68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

AI-Driven Cloud Compliance: Automated Auditing & Regulatory Change Management

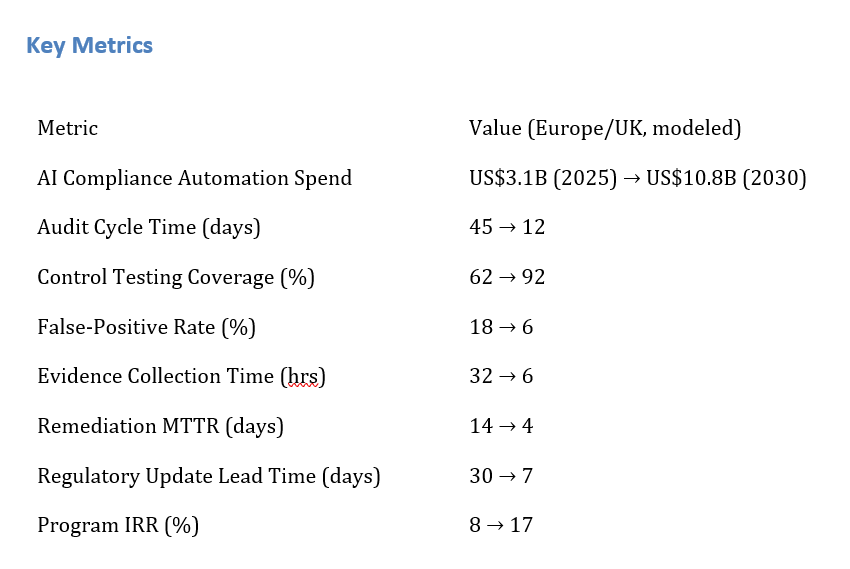

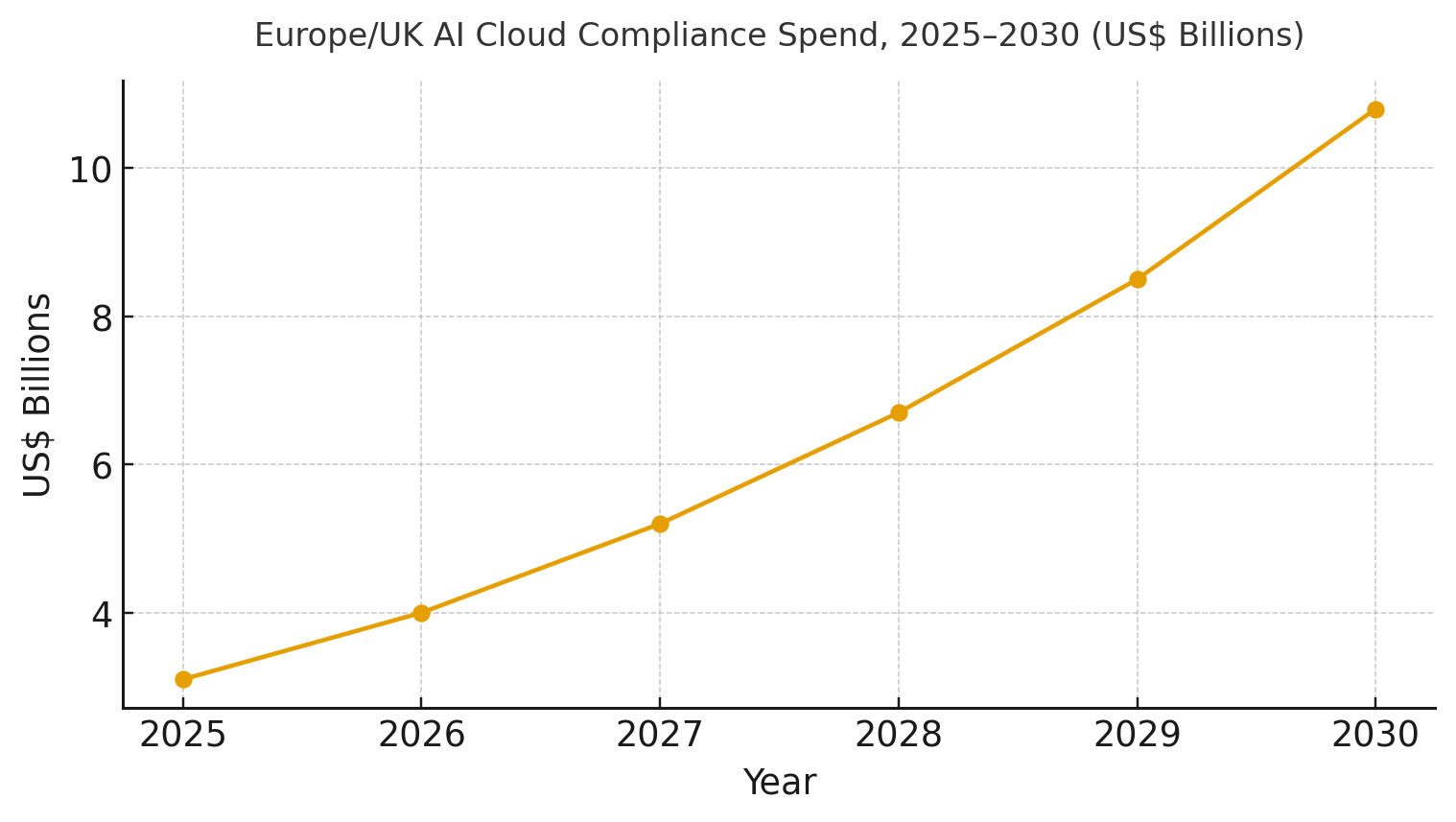

ChatGPT said:Enterprises in Europe and the UK are ramping up AI-driven cloud compliance to meet expanding regulations (GDPR, EU Data Act, NIS2, etc.) and manage multi-cloud estates. AI compliance automation spending is projected to grow from ~$3.1B in 2025 to ~$10.8B by 2030. Key impacts include reduced audit cycles (45 to 12 days), increased control testing coverage (62% to 92%), and lower false-positive rates (18% to 6%). Automation cuts evidence collection time (32 to 6 hours) and improves regulatory update speed (30 to 7 days). The program IRR is expected to rise from ~8% to ~17%. AI-driven compliance will lower risk and enable faster product releases.

What's Covered?

Report Summary

Key Takeaways

1. Continuous control monitoring replaces periodic audits with real-time assurance.

2. Policy-as-code standardizes controls across clouds and cuts drift MTTR.

3. Regulatory intelligence reduces update lead time from ~30 to ~7 days.

4. Automated evidence collection slashes audit prep from ~32 to ~6 hours.

5. Control coverage scales from ~62% to ~92% via API-driven tests and logs.

6. False positives fall to ~6% with context-aware models and asset graphs.

7. Third-party/SaaS risk is integrated into one control plane with attestations.

8. CFO dashboard: cycle time, coverage %, FP %, evidence hrs, MTTR days, update days, IRR %.

a) Market Size & Share

Europe/UK AI cloud compliance spend is modeled to grow from ~US$3.1B (2025) to ~US$10.8B (2030) as enterprises adopt CCM, policy-as-code, and regulatory intelligence to address GDPR, DORA, NIS2, EU AI Act alignments, and UK supervisory expectations. The line figure shows the investment ramp. Share accrues to platforms that integrate multi-cloud APIs, evidence lakes with lineage, and change-management pipelines that translate new rules into testable controls. Execution risks: tool sprawl, weak asset inventories, and fragmented ownership; mitigations: single control planes, asset graphs, and federated operating models across security, risk, and engineering.

