68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Circular Economy in Automotive Logistics: Sustainability & ESG Strategies for EU OEMs

Between 2025 and 2030, the circular economy in automotive logistics across Europe, led by Germany, expands from €5.2B to €16.4B (CAGR 26.3%). EU OEMs are re-engineering logistics networks to integrate remanufacturing loops, green warehousing, and parts reuse systems. Germany, accounting for 37% of regional investment, pioneers battery reverse logistics and ESG-certified material flows. Closed-loop supply models cut carbon intensity by 44% and logistics waste by 35%. By 2030, circular logistics will become a regulatory and financial requirement under EU CSRD and ESG disclosure mandates.

What's Covered?

Report Summary

Key Takeaways

- Market size: €5.2B → €16.4B (CAGR 26.3%).

- Germany leads with 37% of EU circular logistics investment.

- 44% reduction in logistics carbon intensity via closed-loop systems.

- Battery reverse logistics grows 28% CAGR.

- 35% drop in packaging waste through reusable containers.

- Scope 3 emission tracking mandatory for 95% of OEMs by 2030.

- Digital twins & AI improve route optimization by 22%.

- €1.4B annual savings from remanufacturing-based spare-part logistics.

- EV supply chain circularity index rises from 41% → 73%.

- EU CSRD/ESRS drive ESG-aligned logistics reporting adoption.

Key Metrics

Market Size & Share

The European circular-logistics market expands from €5.2 billion in 2025 to €16.4 billion by 2030, at 26.3% CAGR. Germany commands 37% of total investment, led by Volkswagen, BMW, and Mercedes-Benz, each integrating remanufacturing hubs and reverse-logistics networks across Europe. Battery collection and recycling flows grow fastest—handling 820 k tons annually by 2030—as EV penetration deepens. Packaging reuse initiatives eliminate 2.8 million tons of single-use plastics yearly, while AI-driven material traceability reduces lost or scrapped inventory by 18%. Carbon emissions per ton-kilometer fall from 72 g CO₂e (2025) to 40 g (2030) as fleet electrification and multimodal transport expand. EU-wide legislation, notably the Circular Economy Action Plan 2.0, enforces mandatory recovery quotas (70%) for logistics materials. Germany’s Digital Product Passport initiative ensures parts traceability through blockchain-verified identifiers. Together, these measures save OEMs €1.4 billion annually while strengthening ESG compliance. By 2030, circular logistics will underpin 95% of EU automotive exports, reshaping supplier contracts and trade finance models toward resource-positive value chains.

