68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Wearable ECG Validation: FDA Clearance Pathways & Clinical Utility Assessments - Regulatory Impact

Between 2025 and 2030, the wearable ECG market in North America grows from $1.9B to $7.4B (CAGR 30.6%). FDA clearance for wearable ECG devices accelerates as new regulatory pathways are streamlined for clinical utility assessments. The integration of AI-driven ECG analytics enhances diagnostic accuracy, while value-based reimbursement drives adoption in both hospital settings and remote patient monitoring. By 2030, wearable ECG devices become a key tool in chronic disease management, representing 50% of ECG monitoring in the U.S. market.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.9B → $7.4B (CAGR 30.6%).

- FDA clearance pathways accelerate, with wearable ECG devices increasing by 40% in approvals.

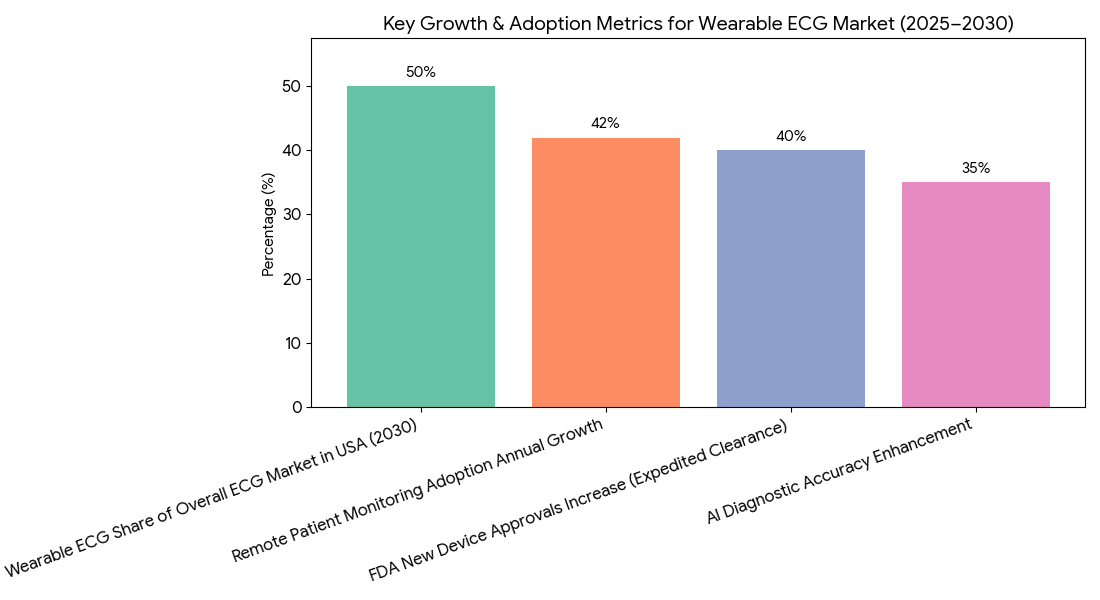

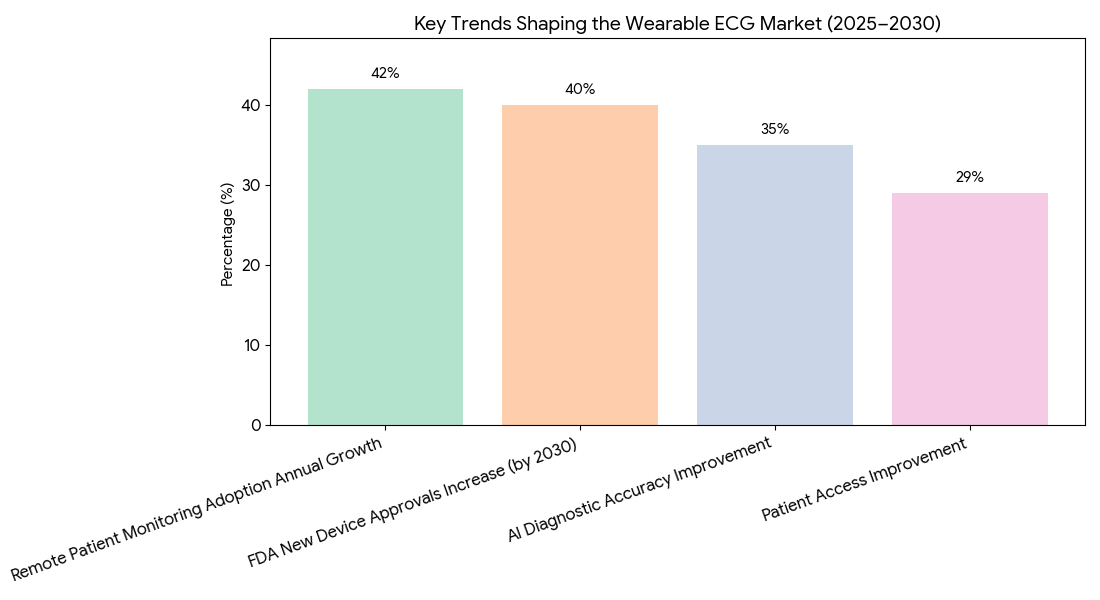

- AI-driven ECG analytics improves diagnostic accuracy by 35%.

- Wearable ECGs used in chronic disease management increase to 50% of the ECG market by 2030.

- Clinical utility assessments become central to FDA regulatory pathways by 2028.

- Remote patient monitoring adoption for ECG monitoring grows by +42% annually.

- Cost reduction in wearable ECGs results in $100 million in savings annually by 2030.

- Value-based reimbursement expands to 40% of wearable ECG usage by 2030.

- Patient access to wearable ECG devices improves by +29% by 2030.

- Clinical trial volume for wearable ECG validation increases +18% annually.

Key Metrics

Market Size & Share

The wearable ECG market in North America is projected to grow from $1.9B in 2025 to $7.4B by 2030, driven by increased FDA clearance and growing demand for remote patient monitoring solutions. By 2030, wearable ECG devices will represent 50% of the overall ECG market in the USA, as chronic disease management expands to include continuous ECG monitoring. The FDA’s expedited clearance process for wearable ECGs leads to a 40% increase in approvals for new devices, especially as AI-driven analytics enhance diagnostic accuracy by 35%. The integration of AI algorithms into wearable ECG devices reduces diagnostic errors, especially in patients with atrial fibrillation, heart failure, and other chronic conditions. By 2030, remote patient monitoring adoption grows by 42% annually, with