68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Subscription Box Economics: Customer Lifetime Value Optimization in European Beauty Markets

European beauty subscriptions are shifting from discovery‑only to LTV‑engineered membership programs that blend curation, community, and replenishment. From 2025 to 2030, we model EU beauty subscription box revenues rising from ~US$3.2B to ~US$6.2B as operators tighten unit economics: higher 12‑month retention, lower monthly churn, disciplined CAC, and faster payback via smarter merchandising and logistics. Benelux including Luxembourg over‑indexes on digital adoption, cross‑border fulfillment, and multilingual content, making it attractive for high‑ARPU pilots. CLV playbook: (1) Value ladders Good/Better/Best plans with refill credits, early access, and member pricing; (2) Personalization quiz + usage telemetry to select hero SKUs and minimize ‘shelf of shame’; (3) Logistics right‑sized packaging, regional DCs, and returns‑lite swaps to cut cost per shipment; (4) Content & community creator capsules, member‑only livestreams, and referral missions; (5) Risk churn prevention via pause/skips, at‑risk outreach, and proactive refunds for stockouts. Measurement shifts from GMV to CLV accounting: ARPU/month, 12‑month retention, CAC payback, and LTV/CAC by cohort.

What's Covered?

Report Summary

Key Takeaways

1. Design tiers to trade up ARPU without spiking churn.

2. Use quiz + usage data to cut mismatch and returns.

3. Refill credits and skips reduce cancellation intent.

4. Regional DCs and right‑sized packs lower cost/ship.

5. Creator capsules and member events lift referral K‑factor.

6. Holdouts prove incrementality of offers and content.

7. Consent‑first renewals and easy downgrades protect trust.

8. CFO dashboard: retention %, churn %, ARPU, CAC payback, LTV/CAC, refund rate.

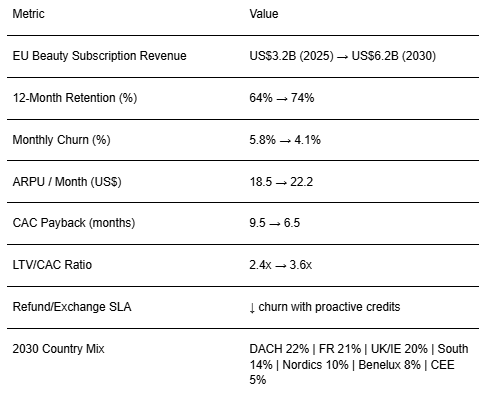

Key Metrics

Market Size & Share

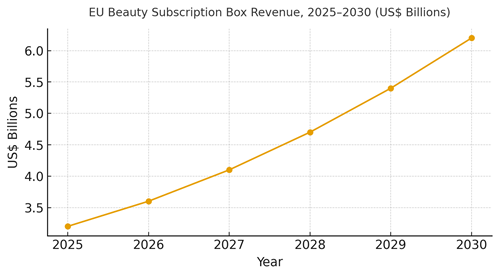

EU beauty subscription revenues are modeled to grow from ~US$3.2B in 2025 to ~US$6.2B by 2030, powered by premiumization, refill bundles, and hybrid commerce (box + add‑on shops). France, DACH, and the UK/IE cluster lead scale; Benelux including Luxembourg delivers outsize ARPU and low churn due to affluent, multilingual households and cross‑border convenience. The line figure shows the trajectory.

Share dynamics: operators that combine vendor‑funded sampling with curated refills gain margin share; those that align retail media and creator capsules unlock lower CAC and faster payback. Execution risks: supply volatility for hero SKUs, shade/season mismatch, and fulfillment delays; mitigations include dual‑sourcing, dynamic bundles, and promise‑date SLAs. Share should be tracked by active subscribers, ARPU, and LTV/CAC across country cohorts.

