68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Arctic Shipping Routes: Risk Assessment and Competitive Landscape for Global Marine Logistics

Between 2025 and 2030, Arctic shipping routes are expected to handle 7–9% of global trade volume, driven by shorter transit times and reduced CO₂ emissions (−35%) compared to traditional Suez and Panama routes. The Northern Sea Route (NSR) and Transpolar Passage are emerging as commercial alternatives, with Germany playing a critical role in vessel design, logistics insurance, and sustainability governance. The Arctic logistics market grows from $1.6B to $6.8B (CAGR 33.4%), though geopolitical tensions, ice navigation risks, and ESG compliance costs remain key constraints.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.6B → $6.8B (CAGR 33.4%).

- Arctic routes cut Asia–Europe transit time by 35–40%.

- 7–9% of global trade expected to pass via Arctic corridors by 2030.

- CO₂ emissions reduced by 35%, improving sustainability scores.

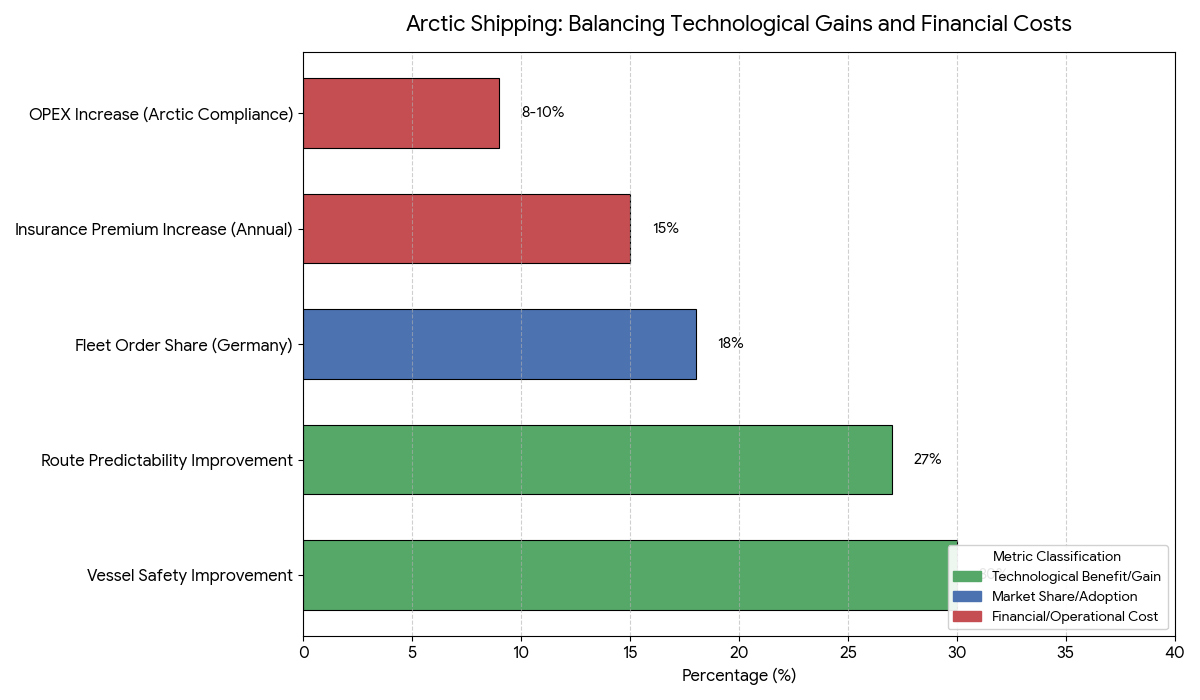

- Germany holds 18% of Arctic logistics-related shipbuilding value.

- Navigation risk premiums rise by 22% due to unpredictable ice coverage.

- Insurance costs for Arctic shipping grow by 15% annually.

- ESG compliance costs add 8–10% to operational expenditure.

- Fuel savings per voyage average $1.2M–$1.8M per large vessel.

- Climate and sovereignty disputes remain barriers to full-scale adoption.