Market Analysis

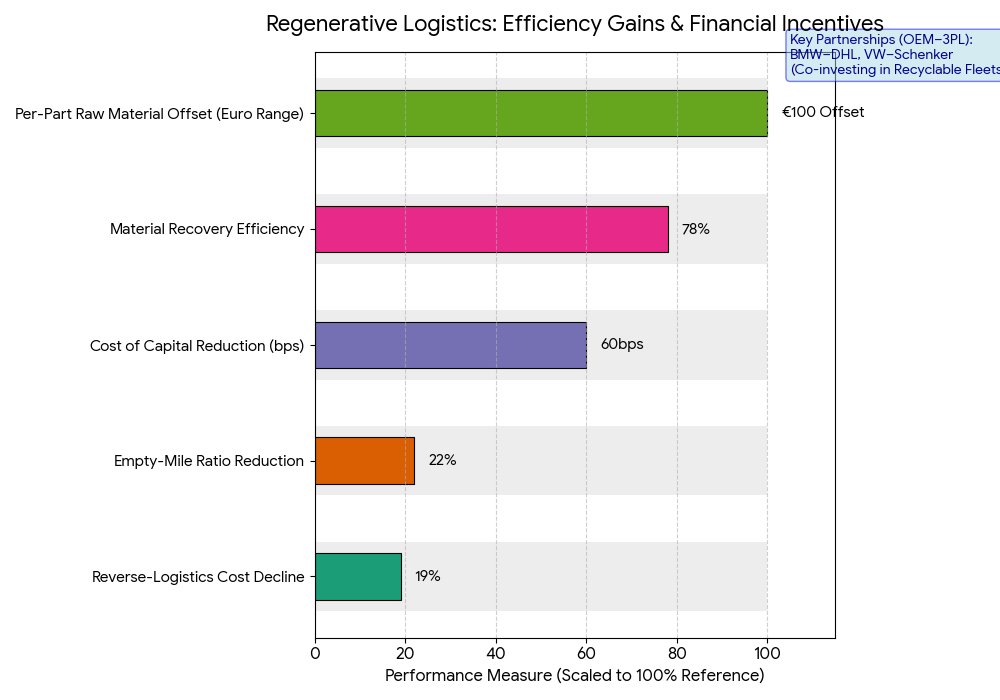

Market performance reflects a systemic shift from linear to regenerative logistics. Reverse-logistics costs decline 19%, aided by automated sorting and shared return networks. AI route-optimization and digital twins lower empty-mile ratios by 22%, cutting fuel and emissions. OEM–3PL partnerships (e.g., BMW–DHL Supply Chain, VW–Schenker) co-invest in recyclable container fleets and zero-emission last-mile delivery. Germany’s battery-recovery ecosystem, driven by Northvolt and Mercedes-BatteryLoop, yields material recovery efficiencies of 78%, surpassing EU targets. Lifecycle analytics platforms quantify carbon impact at the component level, integrating with ESG-reporting software like SAP Sustainability Control Tower. Rising energy costs incentivize closed-loop logistics—each reused part offsets €80–€120 in raw-material inputs. Green-financing instruments, including EU Taxonomy-linked loans, cut weighted cost of capital by 60 bps for compliant OEMs. Key risks include high data-integration costs and vendor-standard fragmentation, though harmonization efforts under ESRS E5 are reducing barriers. By 2030, logistics will evolve into an asset-light, digitally monitored circular network, transforming sustainability from compliance obligation to profitability lever.

Trends & Insights

(1) Reverse logistics automation: Robotics-enabled returns processing improves efficiency by 30%.

(2) Battery traceability: QR- and blockchain-linked identifiers certify end-of-life recovery for >90% of EV cells.

(3) Modular packaging reuse: Crate-pooling platforms across OEMs save €420 M/year.

(4) Renewable-powered fleets: 48% of logistics energy from renewables by 2030.

(5) Digital product passports: Mandatory under CSRD from 2028 for auto components.

(6) Supplier ESG scoring: Embedded in OEM procurement, reducing high-risk suppliers by 18%.

(7) Carbon-accounting software integration: ERP-based emissions dashboards achieve real-time Scope 3 visibility.

(8) AI lifecycle analytics: Predictive tools extend component reuse by 25%.

(9) Green financing linkages: Banks tie loan spreads to logistics ESG ratings.

(10) Circular procurement alliances: Joint OEM networks consolidate material recovery contracts, lowering costs by 17%.

Collectively, these trends establish a data-centric circular-logistics framework, embedding sustainability across the entire European automotive supply chain.

