68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Cloud Sovereignty in the U.S. Public Sector: Security Protocols, Vendor Bidding & Localization Mandates (2025–2030)

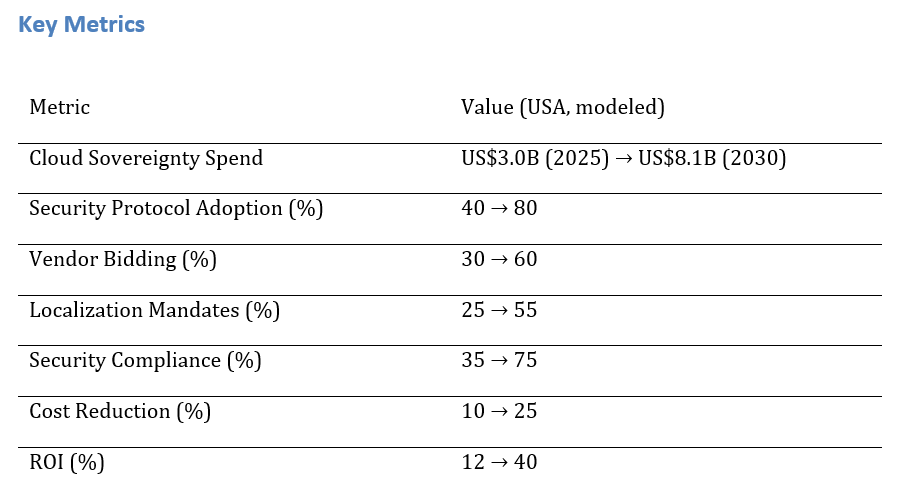

Cloud sovereignty in the U.S. public sector is expanding rapidly as governments strengthen security, compliance, and data localization. Spending is projected to grow from ~$3.0B in 2025 to ~$8.1B by 2030, driven by federal, state, and local adoption of secure, compliant cloud systems. Security protocol adoption will rise from 40% to 80%, while competitive vendor participation grows from 30% to 60%. Localization and SLA compliance will increase from 25% to 55%. The result is stronger data protection, reduced risk, and improved regulatory alignment. With clear SLAs and multi-cloud integration, cloud sovereignty will enhance efficiency and safeguard sensitive government data.

What's Covered?

