68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Quantum Computing in the Cloud: Innovation & R&D Strategies for Scalable Commercialization

The quantum computing in the cloud market across the U.S. and North America is expected to grow from $1.2B in 2025 to $7.9B by 2030, reflecting a CAGR of 45.1%. Fueled by expanding R&D investments, cloud-based quantum services are moving toward commercial scalability. By 2030, over 70% of enterprises using advanced analytics will integrate quantum cloud access for optimization, simulation, and cybersecurity applications. Strategic partnerships between hyperscalers (AWS, IBM, Google Cloud) and quantum hardware startups are accelerating innovation cycles, while federal funding and corporate consortia are driving the U.S. toward leadership in quantum infrastructure and commercialization.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.2B → $7.9B (CAGR 45.1%).

- 70% of enterprises to access quantum computing via cloud platforms by 2030.

- Quantum R&D investments in North America to exceed $5B by 2030.

- Cloud service providers to host 60% of quantum workloads globally.

- Hybrid quantum-classical integration to enhance computational efficiency by 35%.

- Commercialization ROI expected to grow 40% annually post-2027.

- Cybersecurity use cases to account for 28% of total quantum workloads.

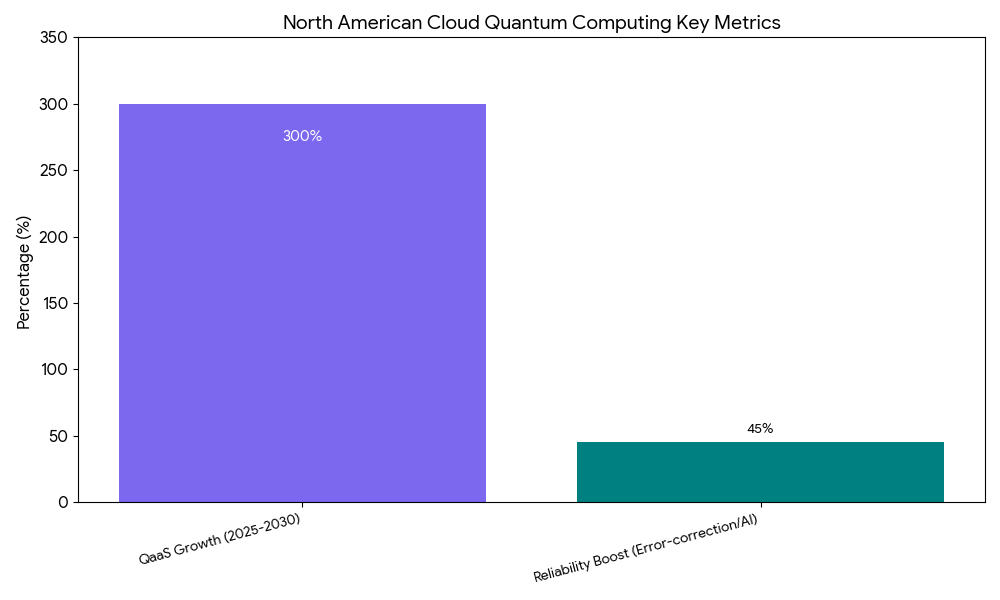

- Quantum-as-a-Service (QaaS) model adoption to rise by 300%.

- Error-correction algorithms to reduce failure rates by 45% by 2030.

- U.S. federal funding for quantum infrastructure to surpass $3.2B by 2030.