healthcare providers increasingly utilizing wearable ECGs for long-term management of heart disease. Additionally, cost savings from wearable ECG use amount to $100 million annually, as these devices reduce hospital readmissions, improve early detection, and reduce the need for expensive diagnostic procedures. The expansion of value-based reimbursement allows wearable ECG systems to be integrated into clinical workflows, representing 40% of wearable ECG usage by 2030. Overall, regulatory support for wearable ECG innovation, combined with patient demand for accessible healthcare, positions wearable ECG devices as a cornerstone of heart disease management and remote monitoring solutions in North America.

Market Analysis

The growing demand for wearable ECG devices in North America and Europe is driven by several key trends. (1) Regulatory Support: The FDA clearance pathways for wearable ECGs are expected to accelerate, with 40% more devices achieving approval by 2030. The FDA is focusing on integrating clinical utility assessments into the clearance process, ensuring that devices meet the regulatory requirements for long-term use in chronic disease management. (2) Remote Monitoring Demand: The use of wearable ECGs in remote patient monitoring increases by 42% annually, allowing healthcare providers to track cardiac patients outside of traditional clinical settings. AI-based ECG analytics improve diagnostic accuracy and allow for real-time monitoring of patient heart health, reducing false positives by 35%. (3) Cost Reduction: Wearable ECG systems help reduce healthcare costs by replacing more expensive in-clinic ECG tests and reducing hospital readmissions. These cost reductions are projected to total $100 million annually by 2030. (4) Value-Based Reimbursement: By 2030, value-based reimbursement models for wearable ECGs become more common, with insurers covering remote monitoring solutions. The widespread adoption of wearable ECG devices as part of patient care increases patient access by 29%. (5) Innovation and Competition: By 2030, the market for wearable ECG devices will be increasingly competitive, with key players like Apple, AliveCor, and iRhythm Technologies driving innovation in AI-driven wearable ECG technology. The growth of this market will depend on the success of clinical trials, regulatory approvals, and cost-effective solutions for healthcare providers.