b) Market Analysis

Quantified gains underpin the business case for AI-driven compliance. We model audit cycle time falling from ~45→~12 days, control testing coverage rising from ~62→~92%, false positives shrinking from ~18→~6%, evidence collection hours dropping from ~32→~6, remediation MTTR from ~14→~4 days, and regulatory update lead time from ~30→~7 days by 2030. Program IRR expands from ~8→~17% as fines and labor are reduced and product teams ship faster with gates codified as tests. Enablers: policy-as-code, evidence automation, graph-based asset context, and regulatory NLP. Barriers: legacy change processes, multi-cloud fragmentation, and third-party blind spots.

Financial lens: combine avoided penalties and audit savings with acceleration value (sooner revenue from faster releases). The bar figure summarizes the KPI shifts achieved under disciplined programs.

c) Trends & Insights

1) Policy-as-code repositories become the contract between compliance and engineering. 2) Evidence lakes unify logs, tickets, and scans with lineage and immutability. 3) Regulatory intelligence pipelines diff new rules and auto-generate control updates. 4) Graph-based inventories bring context to alerts, reducing false positives. 5) Human-in-the-loop review focuses on exceptions and model drift. 6) Automated vendor evidence ingestion normalizes SIG/CAIQ and SOC reports. 7) Data residency-as-code enforces localization and transfer rules. 8) Green compliance ops: rightsizing scans and storing cold evidence cheaply. 9) Real-time dashboards tie control status to release gates. 10) Collaboration models merge security, risk, legal, and platform engineering.

d) Segment Analysis

Financial Services: DORA/NIS2 alignment, strict RTO/RPO, and continuous vendor oversight. Healthcare/Life Sciences: GDPR + MDR, strong PHI controls and evidence chains. Retail/CPG: high SaaS footprint; focus on vendor attestations and data minimization. SaaS/Tech: SOC 2 & ISO 27001 automation; privacy impact assessments integrated with CI/CD. Public Sector: data sovereignty and residency-as-code. Across segments, KPIs: cycle time, coverage %, FP %, MTTR days, update days, and IRR. Pricing models mix per-asset, per-tenant, and evidence storage tiers.