Market Analysis

CLV optimization compounds small gains across the funnel. We model 12‑month retention improving from ~64% to ~74%, monthly churn decreasing from ~5.8% to ~4.1%, ARPU/month rising from ~US$18.5 to ~US$22.2, CAC payback tightening from ~9.5 to ~6.5 months, and LTV/CAC moving from ~2.4x to ~3.6x by 2030. Enablers: segmentation by needs and spend potential, A/B‑tested tier ladders, refill credits, and pause/skip mechanics. Logistics right‑sized packaging and regional DCs reduces cost/ship and late deliveries that trigger churn. The bar chart summarizes the directional KPI shifts under disciplined CLV ops.

Trends & Insights

1) From discovery to replenishment: refill bundles stabilize ARPU. 2) Zero‑party data: quizzes and usage telemetry tailor boxes and reduce waste. 3) Creator‑commerce: capsules and live sessions compress time‑to‑purchase. 4) Retail media tie‑ins: authenticated audiences lift match rates and CAC. 5) Flexible memberships: pause/skip and family plans reduce churn friction. 6) EU compliance: explicit consent, renewal reminders, easy downgrades. 7) Supply resilience: dual‑sourcing for hero items; dynamic substitutions. 8) Sustainable ops: right‑sized packs and local DCs cut emissions and damage. 9) Add‑on shops: high‑margin upsell with loyalty pricing. 10) Cohort P&L: CLV accounting guides category expansion and vendor terms.

Segment Analysis

Skin Care: Routine‑based bundles; high retention; shade agnostic. Make‑Up: Shade/season risk; higher churn without quizzes and swaps. Hair Care: Regimen and size variants; strong refill economics. Fragrance: Discovery value via vials; convert to full‑size with credits. Men’s Grooming: Simpler assortments; strong pause/skip utility. Clean & Derm Brands: Higher trust; premium ARPU. Across segments, define assortment rules, refill cadence, and swap/return policies; track retention %, churn %, ARPU, CAC payback, and LTV/CAC by segment.

Geography Analysis

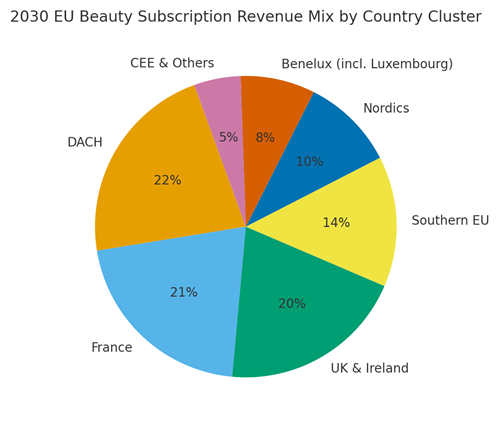

By 2030, EU beauty subscription revenue mix is modeled as DACH (~22%), France (~21%), UK & Ireland (~20%), Southern EU (~14%), Nordics (~10%), Benelux (including Luxembourg) (~8%), and CEE & Others (~5%). Luxembourg’s proximity to FR/DE/BE enables cross‑border delivery promises and multi‑language content, supporting premium tiers with stable retention. The pie figure reflects the country‑cluster mix.

Execution: localize brand/style preferences, VAT and returns; stage Luxembourg‑centric pilots for premium tiers and refill bundles; and expand to nearby regions with similar ARPU and churn profiles. Measure geography‑specific retention, churn, ARPU, CAC payback, and LTV/CAC; reallocate budgets quarterly.

Competitive Landscape

Incumbent beauty subs lean on discovery and sampling; challengers emphasize refill bundles, derm guidance, and creator capsules. Differentiation vectors: (1) CLV discipline and cohort P&L, (2) zero‑party data quality, (3) supply resilience and fulfillment SLAs, (4) retail media and creator efficiency, and (5) compliance and renewal UX. Procurement guidance: require open APIs, cohort dashboards, returns‑lite swaps, and vendor‑funded trials. Competitive KPIs: retention %, churn %, ARPU, CAC payback, LTV/CAC, refund rate, and on‑time delivery.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071