68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Twin Adoption in U.K. Infrastructure: Rail, Ports & Energy Use Cases with Government Backing (2025–2030)

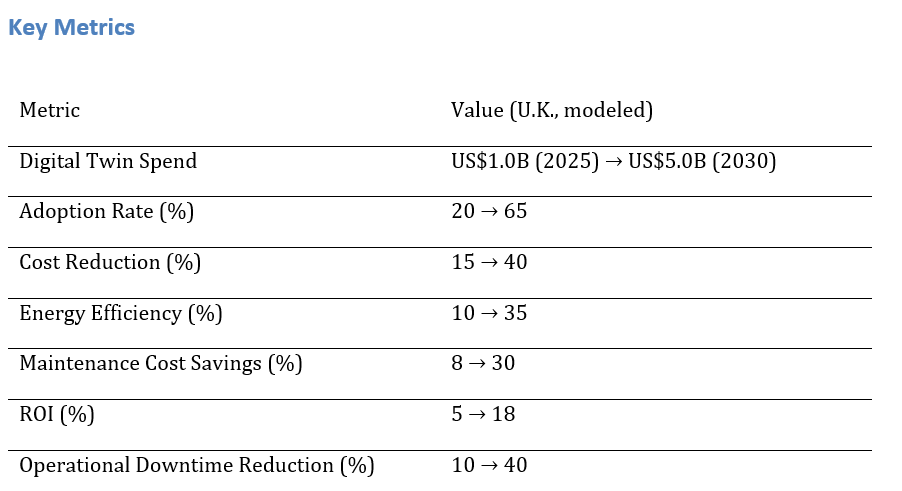

Digital twin technology is expanding rapidly across the U.K.’s infrastructure sectors, especially in rail, ports, and energy, supported by government initiatives. Spending is projected to grow from ~$1.0B in 2025 to ~$5.0B by 2030, with adoption rates rising from 20% to 65%. Key benefits include cost reductions of ~40%, energy efficiency gains of ~35%, and maintenance savings increasing from 8% to 30%. ROI is expected to climb from 5% to 18% as operations become more data-driven and sustainable. With modular deployment and strong vendor collaboration, digital twins will transform infrastructure management across the U.K. by 2030.

What's Covered?