e) Geography Analysis

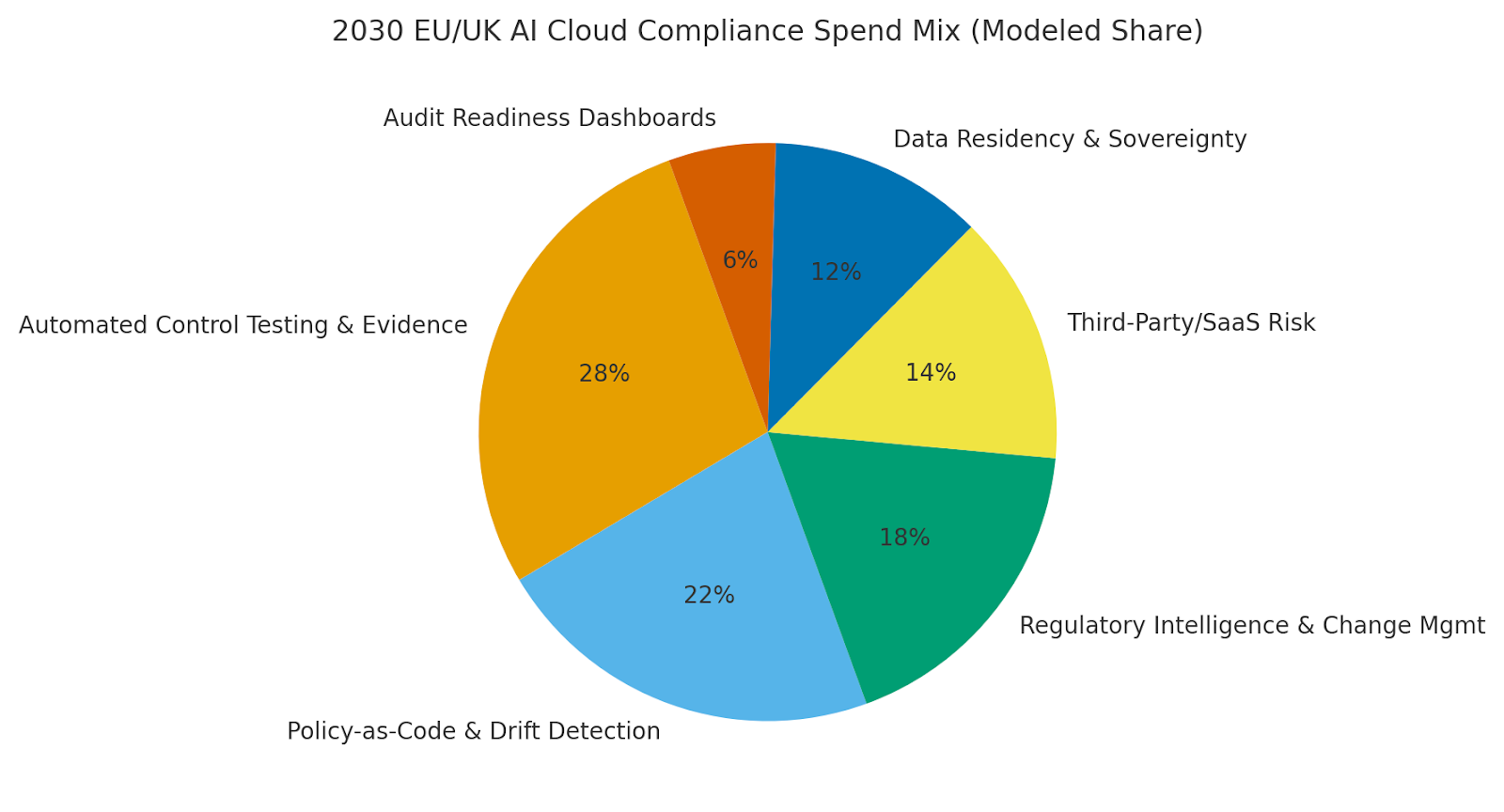

By 2030, we model EU/UK spend distribution across use cases as: Automated Control Testing & Evidence (~28%), Policy-as-Code & Drift Detection (~22%), Regulatory Intelligence & Change Mgmt (~18%), Third-Party/SaaS Risk (~14%), Data Residency & Sovereignty (~12%), and Audit Dashboards (~6%). The pie figure reflects this mix. UK financial hubs lead early due to DORA/NIS2 equivalence and sector expectations; EU growth centers on regulated industries and public sector modernization. Execution priorities: unify inventories, codify rules, and automate evidence pipelines; measure coverage %, MTTR, and update lead time per region.

f) Competitive Landscape

Vendors span cloud-native compliance platforms, governance suites, and vertical specialists. Differentiation vectors: (1) depth of policy-as-code and multi-cloud coverage, (2) evidence ingestion and lineage, (3) regulatory NLP accuracy, (4) third-party risk integration, and (5) time-to-value with playbooks and templates. Procurement guidance: require open APIs, mappable controls to major frameworks, attestation support, and provable KPI impact. Competitive KPIs: cycle time, coverage %, false-positive %, MTTR days, update lead time, and IRR uplift.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1350

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071