68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Voice Commerce Adoption in Emerging Markets: AI-Powered Personalization & Multilingual Interface Challenges

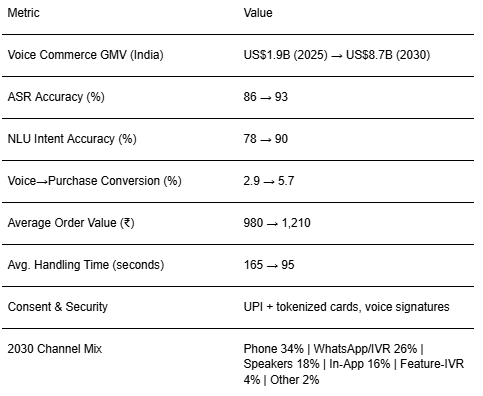

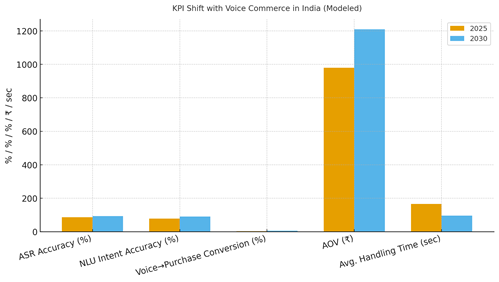

India’s next commerce interface speaks and understands. Between 2025 and 2030, voice becomes a credible shopping surface as automatic speech recognition (ASR), natural‑language understanding (NLU), and payments rails converge in multiple Indian languages. We model voice‑led GMV expanding from ~US$1.9B (2025) to ~US$8.7B (2030), with growth propelled by smartphone assistants, WhatsApp/IVR bots, and smart displays in households. Gen‑Z and first‑time e‑commerce users adopt voice for convenience, hands‑free search, and assisted discovery (recipes, routines, how‑to flows). The operating system has five layers. (1) Acquisition: assistant‑optimized SEO, vernacular ads, and contact‑book seeding for WhatsApp; (2) Understanding: multilingual ASR and intent models tuned for code‑switching and regional accents; (3) Personalization: zero‑party preferences, purchase history, and contextual prompts; (4) Transactions: UPI and tokenized cards, COD gating, and consented voice signatures; (5) Service: order status, returns, and cross‑sell delivered through dialog. Our modeled KPI shifts: ASR accuracy improves from ~86% to ~93%; NLU intent accuracy from ~78% to ~90%; voice→purchase conversion from ~2.9% to ~5.7%; average order value from ~₹980 to ~₹1,210; and average handling time drops from ~165s to ~95s as flows compress.

What's Covered?

Report Summary

Key Takeaways

1. Design for code‑switching: mixed Hindi‑English and regional dialects.

2. Short, stateful dialogs cut handling time and abandonment.

3. UPI and tokenized cards make payments natural; add COD gates for risk.

4. Personalize with remembered preferences and routines (opt‑in).

5. Fallback to tap/text when confidence is low; never trap users in voice.

6. Use WhatsApp/IVR to reach beyond app installs; seed contact‑book.

7. Measure equity: accuracy and completion rates by language and gender.

8. CFO dashboard: ASR %, NLU %, voice→purchase %, AOV, AHT, and LTV.

Key Metrics

Market Size & Share

India’s voice commerce GMV is modeled to grow from ~US$1.9B in 2025 to ~US$8.7B by 2030. Share accrues to operators who combine assistant SEO, vernacular ads, and device‑agnostic dialogs. Categories with habitual reorders (grocery, household, beauty basics) lead adoption; complex sizing/spec categories lag until confidence scores and visual fallbacks improve. The line figure charts the modeled trajectory.

Stack shares: ASR/NLU models tuned for code‑switching; identity and consent; payments with UPI and tokenized cards; dialog management; and service automation. Execution risks: platform policy shifts, poor IVR UX, and model bias. Mitigations: multi‑channel reach, short prompts with slot‑filling, and equity dashboards tracking accuracy and completion by language and gender. Share should be tracked via GMV by channel, voice→purchase %, AOV, AHT, and LTV.

