germany, as Europe’s logistics hub, will account for 32% of regional market revenue, with over 110,000 E-trucks deployed by 2030. Electrification will reduce operating costs by 28%, CO₂ emissions by 65%, and achieve a battery cost decline to $78/kWh. Supported by EU Fit for 55 mandates and OEM innovation, Europe’s freight transition is entering large-scale fleet electrification.

What's Covered?

Report Summary

Key Takeaways

- Market size: $7.2B → $39.4B (CAGR 40.3%).

- Germany leads with 32% of European E-truck revenue.

- Operating cost reduction: −28% vs diesel fleets.

- Battery cost decline: $128/kWh → $78/kWh by 2030.

- Charging infrastructure: 48,000+ heavy-duty charging points by 2030.

- Fleet electrification: 110,000+ E-trucks in Germany by 2030.

- Emission reduction: −65% CO₂ intensity per km.

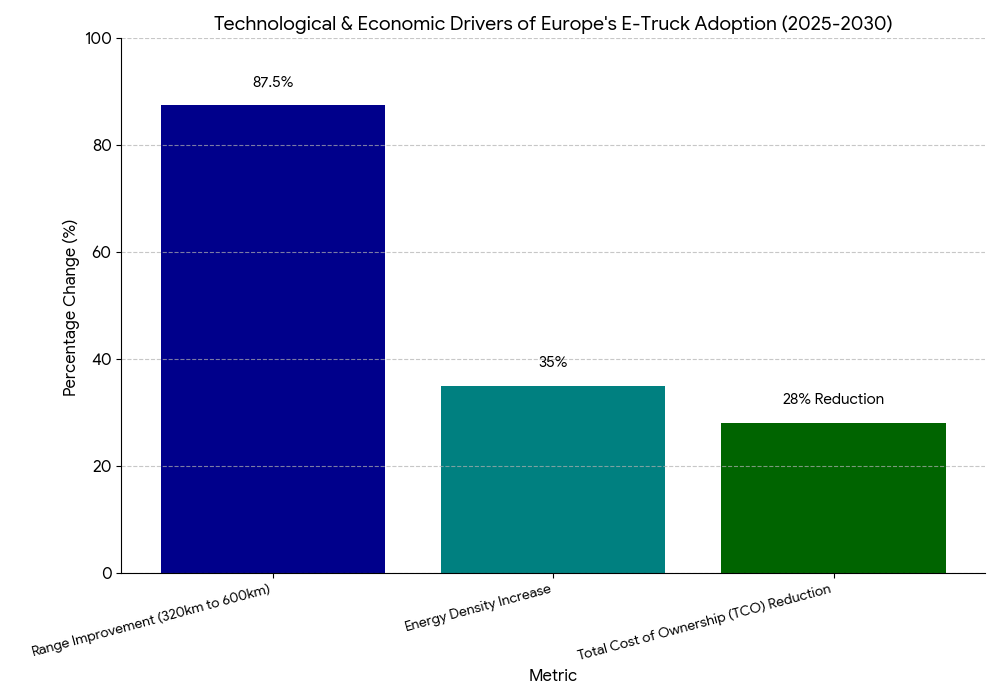

- Payload optimization: Energy density up 35%.

- Policy support: Fit for 55, CO₂ standards, and Green Freight programs.

- TCO parity: Achieved for regional freight by 2028.

Key Metrics

Market Size & Share

The E-truck market in Europe is expected to expand from $7.2B in 2025 to $39.4B by 2030, achieving a CAGR of 40.3%. Germany dominates with 32% market share, driven by logistics demand across the Rhine-Ruhr and Hamburg corridors. Heavy-duty E-truck registrations in Europe will surpass 280,000 units by 2030, with Germany contributing over 110,000 units. The market shift is catalyzed by EU CO₂ emission mandates targeting a 45% reduction by 2030, coupled with subsidies covering up to 80% of incremental EV costs. OEMs like Volvo, MAN, and Mercedes-Benz have announced fleet-scale production of long-haul electric models with ranges exceeding 600 km. Battery costs, which dropped from $128/kWh in 2025 to $78/kWh in 2030, enable TCO parity across most medium-duty freight categories. Charging station density, supported by AFIR (Alternative Fuels Infrastructure Regulation), is set to exceed 48,000 heavy-duty points by 2030. With rising diesel taxation and carbon penalties, electric trucking achieves a 22% logistics cost advantage, anchoring Europe’s transition to sustainable freight operations.

Market Analysis

Europe’s E-truck ecosystem is accelerating due to technological readiness, favorable policy, and cost reduction. The average energy density of truck batteries rose 35% between 2025 and 2030, improving range from 320 km to 600 km. Germany’s Federal Ministry for Digital and Transport (BMDV) allocated €1.2B in fleet electrification incentives under its Kraftverkehr program. Logistics giants like DHL, DB Schenker, and Dachser are electrifying regional fleets to meet corporate net-zero goals. The European Investment Bank (EIB) provided $2.3B in infrastructure loans for megawatt charging hubs across Germany, France, and the Netherlands. TCO analysis shows operating cost declines of 28%, primarily from fuel and maintenance savings. Battery recycling capacity, led by Northvolt and Umicore, strengthens sustainability across the supply chain. By 2030, E-trucks will represent 18% of Europe’s new heavy vehicle sales, signaling mass adoption across the continent’s logistics sector.

Trends & Insights

- Megawatt Charging Systems (MCS): Rollout across 250+ European hubs.

- Fleet Electrification Incentives: Cover up to 80% of capital differential.