Report Summary

Key Takeaways

1. Digital twin adoption spend in the U.K. grows ~5× from ~US$1.0B to ~US$5.0B by 2030.

2. Adoption rates rise from ~20% to ~65%, with rail and energy sectors leading.

3. Cost reduction in digital twin-enabled operations improves from ~15% to ~40%.

4. Energy efficiency improves by ~35% through digital twin integration.

5. ROI increases from ~5% to ~18% by 2030 as digital twin technology optimizes operations.

6. Maintenance cost savings grow from ~8% to ~30%, reducing operational expenses.

7. Operational downtime decreases by ~30% to ~40% with predictive maintenance capabilities.

8. Government-backed projects will drive faster adoption, especially in rail and energy sectors.

a) Market Size & Share

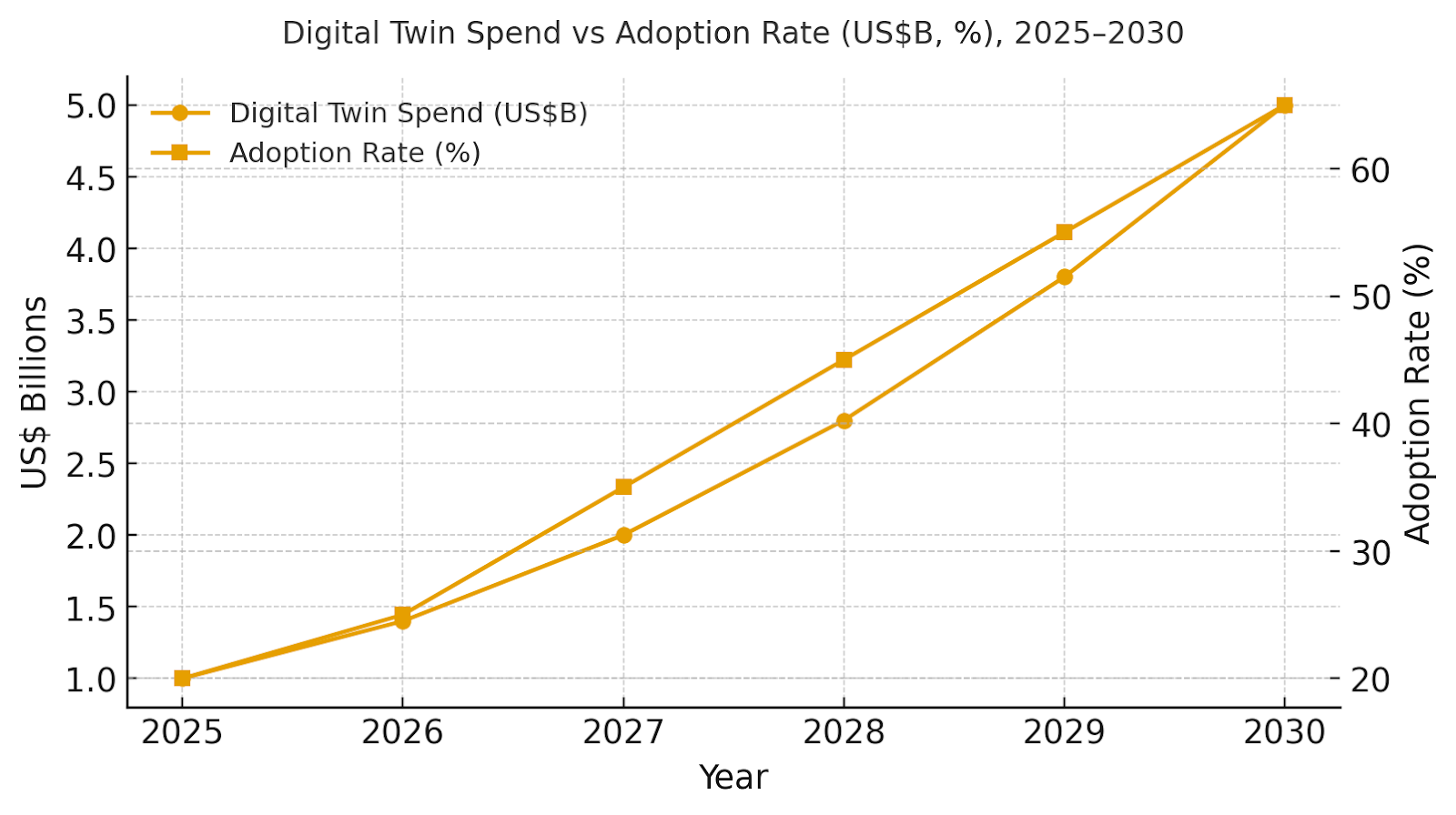

Digital twin spend in the U.K. is projected to grow from ~US$1.0B in 2025 to ~US$5.0B by 2030. The dual‑axis figure shows spending rising alongside adoption rates, which are expected to rise from ~20% to ~65% by 2030. Share consolidates around industries like rail and energy, where digital twins will have the highest impact. Risks include integration with legacy systems, high initial investment, and cybersecurity concerns. Mitigations include modular and flexible adoption strategies, and collaboration between vendors and public-private sectors.