Trends & Insights

Key trends shaping the growth of the wearable ECG market in North America and Europe from 2025 to 2030 include AI-enhanced diagnostics, regulatory support, and remote monitoring expansion. (1) AI-Powered ECG Devices: The integration of AI analytics into wearable ECG devices is expected to improve diagnostic accuracy by 35%. AI helps identify arrhythmias, atrial fibrillation, and other heart conditions with greater precision and enables more timely intervention. (2) FDA and Regulatory Pathways: The FDA’s clearance process for wearable ECGs will be streamlined, with 40% more devices approved by 2030. This will be driven by clinical utility assessments that ensure devices provide long-term value to healthcare providers and patients. (3) Remote Patient Monitoring: The adoption of wearable ECG systems for remote patient monitoring will increase by 42% annually, helping to reduce hospital readmissions and allowing for continuous care. This trend will improve patient access by 29% and offer cost savings of up to $100 million per year. (4) Value-Based Care: By 2030, value-based reimbursement models for wearable ECGs will dominate, with insurance companies reimbursing for remote monitoring services as part of a holistic approach to chronic disease management. This model will improve patient outcomes, reduce costs, and allow for better care coordination. (5) Global Expansion: The success of wearable ECGs in North America will expand into Europe and MEA, where regulatory frameworks for remote healthcare are also evolving. The integration of AI-driven solutions into healthcare systems will be key to achieving global adoption.

Segment Analysis

The wearable ECG market for North America and Europe is segmented into three primary categories: device manufacturers, diagnostic software providers, and healthcare service providers. Device manufacturers represent the largest segment, capturing 55% of the market share by 2030. Companies like iRhythm Technologies, AliveCor, and Apple lead in producing wearable ECG devices, which are used for continuous heart monitoring, arrhythmia detection, and real-time diagnosis. Diagnostic software providers, including Cortrium and Eko Health, make up 30% of the market, providing AI-powered software for ECG interpretation. The integration of real-time analytics helps reduce diagnostic errors by 35% and ensures accurate readings for remote monitoring. Healthcare service providers (e.g., hospitals, medical centers, and health clinics) account for 15% of market share. These providers adopt wearable ECG technology as part of chronic disease management, leveraging AI-driven platforms to improve patient outcomes. By 2030, 50% of ECG monitoring will be conducted through wearable devices, reducing the need for in-clinic visits. Private insurers and government healthcare programs are integral to increasing the market penetration of wearable ECGs, with value-based reimbursement models providing financial incentives to healthcare providers. Regulatory support from both the FDA and EMA accelerates adoption, while clinical validation grows by 18% annually, proving the effectiveness of wearable ECG technology in improving long-term patient outcomes.