- Hydrogen-Electric Hybrids: Emerging for >600 km range segments.

- Battery Second-Life Ecosystems: 40% of truck batteries repurposed by 2030.

- Predictive Maintenance Software: Reduces downtime by 24%.

- Smart Grid Integration: Enables fleet load balancing and grid stabilization.

- OEM Vertical Integration: In-house battery and drivetrain manufacturing lowers costs.

- Carbon Pricing Reform: Increases diesel operating costs by 19%.

- Autonomous E-truck Pilots: Initiatives under EU Connected Mobility Corridor.

- Circular Economy Compliance: EU mandates 70% recycling rate for EV materials.

Collectively, these trends mark a structural freight transition towards electrified, low-emission logistics networks.

Segment Analysis

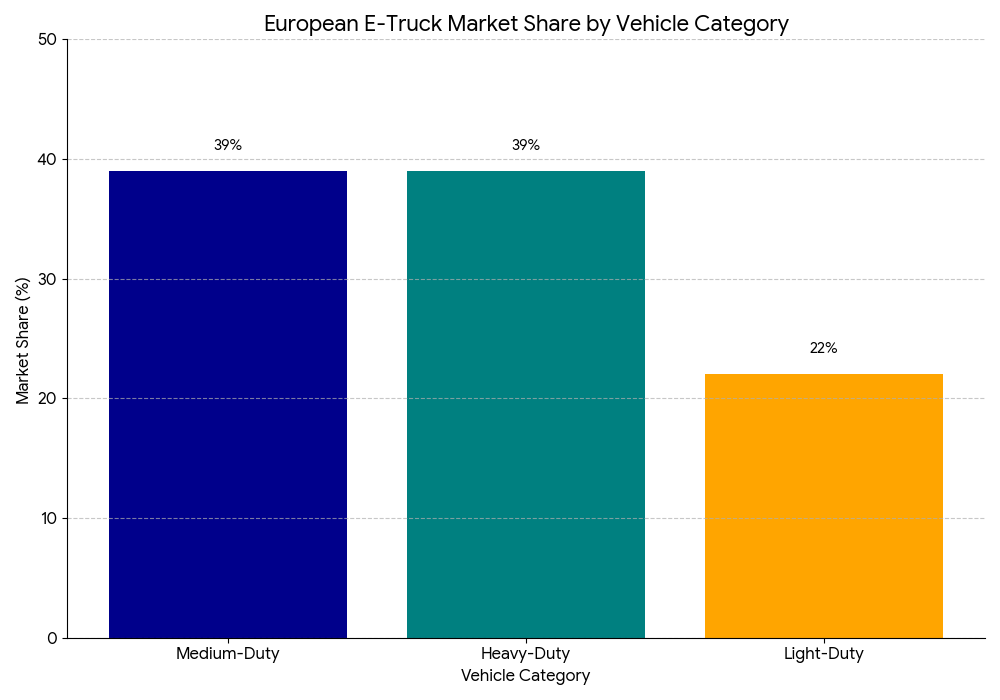

The market divides into light-duty (22%), medium-duty (39%), and heavy-duty (39%) E-truck categories. Medium-duty trucks dominate regional logistics fleets, especially in urban and intercity delivery routes. Heavy-duty long-haul E-trucks, achieving range improvements up to 650 km, are forecasted to grow 6.4× by 2030. Light-duty trucks, targeting city logistics, benefit from short-range cost efficiency, with average ownership cost reductions of 31%. Germany’s MAN eTruck and Mercedes eActros 600, alongside Volvo FH Electric, lead sales across Europe. Charging infrastructure segmentation shows fast-charging hubs (54%), depot-based charging (33%), and on-route megawatt systems (13%). Market fragmentation is declining as OEMs partner with utilities like E.ON and EnBW for grid-ready logistics hubs. By 2030, E-trucks are expected to capture 27% of total European road freight value, reshaping operational economics across distribution chains.

Geography Analysis

Germany leads European E-truck deployment with 32% market share, followed by France (21%), Nordics (15%), Benelux (12%), and Eastern Europe (8%). Germany’s Autobahn electrification pilots—covering 480 km under Siemens eHighway—serve as a testbed for hybrid truck adoption. France accelerates through €1.4B incentives under Plan France 2030, while Sweden and Norway lead in green freight corridor electrification. Benelux countries deploy dense depot charging networks, achieving 92% fleet connectivity by 2030. Eastern Europe is emerging as a manufacturing base for E-truck components due to lower production costs. By 2030, Western Europe will host 68% of all electric heavy truck fleets, while Central and Eastern Europe become export hubs, forming a pan-European green freight ecosystem with cross-border energy interoperability.

Competitive Landscape

The competitive ecosystem is dominated by OEMs, charging infrastructure providers, and logistics operators. Volvo Trucks, MAN, and Mercedes-Benz lead in vehicle deployment, each exceeding 20,000 units across Europe by 2030. Tesla Semi and Scania target long-haul electrification with autonomous-ready vehicles. Infrastructure firms like ABB, Siemens Energy, and Alpitronic develop megawatt charging systems for depot integration. Fleet electrification partnerships between DHL–Volvo, DB Schenker–MAN, and Dachser–Mercedes enhance operational scalability. Battery recycling leaders, including Northvolt, Umicore, and Li-Cycle, secure circular economy compliance. Software players like Geotab and Trimble are embedding real-time energy optimization into fleet management. Competitive success hinges on charging speed, TCO parity, and lifecycle emissions reduction, positioning Germany and Scandinavia as Europe’s E-truck innovation epicenters by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071