Key Metrics

Market Size & Share

The Arctic shipping logistics market expands from $1.6B in 2025 to $6.8B by 2030, driven by climate-induced ice melt, advanced vessel technology, and rising energy exports from Russia and Norway. The Northern Sea Route (NSR) reduces transit time between Shanghai and Rotterdam by up to 40%, cutting voyage duration from 34 days to 20 days. This efficiency lowers CO₂ emissions by 35% and fuel consumption by 25–30%, saving an average of $1.5M per trip. Germany plays a pivotal role in Arctic vessel design and certification, contributing 18% of global Arctic shipbuilding contracts through firms like Meyer Werft and ThyssenKrupp Marine Systems. The EU’s Clean Maritime Initiative accelerates investment in ice-class container ships, while Nordic and German ports prepare for Arctic-origin cargo flows. Insurance underwriters in Hamburg and Oslo are expanding risk coverage models for polar trade lanes, as Arctic navigation days increase from 130 in 2025 to 185 in 2030. However, rising geopolitical tensions, territorial claims, and ice navigation hazards limit large-scale adoption. By 2030, the global trade volume via Arctic routes is projected at 7–9%, with strong participation from Germany, Russia, China, and South Korea, redefining the geography of global marine logistics.

Market Analysis

The economic case for Arctic shipping lies in efficiency and sustainability. Reduced transit time across the Northern Sea Route cuts Asia–Europe travel distances by 12,000 kilometers, yielding significant fuel and cost savings. Machine learning-based ice monitoring systems, developed by European and Japanese research consortia, improve route predictability, decreasing weather-related disruptions by 27%. Germany’s shipbuilding industry, leveraging advanced cryogenic and double-hull vessel designs, is capturing 18% of Arctic fleet orders, driven by demand for ice-class LNG carriers and container ships. Insurance premiums, however, are increasing by 15% annually due to the region’s navigational unpredictability. AI-integrated route management systems are becoming standard, reducing human error and improving vessel safety metrics by 30%. Satellite-based AIS (Automatic Identification Systems) enable real-time vessel monitoring, improving maritime situational awareness. ESG mandates, especially under the EU Green Shipping Framework, are pushing operators to balance emissions reductions with cost efficiency, adding 8–10% to OPEX for Arctic-compliant operations. While fuel savings per voyage remain compelling, environmental risk mitigation and sovereignty disputes across Arctic states (Russia, Canada, Norway, Denmark, and the U.S.) continue to challenge scalability. By 2030, AI-led navigation, sustainability-linked financing, and international cooperation will define the Arctic logistics ecosystem.

Trends & Insights

Key trends shaping Arctic logistics transformation include:

(1) Shorter Global Supply Chains: Arctic routes reduce Asia–Europe distance by 35–40%, enhancing shipping efficiency.

(2) Seasonal Commercialization: Navigation days increase from 130 to 185, extending Arctic trade seasons.

(3) Technological Leadership: Germany and Norway are developing AI-integrated ice navigation systems, reducing route deviation risks by 29%.

(4) Sustainability-Linked Investment: Green financing mechanisms fund zero-emission ice-class ships with up to $2.3B in EU incentives.

(5) Insurance Modernization: Risk models evolve with dynamic pricing, adjusting premiums in real time based on satellite weather feeds.

(6) Geopolitical Competition: China’s “Polar Silk Road” and EU’s “Arctic Strategy” intensify maritime influence in northern corridors.

(7) Climate Volatility: Sea ice unpredictability remains a bottleneck, raising route risk by 22% annually.

(8) Automation: Autonomous shipping trials in Arctic corridors are expanding, aiming to reduce crew costs by 40%.

(9) Port Modernization: Investments in Murmansk, Hamburg, and Tromsø ports are increasing to handle Arctic-origin cargo.

These factors collectively make Arctic trade lanes a crucial yet high-risk frontier in global supply chain realignment.