Market Analysis

Experience quality drives conversion and cost. We model ASR accuracy rising from ~86% to ~93%, NLU intent accuracy from ~78% to ~90%, voice→purchase conversion from ~2.9% to ~5.7%, AOV from ~₹980 to ~₹1,210, and average handling time falling from ~165s to ~95s. Enablers: multilingual ASR/NLU, stateful dialogs, UPI payments, and CRM‑backed personalization. Barriers: noisy environments, accent diversity, and inconsistent device mics.

Financial lens: attribute incremental sales net of call/session costs; reduce AHT to protect service P&L; and cap COD exposure using address and risk scores. The bar chart summarizes directional KPI movement under disciplined voice commerce design.

Trends & Insights

1) Code‑switching becomes default Hindi‑English and regional blends must be first‑class. 2) Micro‑prompts and proactive suggestions reduce AHT. 3) Smart displays marry voice with visuals for complex choices. 4) WhatsApp and IVR extend reach beyond apps. 5) Voice signatures and tokenized payments normalize checkout. 6) Bias monitoring dashboards report accuracy and completion by language and gender. 7) Creator‑style prompts and sonic branding enhance recall. 8) Voice CRM remembers preferences and replenishment cycles. 9) Offline‑first logging protects against patchy networks. 10) MMM and geo/HH holdouts calibrate budget across search, social, and voice to true incrementality.

Segment Analysis

Grocery & Household: Routine reorders; strongest AHT reduction and repeat. Beauty & Personal Care: Guided selection; upsell kits; returns drop with expectation‑setting. Electronics & Accessories: Spec queries, warranty registration; higher need for visual fallback. Fashion: Size/fit questions; hybrid voice + link‑to‑chat flows. Bill Pay/Services: High completion and AHT gains; fraud checks essential. Across segments, define prompts, fallback paths, and risk controls; track ASR %, NLU %, voice→purchase %, AOV, AHT, and repeat by category.

Geography Analysis

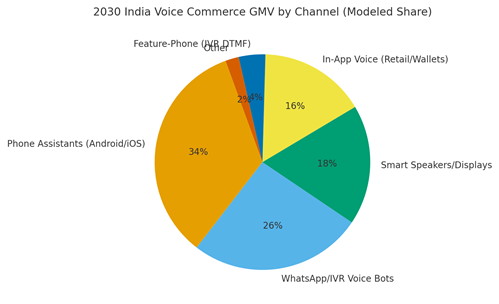

By 2030, India’s channel/device mix for voice commerce GMV is modeled as Phone Assistants (~34%), WhatsApp/IVR (~26%), Smart Speakers/Displays (~18%), In‑App Voice (~16%), Feature‑Phone IVR (~4%), and Other (~2%). Metros adopt smart displays earlier; Tier‑2/3 growth is led by WhatsApp/IVR and phone assistants. The pie figure reflects the modeled mix.

Execution: stage rollouts by state/language; benchmark accuracy and AHT by region; and tune COD and UPI flows to local risk profiles. Measure geography‑specific voice→purchase %, AHT, AOV, and repeat; reallocate budget based on incremental ROI.

Competitive Landscape

Assistant platforms, telco/WhatsApp ecosystems, and retail apps with embedded voice compete for share. Differentiation vectors: (1) multilingual ASR/NLU quality and bias controls, (2) UPI payment depth and consent UX, (3) dialog design and AHT compression, (4) visual fallback and cross‑device continuity, (5) CRM and identity integration. Procurement guidance: demand per‑language accuracy SLAs, PCI scopes, tokenized payment support, and analytics for confidence and fallback events. Competitive KPIs: ASR %, NLU %, voice→purchase %, AOV, AHT, repeat rate, and cost/session.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071