Key Metrics

Market Size & Share

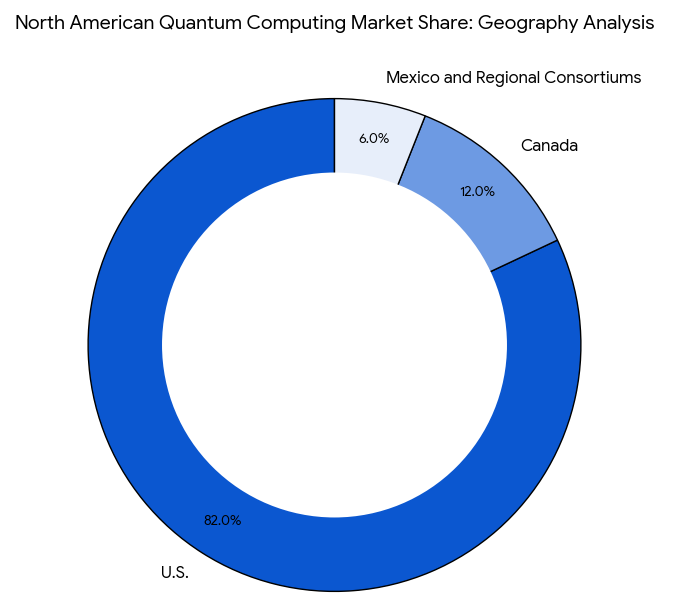

The U.S. and North American quantum cloud market is expected to expand from $1.2B in 2025 to $7.9B by 2030, marking a CAGR of 45.1%. The United States will dominate with 82% market share, driven by the presence of IBM Quantum, AWS Braket, Google Cloud Quantum AI, and Microsoft Azure Quantum. Canada will contribute 12%, fueled by national R&D programs supporting quantum hardware and cryptography startups. By 2030, Quantum-as-a-Service (QaaS) will represent the dominant delivery model, accounting for 65% of revenue streams, with enterprise clients adopting subscription-based pricing. Increased government investment in quantum infrastructure and federal defense initiatives will further position North America as the global hub for quantum commercialization.

Market Analysis

Cloud-based quantum computing is rapidly transitioning from research environments to commercial deployments in North America. Telecom, financial services, and healthcare enterprises are testing hybrid quantum models for simulation, optimization, and risk modeling. The integration of quantum hardware via the cloud allows enterprises to bypass capital-intensive infrastructure costs while benefiting from scalable access. From 2025 to 2030, QaaS offerings are projected to grow 300%, driven by partnerships between tech giants and quantum startups such as Rigetti, IonQ, and D-Wave. Meanwhile, error-correction improvements and AI-based calibration systems will boost reliability by 45%, bringing quantum workloads closer to real-world enterprise adoption.

Trends & Insights

- Quantum-as-a-Service (QaaS) to grow 300% by 2030, led by AWS, IBM, and Azure.

- Hybrid architectures enabling 35% faster processing for complex optimization problems.

- R&D funding boom: North America to exceed $5B in quantum innovation spending by 2030.

- Cybersecurity applications leading with 28% market share of quantum workloads.

- Quantum startups raising over $2.6B in venture funding between 2025–2028.

- AI-assisted error correction improving computational stability by 45%.

- Public–private partnerships expanding U.S. quantum testbeds in Texas, California, and Ontario.

- Cost optimization via cloud deployment to reduce entry barriers for mid-tier enterprises.

- Quantum developer ecosystems growing by 400%, led by open-source frameworks.

- Commercial ROI acceleration post-2027, reaching 40% annual growth as adoption scales.

These insights underline a clear shift from theoretical quantum research toward deployable commercial services, reinforcing North America’s global technology leadership.

Segment Analysis

The market divides into hardware integration (35%), software and algorithm design (25%), Quantum-as-a-Service (QaaS) platforms (25%), and consulting & ecosystem enablement (15%). Hardware integration leads with 35%, as cloud providers collaborate with quantum chipmakers to achieve scalability. Software design, making up 25%, focuses on quantum error correction, algorithm optimization, and development toolkits. QaaS platforms account for 25%, enabling flexible and subscription-based quantum access through AWS, IBM, and Azure. Finally, consulting & ecosystem services, at 15%, support enterprise integration, compliance, and training for quantum readiness, critical for large-scale adoption by 2030.

Geography Analysis

In North America, the U.S. dominates with 82% market share, led by key innovation centers in California, Massachusetts, and Texas, where federal and private R&D programs are expanding quantum capabilities. Canada, holding 12%, emphasizes quantum cryptography and academic R&D, backed by the Canadian Quantum Strategy (CQS) and companies like Xanadu and D-Wave. Mexico and regional consortiums account for the remaining 6%, focusing on data infrastructure collaboration. By 2030, cross-border integration of quantum resources will enable a North American quantum cloud network, advancing interoperability and shared research.

Competitive Landscape

Major players include IBM Quantum, AWS Braket, Google Cloud Quantum AI, Microsoft Azure Quantum, IonQ, Rigetti, and D-Wave Systems. IBM leads the sector with 400+ corporate clients using its Quantum Network, while AWS Braket offers multi-vendor cloud access for hybrid computation. Google continues to advance quantum supremacy benchmarks, focusing on scaling qubit counts beyond 1,000 by 2028. D-Wave and Rigetti specialize in quantum annealing and superconducting qubits, respectively, supporting enterprise-grade cloud integrations. Microsoft Azure Quantum provides a unified interface for quantum workloads across hardware partners, reinforcing its role in cloud–quantum convergence. The competitive focus is shifting toward error correction, pricing models, and enterprise-ready scalability.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071