Segment Analysis

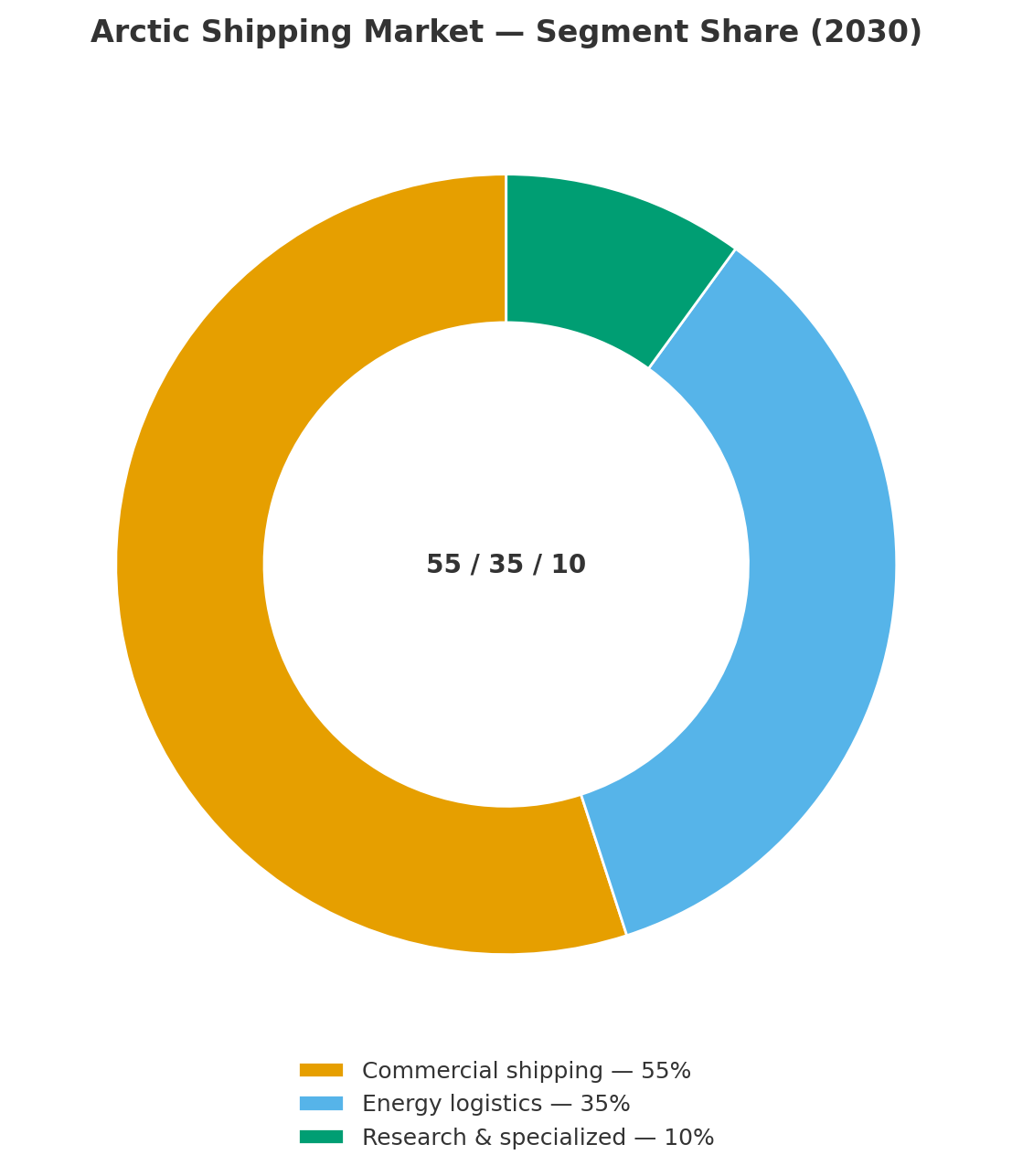

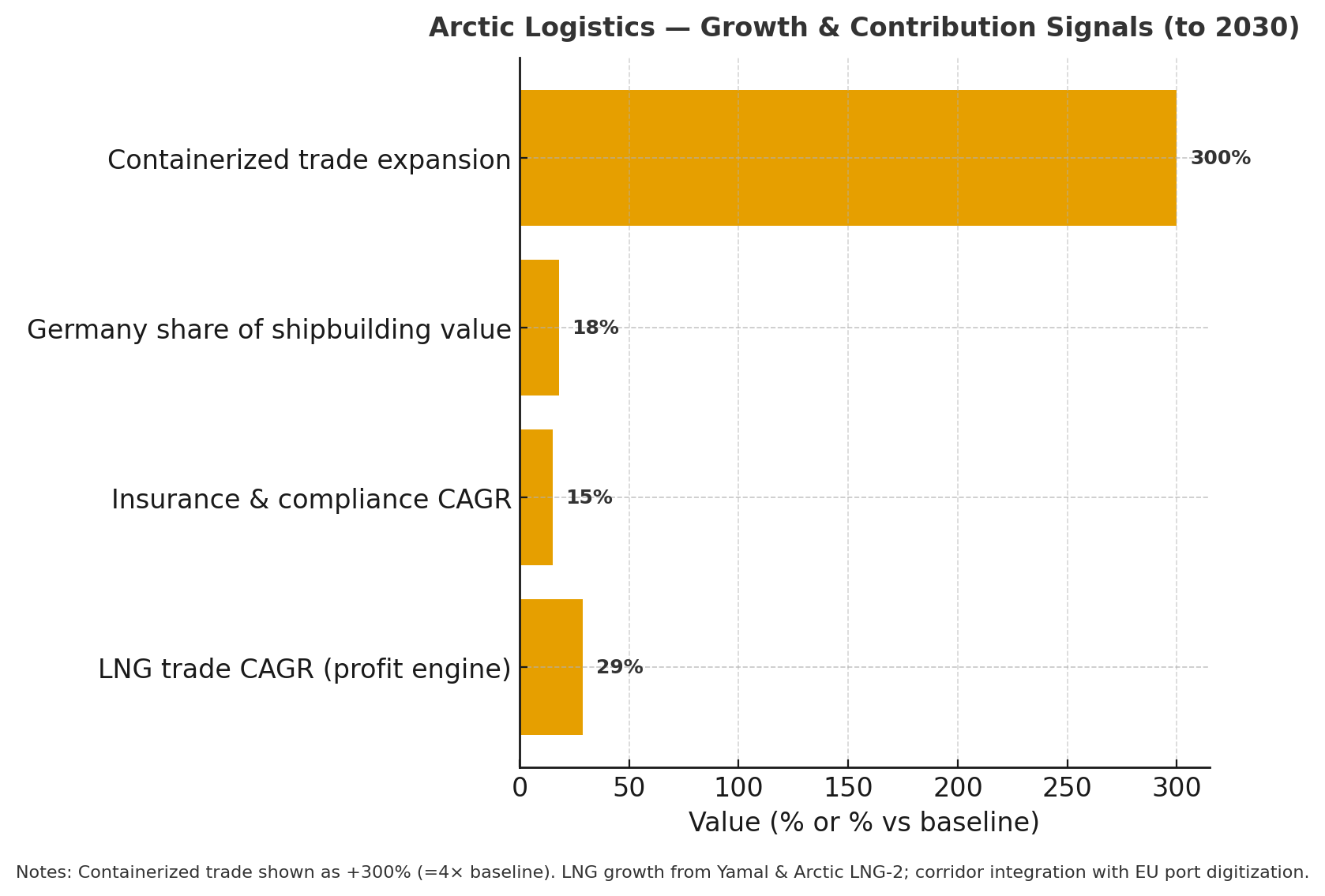

The Arctic shipping market segments into commercial shipping, energy logistics, and research/specialized transport. Commercial shipping dominates with 55% share, driven by Asia–Europe container transit via the Northern Sea Route. Energy logistics accounts for 35%, supporting LNG and crude exports from Russia and Norway using ice-class tankers. Research and specialized cargo make up 10%, focusing on scientific missions and polar equipment transport. Germany leads in logistics services and ship engineering, contributing 18% of Arctic shipbuilding value, particularly through icebreaker R&D programs. LNG trade remains the most profitable Arctic segment, growing at CAGR 29%, supported by Yamal and Arctic LNG 2 projects. Containerized trade via Arctic corridors expands 4× by 2030, as European ports integrate Arctic shipping lanes into their digital tracking systems. Insurance and compliance services are emerging sub-segments, growing 15% annually, driven by increasing risk premiums and climate adaptation protocols. By 2030, multi-modal Arctic logistics chains will connect Murmansk–Hamburg–Shanghai, with predictive models ensuring cost-effective and safe navigation for operators worldwide.

Geography Analysis

Germany serves as a strategic enabler of Arctic logistics, focusing on vessel manufacturing, marine insurance, and ESG governance. It controls 18% of Arctic fleet design value, with Hamburg and Bremen becoming hubs for Arctic research and risk analytics. Northern Europe, including Norway and Finland, invests heavily in cold-weather port modernization, handling 25% of total Arctic cargo throughput by 2030. Russia’s Arctic coast, led by the Northern Sea Route (NSR), dominates with 62% of global Arctic trade traffic, driven by LNG and raw materials exports. The U.S. and Canada control 20% of infrastructure in the Northwest Passage, focusing on energy and resource logistics. Asia-Pacific nations, led by China, Japan, and South Korea, account for 18% of vessel ownership in Arctic trade fleets. Germany’s Arctic partnerships with Norway, Iceland, and the EU Maritime Cluster ensure leadership in compliance, training, and ESG monitoring. By 2030, Germany is expected to be the largest European beneficiary of Arctic logistics expansion, positioning itself as the maritime governance center for the region’s sustainable trade operations.