Segment Analysis

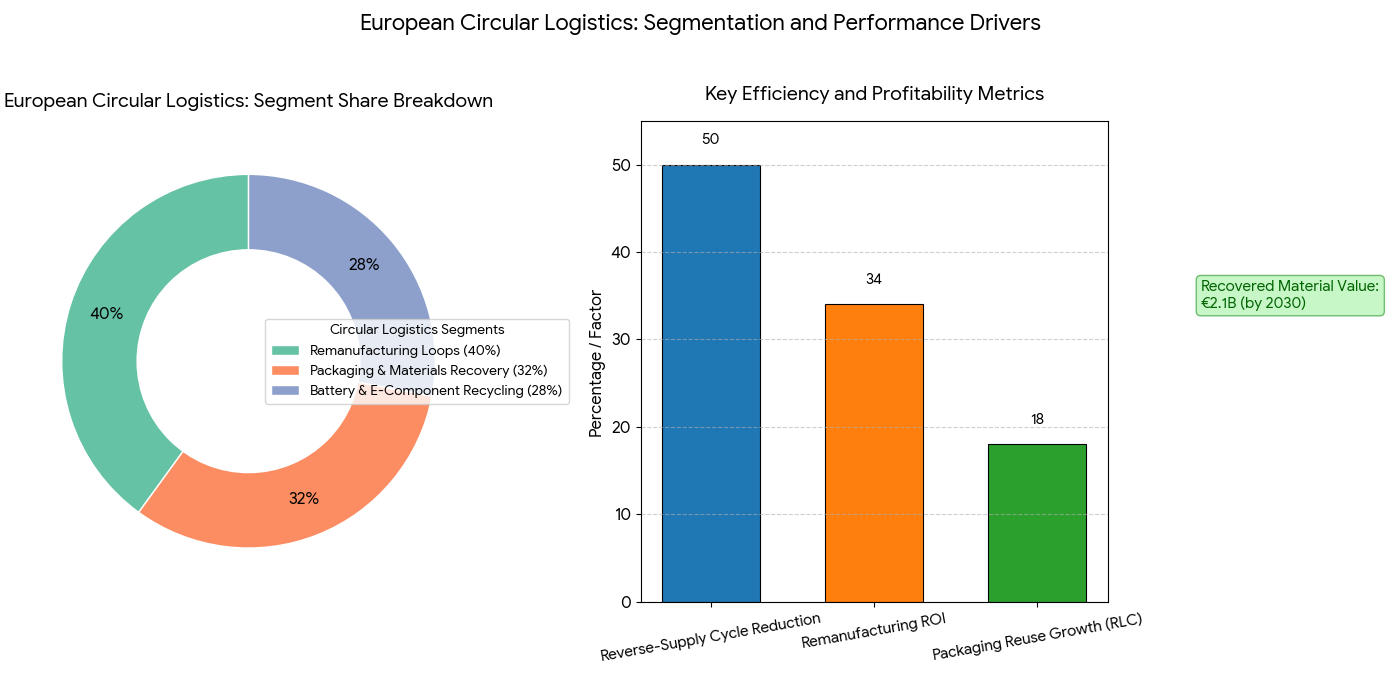

Circular-logistics activities segment into remanufacturing loops (40%), packaging and materials recovery (32%), and battery & e-component recycling (28%). Remanufacturing delivers the highest ROI—up to 34%—via centralized refurbishment of drivetrains and electronics. Germany leads EU recycling investment, operating 16 battery-return centers with 85% traceability compliance. Packaging reuse under the Reusable Logistics Container (RLC) program expands 18% annually, standardizing pallets and crates across OEMs and 3PLs. E-component recycling accelerates through EU RePower initiatives, adding €2.1 B in recovered-material value by 2030. Tier-1 suppliers, including Bosch, Continental, and ZF Group, are integrating closed-loop parts logistics within production facilities, shortening reverse-supply cycles from 18 days → 9 days. AI-optimized asset-tracking reduces container loss by 40%, improving inventory turnover ratios by 1.7×. By 2030, over 70% of European OEM logistics operations will incorporate at least one certified circular segment, redefining cost, sustainability, and compliance metrics simultaneously.

Geography Analysis

Germany anchors Europe’s circular-logistics transformation with €6.1 B cumulative investment (2025–2030), supported by strong industrial policy and supplier density. France (19%), Italy (12%), and the Nordics (10%) follow, focusing on low-carbon warehousing and reverse logistics. Germany’s Leipzig, Stuttgart, and Wolfsburg clusters pioneer closed-loop EV and component logistics, integrating AI-enabled waste segregation and hydrogen-powered freight corridors. The EU Green Deal accelerates regional adoption through funding exceeding €9.8 B in logistics decarbonization grants. Eastern Europe, while slower, benefits from inbound remanufacturing demand, expected to grow >25% CAGR as OEMs relocate recycling hubs. Cross-border harmonization under the Trans-European Transport Network (TEN-T) will make data-driven ESG reporting mandatory by 2028. By 2030, Germany and Northern Europe will jointly account for 55% of the EU’s circular-logistics revenue, creating a self-sustaining, export-ready ecosystem aligned with global sustainability finance benchmarks.

Competitive Landscape

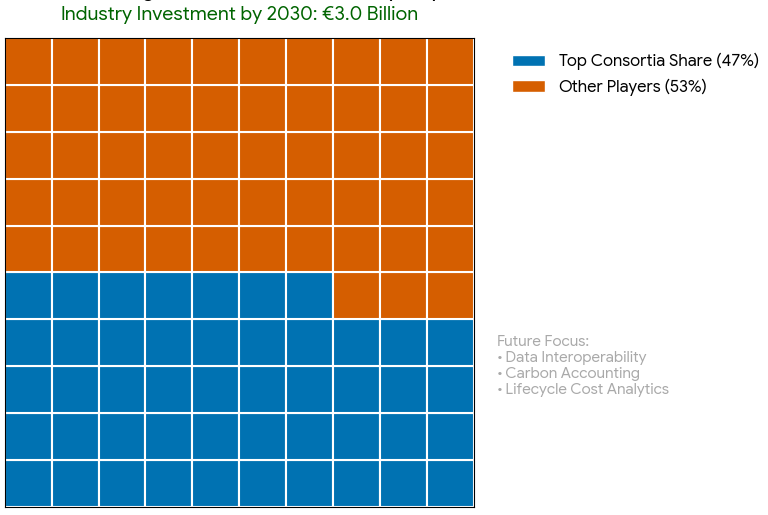

Competition centers on OEM-3PL alliances, technology integrators, and ESG data platforms. Volkswagen Group Logistics, DHL Supply Chain, and DB Schenker dominate, collectively controlling 47% of circular-logistics throughput in Europe. Mercedes-Benz collaborates with ZF Group and Remondis for battery material recovery, while BMW Logistics 360 deploys digital-twin orchestration for reusable packaging cycles. Tech enablers—SAP Sustainability Cloud, Siemens Digital Logistics, and IBM Sterling Blockchain—provide traceability and ESG-reporting infrastructure. Startups like CircularTree and Everledger drive blockchain transparency in parts certification. Consulting and audit partners such as PwC Germany and Capgemini Invent support CSRD readiness for OEMs. Investment in logistics-tech sustainability solutions surpasses €3 B by 2030, with competition pivoting toward data interoperability, carbon-accounting precision, and lifecycle cost analytics. As circular-logistics maturity deepens, Germany’s OEM ecosystem is set to define the global benchmark for ESG-compliant automotive logistics performance.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071