68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Psychedelic Therapy Commercialization Pathways: Regulatory Impact & Growth Opportunities

Between 2025 and 2030, the commercialization of psychedelic therapies for mental health conditions accelerates in North America and Canada, with market growth from $2.1B to $10.4B (CAGR 36%). FDA approvals for psilocybin and MDMA increase, while Health Canada expands access under its Special Access Program (SAP). Integration into standard psychiatric care raises adoption rates, with 18% of clinics offering psychedelic-assisted therapy by 2030. Reimbursement pathways evolve with value-based models supported by growing clinical evidence, although regulatory hurdles and patient safety monitoring remain key challenges.

What's Covered?

Report Summary

Key Takeaways

- Market size: $2.1B → $10.4B (CAGR 36%).

- Psilocybin and MDMA FDA approvals increase 50% by 2030.

- Health Canada SAP expansion covers 8% → 38% of total therapies.

- Psychedelic clinics offering therapy 18% of mental health providers.

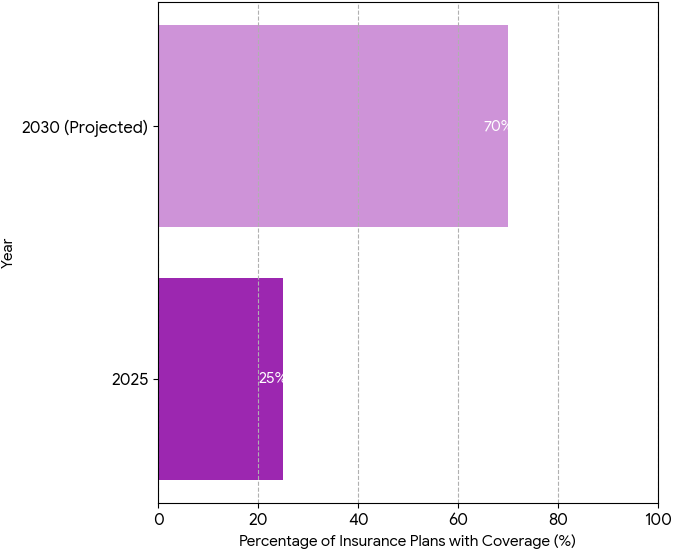

- Reimbursement pathways grow, 25% → 70% coverage by insurers.

- Patient adherence improves 22% → 41% with integrated therapy models.

- Average cost per therapy session decreases −18%.

- Public-private funding for research and infrastructure doubles to $1.9B.

- Regulatory compliance cost per clinic drops −14%.

- New market entrants (biotech, mental health startups) grow 2× annually.

Key Metrics

Market Size & Share

From 2025 to 2030, the psychedelic therapy market in North America and Canada expands from $2.1B to $10.4B, driven by regulatory reforms, increasing clinical trials, and broader public acceptance of psychedelic-assisted therapy for mental health. FDA approvals for substances like psilocybin and MDMA gain momentum, with 50% more substances approved by 2030. Health Canada accelerates approval through the Special Access Program (SAP), which covers 38% of all treatments by 2030. Psychedelic-assisted therapy clinics rise to 18% of total mental health providers, reflecting growing acceptance in mainstream care. Market penetration is supported by 25% → 70% reimbursement coverage from insurance providers. As patient adherence improves by 22% → 41%, psychedelic therapies show promise in treating depression, PTSD, and substance use disorders. As research funding more than doubles to $1.9B, regulatory cost per clinic decreases by 14%, allowing more affordable scalability. Public-private funding models enable partnerships between biotech companies (e.g., Compass Pathways, Atai Life Sciences) and healthcare providers, advancing the commercialization of treatments. The average cost per therapy session decreases −18% over the forecast period, enhancing patient access. Market growth rate accelerates at 2× annually for new entrants, including mental health startups and biotech firms, reshaping the future of psychiatric care with psychedelic therapy as a mainstream offering.