Competitive Landscape

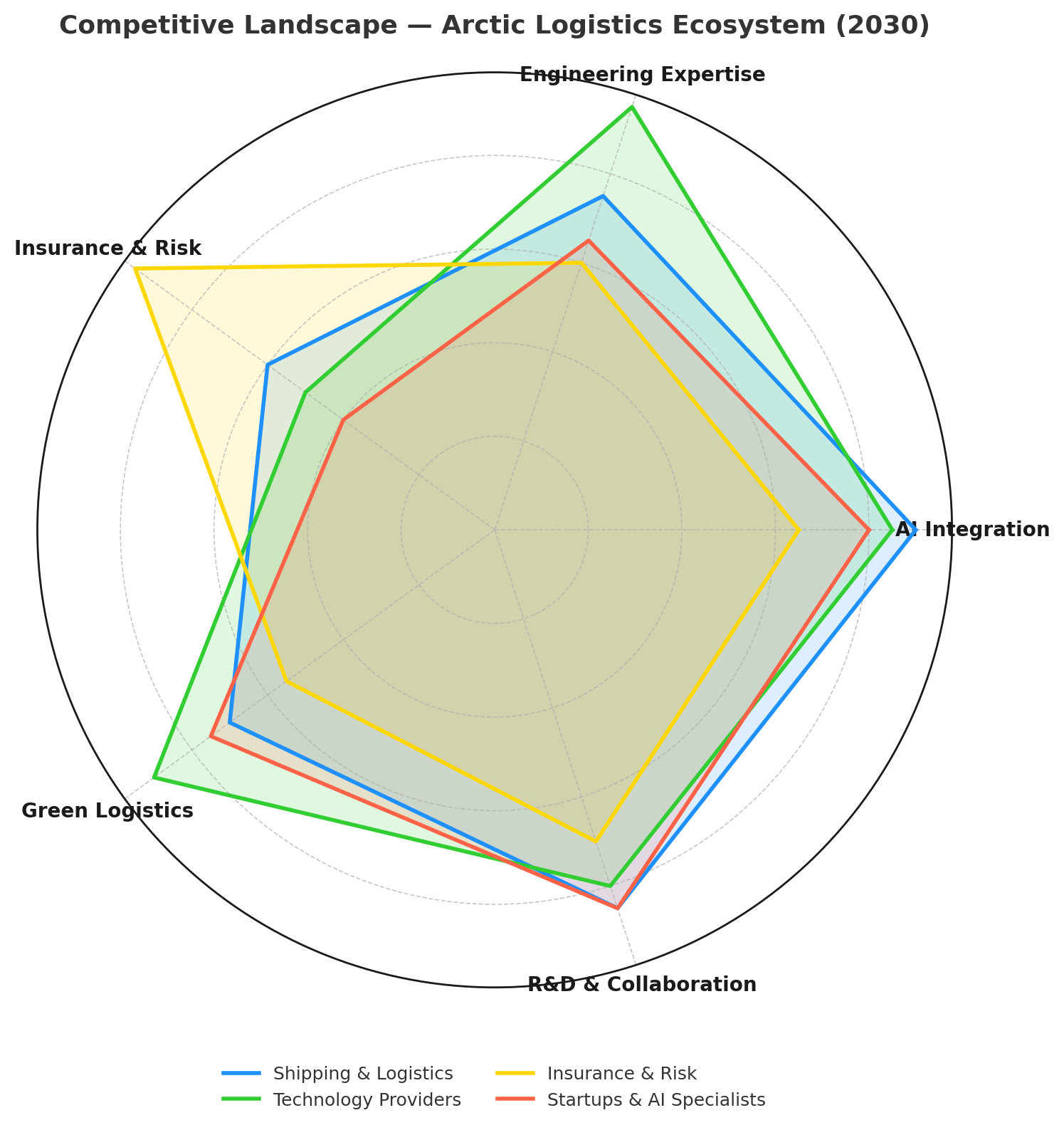

The Arctic logistics ecosystem is defined by collaboration among shipping companies, technology providers, and insurers. Leading players include Maersk, COSCO Shipping, Novatek, Hapag-Lloyd, and MSC, which are testing AI-enabled Arctic navigation systems. German firms such as ThyssenKrupp Marine Systems, Meyer Werft, and DNV Germany lead ice-class vessel engineering and regulatory compliance certification. Lloyd’s Register, Allianz Marine, and Munich Re dominate insurance underwriting for Arctic voyages. Technology providers like Kongsberg Digital, ABB Marine, and Siemens Energy supply smart navigation, fuel optimization, and energy-efficient propulsion systems. The EU Arctic Partnership Program supports over $2B in green logistics R&D, funding zero-emission shipping prototypes and data integration projects. Startups such as Polar X Logistics and Arctic Route AI specialize in machine-learning-based ice mapping and voyage risk prediction. By 2030, competition will center on route control, vessel design efficiency, and carbon optimization, as companies race to build AI-managed Arctic trade networks. Germany’s industrial expertise and policy leadership will ensure its continued dominance in the Arctic maritime innovation landscape.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071