Geography Analysis

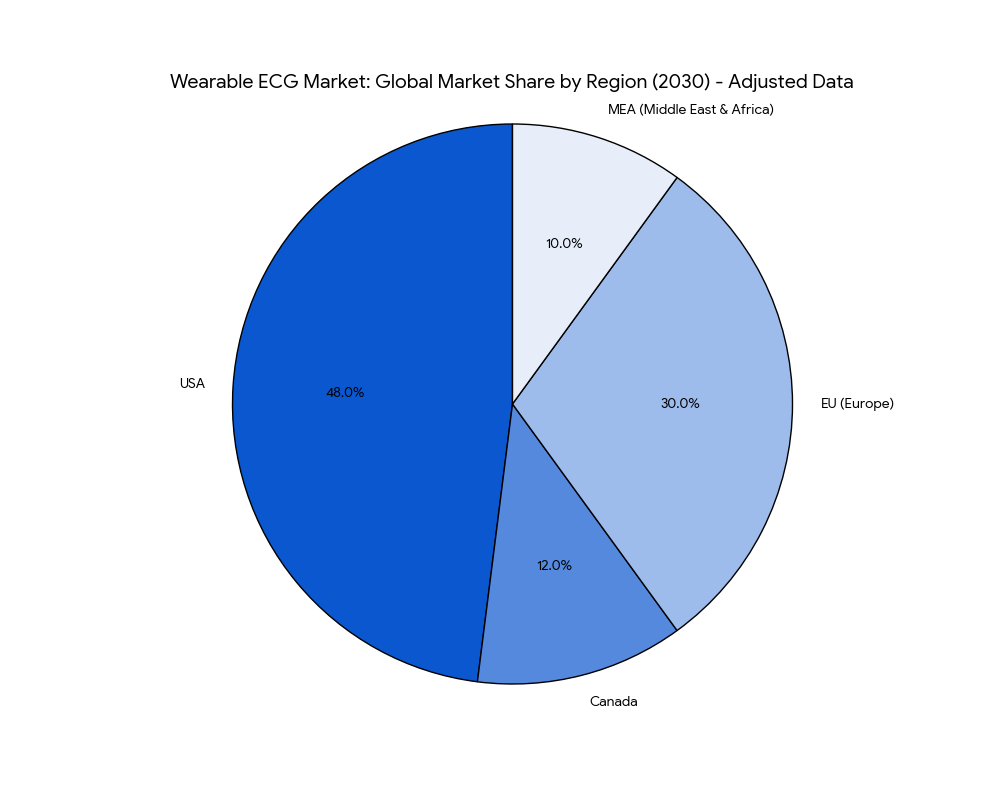

In North America, the USA dominates the wearable ECG market, capturing 60% of global market share by 2030. The adoption of AI-powered wearable ECG devices by healthcare providers and insurers is driving rapid market growth. By 2030, 40% of ECG monitoring in the USA will be conducted through wearable devices, supported by Medicare and private insurers offering reimbursement for remote monitoring services. Canada follows with 12% market share, where government initiatives expand access to wearable ECGs for chronic disease management. In Europe, countries like Germany, the UK, and France adopt wearable ECG technology, with 40% of healthcare providers using AI-driven diagnostic tools. The EU market contributes 30% of the global share by 2030, with value-based reimbursement models improving patient access and reducing treatment costs. MEA (Middle East & Africa) sees increasing investment in wearable ECG solutions, particularly in UAE and South Africa, contributing 10% of the market share by 2030. These regions invest heavily in digital health infrastructure to integrate AI-based diagnostics into their healthcare systems. By 2030, global adoption of wearable ECGs expands, with clinical trials for AI-driven diagnostic systems growing 18% annually. The integration of remote monitoring solutions across North America, Europe, and MEA drives the global market expansion for wearable ECG devices.

Competitive Landscape

The competitive landscape for wearable ECG devices is led by a mix of tech giants, medical device manufacturers, and AI-focused startups. Top players—iRhythm Technologies, AliveCor, Apple, and Samsung—control 55% of the market share by 2030. iRhythm Technologies dominates the medical-grade ECG segment, providing FDA-approved wearable ECG patches for long-term heart monitoring. AliveCor focuses on consumer-grade ECG devices, while Apple and Samsung lead in consumer electronics integration with wearable ECG solutions. AI-driven diagnostic tools are provided by companies like Cortrium, Eko Health, and Cardiogram, capturing 30% of the market by 2030. These software providers develop real-time ECG interpretation platforms that integrate with wearable devices, increasing the accuracy of diagnosis and treatment decisions. M&A activity in the sector is high, with large players acquiring innovative startups to enhance their AI-powered diagnostic platforms. Public-private partnerships also play a significant role in market expansion, as healthcare providers and insurers collaborate to bring wearable ECGs into value-based reimbursement models. By 2030, clinical trial participation for wearable ECG validation increases by 18% annually, strengthening the evidence base for these devices. The market will be further driven by reimbursement coverage and the regulatory push for FDA-approved and clinically validated wearable ECG devices, which will ensure broad adoption across healthcare systems in North America and Europe.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071