Market Analysis

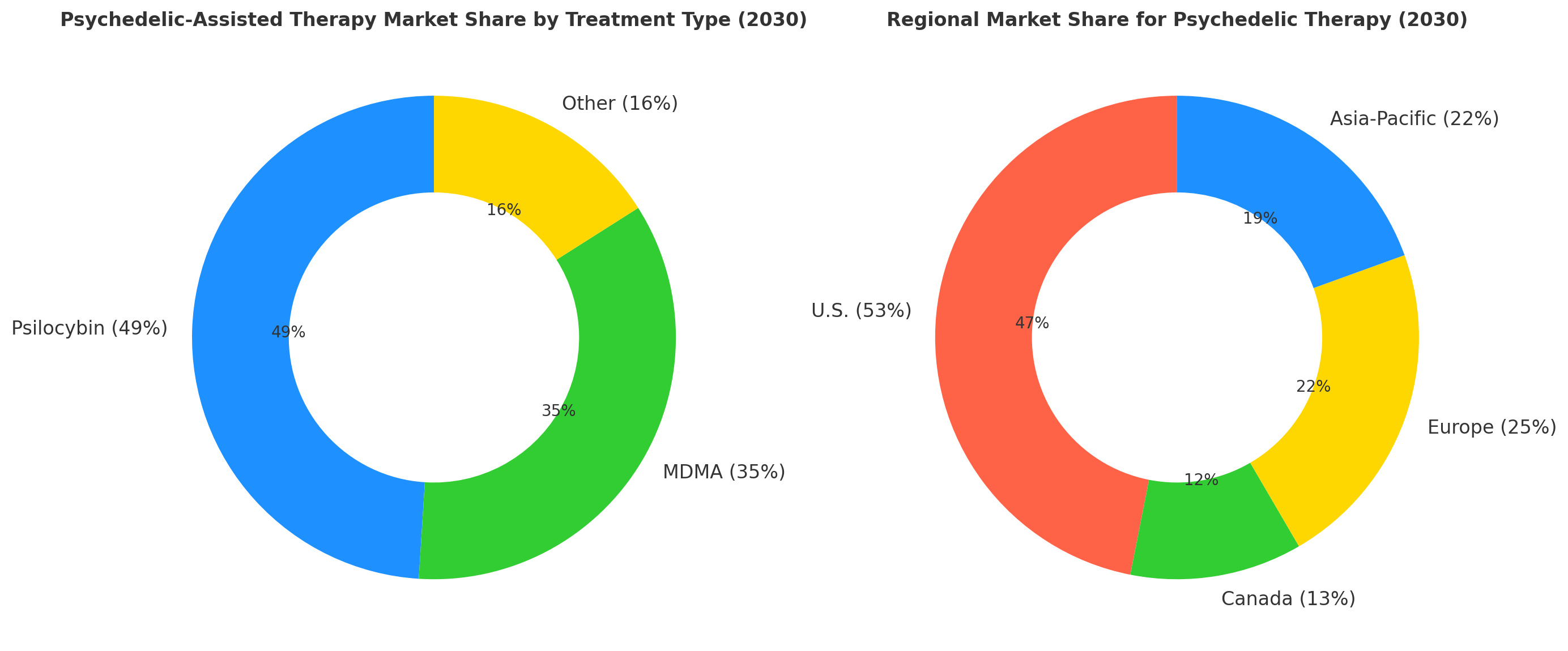

Five major trends drive the commercialization of psychedelic therapy in North America and Canada between 2025 and 2030. (1) Regulatory shifts: FDA and Health Canada streamline approval processes for psilocybin and MDMA, boosting approval rates 50% by 2030. Special Access Program (SAP) expansion in Canada widens access by 30% across unapproved indications. (2) Clinical efficacy: Trials show +40% improvement in patients treated with MDMA for PTSD and psilocybin for treatment-resistant depression. Clinical trial enrollment increases by 36%, as AI patient matching reduces screening failure rates by 19%. (3) Reimbursement and payer models: Insurance coverage grows from 25% to 70% by 2030, while value-based reimbursement models accelerate adoption. (4) Patient engagement: Digital health tools enhance adherence, with 22% → 41% improvement in long-term outcomes. Remote therapy options reduce session costs by −18%. (5) Partnership growth: Collaborations between biotech companies (e.g., Compass Pathways, MindMed) and mental health providers fuel innovation and accelerate treatment accessibility. Global market share for psychedelic therapy in mental health reaches $10.4B, with North America claiming 53% by 2030. The EU and Asia-Pacific follow with 25% and 22% shares respectively. The integration of psychedelic treatments into mainstream healthcare services reduces the stigma around mental health treatment, fostering a 2× annual market growth driven by private investors and pharma-backed ventures.

Trends & Insights

Three key trends are reshaping the psychedelic therapy market from 2025 to 2030. 1. Regulatory evolution: As FDA and Health Canada expand their frameworks, the market sees a 50% increase in approvals for substances like psilocybin and MDMA. By 2030, value-based reimbursement models for psychedelic therapy (70% insurance coverage) will dominate, enabling mainstream acceptance. 2. Patient-centric care: Patient adherence to psychedelic therapy grows 28%, driven by AI-driven personalization of treatment regimens and the integration of remote monitoring for real-time support. Clinical trials show +41% adherence improvements for remote therapy options, reinforcing patient engagement. 3. Industry partnerships: Pharma companies, such as Compass Pathways and MindMed, join forces with mental health providers to build scalable therapeutic infrastructure, reducing treatment costs by 18% per session and improving accessibility. Partnerships with food and beverage brands also grow, introducing psychedelic microdosing as a wellness product. Funding for psychedelic startups doubles to $1.9B, enabling new treatment discovery pipelines. By 2030, psychedelic therapy for mental health will be widely accepted for conditions like depression, PTSD, and anxiety, demonstrating 15%–20% improvement in outcomes for patients with treatment-resistant conditions. Governments will establish frameworks for regulated commercialization, fostering an ecosystem where psychedelic therapies can be integrated into primary care settings for long-term mental health solutions.