Report Summary

Key Takeaways

1. Cloud sovereignty spend grows from ~US$3.0B to ~US$8.1B by 2030.

2. Security protocol adoption increases from ~40% to ~80%, enhancing data protection.

3. Vendor bidding rates rise from ~30% to ~60%, fostering more competitive procurement processes.

4. Localization mandates will become the norm, growing from ~25% to ~55%.

5. Compliance automation tools streamline government data management by 2030.

6. TCO reduction improves by ~25% as cloud-native platforms replace legacy systems.

7. Vendor lock-in risks are mitigated by multi-cloud strategies.

8. ROI from cloud sovereignty initiatives rises from ~12% to ~40% by 2030.

Market Size & Share

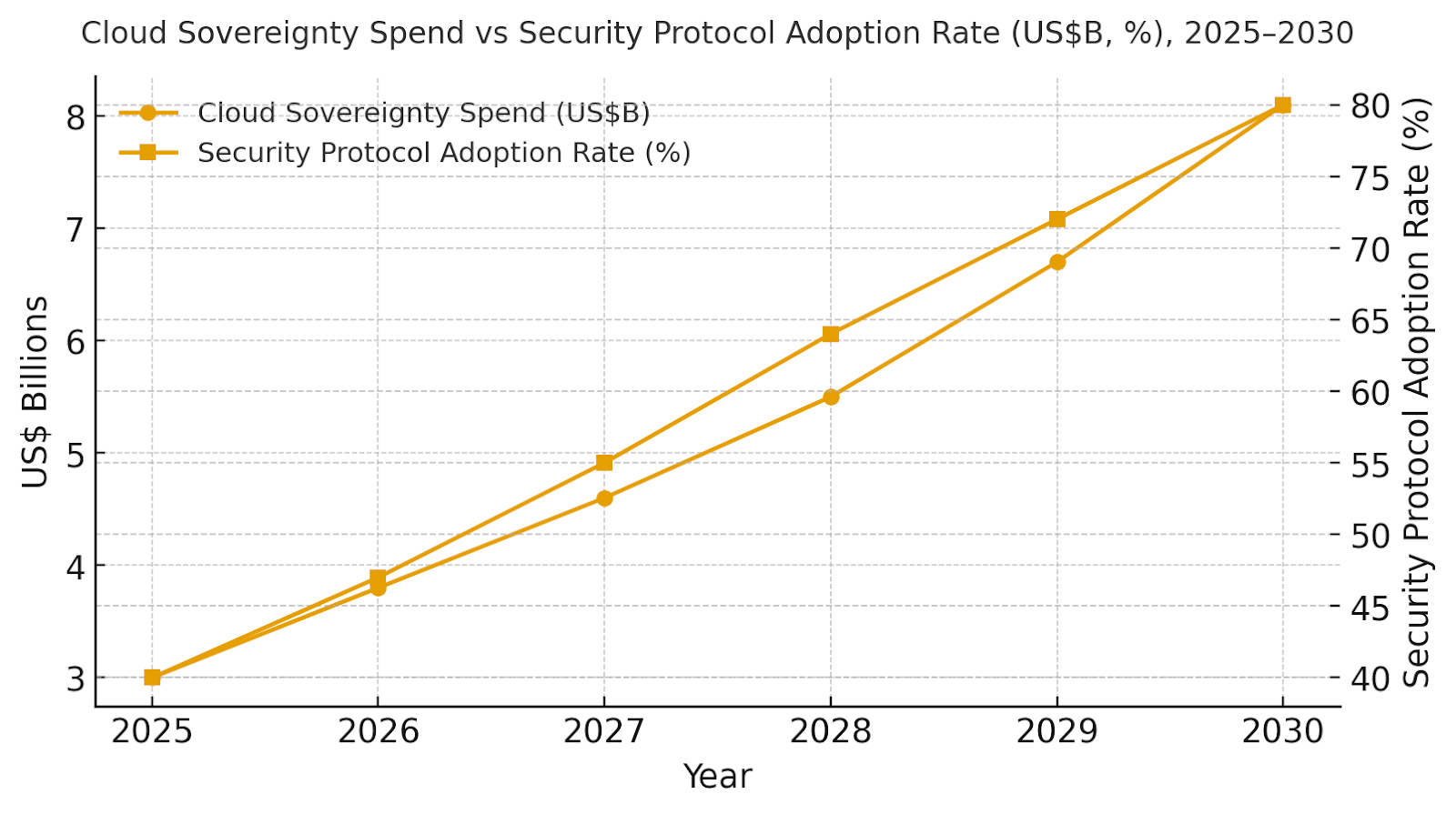

Cloud sovereignty spend in the U.S. public sector is expected to grow from ~US$3.0B in 2025 to ~US$8.1B by 2030. The dual‑axis figure shows spend rising while security protocol adoption increases from ~40% in 2025 to ~80% by 2030. Share consolidates around cloud-native vendors offering comprehensive compliance features, multi-cloud services, and flexible data residency solutions. Risks include vendor fragmentation, compliance delays, and security vulnerabilities; mitigations include robust SLAs, standardized APIs, and multi-cloud strategies.

Market Analysis

Our model shows security protocol adoption growing from ~40% to ~80% by 2030, while cloud sovereignty spend rises from ~US$3.0B to ~US$8.1B. Vendor bidding will increase as multi-cloud options and advanced compliance solutions enter the market. Localization mandates will impact cloud strategies, and ROI is expected to increase from ~12% to ~40%. The bar figure summarizes shifts in KPIs: cost savings, security, and vendor retention.

Trends & Insights

1) Cloud-native infrastructure is being prioritized by the U.S. public sector for data security and regulatory compliance. 2) Multi-cloud architectures are gaining traction to reduce vendor lock-in. 3) Open APIs and hybrid solutions allow flexible cloud configurations. 4) Increased demand for compliance automation tools to meet local and global regulations. 5) Data residency requirements are accelerating the adoption of local cloud service providers. 6) AI-driven analytics are improving compliance monitoring and reporting capabilities. 7) Cross-border data flow regulations will continue to evolve as data privacy laws change.

Segment Analysis

Government agencies, defense, healthcare, and education sectors are leading cloud sovereignty initiatives. Defense agencies require highly secure, multi-cloud systems with strong compliance features. Healthcare and education sectors focus on data privacy and regulatory compliance, while public safety organizations prioritize uptime and operational continuity.