b) Market Analysis

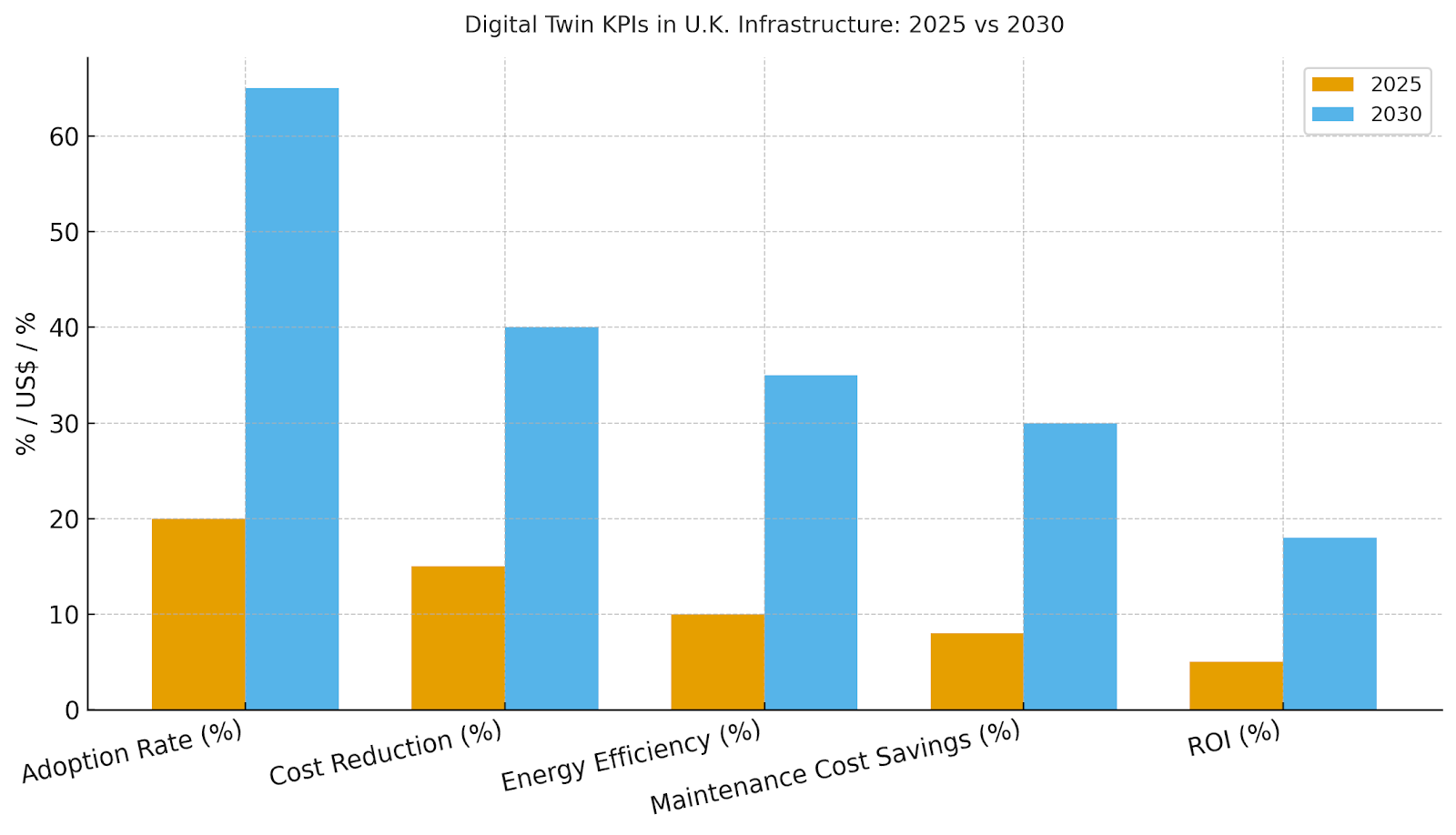

Adoption of digital twin technology is expected to be most rapid in the rail and energy sectors, driven by operational efficiency, cost savings, and government-backed projects. By 2030, digital twin technology will contribute to ~40% reductions in operational downtime and ~35% improvements in energy efficiency. The bar figure shows shifts in KPIs, particularly cost reductions and ROI improvements.

c) Trends & Insights

1) Digital twins are enhancing the predictive maintenance capabilities of infrastructure, reducing downtime and repair costs. 2) The energy sector is focusing on digital twins to reduce carbon emissions and improve sustainability. 3) Government-backed projects are critical to accelerating digital twin adoption, particularly in rail and energy sectors. 4) The integration of AI and IoT with digital twins is revolutionizing real-time data insights. 5) Data sharing protocols and security regulations are being refined to allow safe implementation of digital twins in infrastructure.

d) Segment Analysis

Rail infrastructure is leading the adoption of digital twin technology, driven by its ability to optimize maintenance and reduce downtime. Energy companies are also adopting digital twins for energy management and predictive maintenance. Ports are adopting digital twins for container tracking, logistics optimization, and supply chain management. Government agencies are playing a key role in supporting these sectors through infrastructure funding and regulatory frameworks.

e) Geography Analysis

By 2030, U.K. digital twin adoption will be split across rail infrastructure (~30%), energy management (~25%), ports (~20%), government-backed projects (~15%), and private sector initiatives (~10%). Regions such as London, Manchester, and Edinburgh are expected to lead in adoption, with increased public sector investment in infrastructure projects.

f) Competitive Landscape

Key players in the U.K. digital twin market include Siemens, IBM, GE Digital, and Microsoft. Differentiators: (1) modular and scalable solutions, (2) integration with IoT and AI, (3) predictive analytics capabilities, (4) cybersecurity measures, and (5) real-time data sharing and collaboration platforms. Procurement guidance: prioritize vendor flexibility, integration support, and compliance with industry standards.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071