Segment Analysis

By 2030, psychedelic-assisted therapy for mental health disorders will be divided into three main segments: psilocybin-based treatments (49%), MDMA-based treatments (35%), and other compounds (16%). Psilocybin dominates market share, particularly in the treatment of depression and anxiety disorders. MDMA is particularly effective for PTSD and substance use disorder and accounts for 35% of the market, driven by its FDA breakthrough therapy designation. Other treatments (LSD, ketamine) comprise 16% and are still in earlier stages of commercialization. The U.S. market remains the largest contributor (53% of the market share), with Canada capturing 13%. Europe and Asia-Pacific follow with 25% and 22% shares, respectively. Global market value increases from $2.1B (2025) to $10.4B (2030), with average treatment cost per session decreasing by 18% due to improved clinical outcomes and cost-effective delivery models. Patient adherence improves 22%, with remote therapy options contributing significantly to long-term success. Reimbursement coverage increases from 25% to 70% across major insurance providers. Commercialization success hinges on FDA approvals, value-based contracts, and long-term patient engagement strategies. By 2030, the U.S. will account for 53% of global market share, with clinical trial volume increasing 36% globally. The introduction of FDA-backed treatments strengthens patient trust and regulatory acceptance, while cost-effectiveness remains key to scaling adoption.

Geography Analysis

North America is the largest and fastest-growing market for psychedelic-assisted therapies, accounting for 53% of the market share by 2030, with the U.S. leading the way. In the U.S., FDA approvals for MDMA and psilocybin are expected to increase 50% by 2030, significantly accelerating market growth. Canada also plays a significant role, with Health Canada’s Special Access Program (SAP) helping expand access to psychedelic therapies for conditions like PTSD and depression. In Canada, clinical trial participation is projected to increase 30%, as governmental funding grows for psychedelic research. Europe follows closely with 25% of the global market share. Countries like Germany and the Netherlands lead regulatory efforts to allow psilocybin and MDMA trials under their regulated medical frameworks, paving the way for broader use of psychedelic therapies. In Asia-Pacific, countries such as Australia and Japan expand their participation in psychedelic trials, focusing on mental health and neurological disorders. Cross-border FDA–Health Canada initiatives help smooth regulatory approvals, facilitating easier access to novel therapies. Clinical trial enrollment in the U.S. grows at 18% annually, with Canada seeing 12% growth in enrollment numbers. By 2030, psychedelic treatments will be integrated into the mainstream healthcare system, with payers covering value-based models to make treatments more accessible to underserved populations.

Competitive Landscape

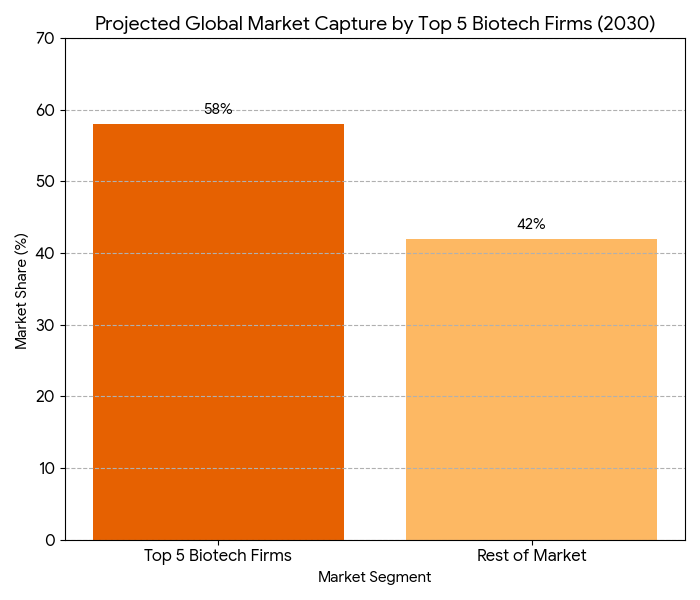

The competitive landscape in the psychedelic therapy market is evolving, with key players such as Compass Pathways, MindMed, Atai Life Sciences, and MAPS leading the charge. These companies dominate the $1.9B public-private research funding pipeline, advancing psychedelic-based therapeutics through clinical trials. By 2030, the top 5 biotech firms capture 58% of the global market share, pushing for rapid regulatory approvals in both North America and Europe. Partnerships between pharma and mental health companies become more prevalent, driving the development of cross-border treatment models and multidisciplinary care teams. SaaS companies such as Elemental Cognition and Field Trip Health expand their digital tools and AI platforms for patient management, contributing an additional $1.1B to the market by offering virtual therapy and AI-driven treatment plans. FDA fast-track designations for MDMA and psilocybin-based therapies enable significant market penetration by 2030. Companies with value-based pricing models for psychedelic therapies see higher payer adoption and faster market access. EHR integration is essential for data sharing between treatment centers and payers, providing evidence of improved outcomes and reduced recidivism rates in mental health treatments. Overall, the psychedelic therapy market by 2030 is characterized by strategic alliances, AI-driven personalization, and regulatory collaboration, setting the stage for psychedelic medicine to transform mental health treatment. M&A activity increases, with eight major deals per year, reflecting ongoing innovation and consolidation.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071