Geography Analysis

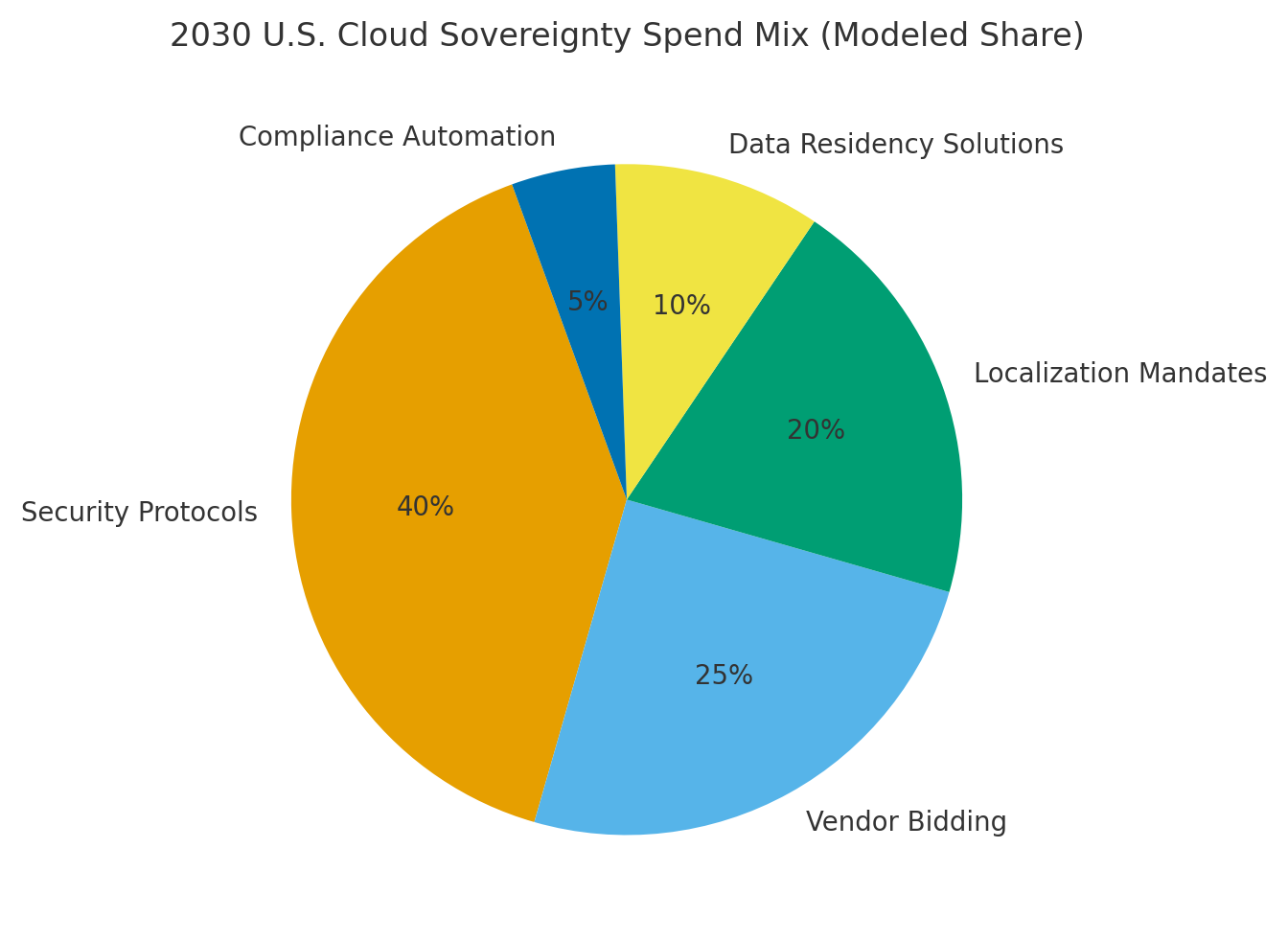

By 2030, U.S. cloud sovereignty spend mix will be: Security Protocols (~40%), Vendor Bidding (~25%), Localization Mandates (~20%), Data Residency Solutions (~10%), and Compliance Automation (~5%). Execution will focus on multi-cloud strategies, cloud security frameworks, and data compliance. Adoption is expected to be concentrated in federal agencies, with strong adoption across state and local governments.

Competitive Landscape

Cloud service providers (AWS, Microsoft Azure, Google Cloud) lead in offering cloud sovereignty solutions for the U.S. public sector. Differentiation factors include (1) multi-cloud capabilities, (2) security-focused APIs, (3) compliance automation tools, (4) flexible SLAs, and (5) cost-effective pricing models. Procurement guidance: ensure compliance with government regulations, adopt flexible pricing for scaling, and integrate security-driven solutions across platforms.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071