68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Personalized Nutrition Retail Models: DNA-Based Diet Curation & EU Novel Food Compliance

Personalized nutrition is shifting from wellness trend to retail operating model. Between 2025 and 2030, European brands fuse DNA and microbiome signals with pantry‑level recommendations, dynamic bundles, and compliant ingredient innovation. We model Europe’s personalized nutrition retail and testing spend growing from ~US$6.5B in 2025 to ~US$14.8B by 2030, with France emerging as a leading market thanks to pharmacy networks, grocery alliances, and strong food‑tech ecosystems. The strategy blends three engines: (1) diagnostics at‑home DNA/microbiome kits with consent‑first data capture; (2) curation SKU and recipe graphs that map genotypes, intolerances, and goals to cart‑ready plans; and (3) compliance ops ingredient provenance, EU novel food workflows, and labeling automation. Growth depends on trust, consent, and measurable outcomes. Programs must make value explicit: diet adherence tools, refill reminders, on‑label guidance, and clinician touchpoints. Commercially, the attach rate from test to paid program, plan→cart conversion, ARPU, and 12‑month retention define success.

What's Covered?

Report Summary

Key Takeaways

1. Consent‑first diagnostics power trust and long‑run retention.

2. SKU/recipe graphs translate genetics and goals into cart‑ready plans.

3. Compliance ops (claims, labeling, novel foods) are as strategic as marketing.

4. Attach rate, plan→cart CVR, ARPU, and 12‑mo retention are the CFO‑grade KPIs.

5. Evidence repositories and clinician review de-risk health claims.

6. Partnerships with pharmacies, grocers, and insurers accelerate adoption in France.

7. Local gastronomy and language variants raise adherence and repeat purchases.

8. Data minimization and clear opt‑outs close the trust gap in EU markets.

Key Metrics

Market Size & Share

Europe’s personalized nutrition retail and testing market is modeled to expand from ~US$6.5B in 2025 to ~US$14.8B in 2030. Growth vectors include mainstreaming of DNA/microbiome kits, app‑led diet curation, pharmacy integration, and compliant functional ingredients. France’s projected ~24% share reflects strong pharmacy and grocery ecosystems and a maturing food‑tech scene. The line figure shows the compounded trajectory to 2030.

Share dynamics across the stack: diagnostics monetization (kits, subscriptions), curation engines (AI recipe/plan generation), and compliant product innovations (novel foods, bio-actives) that pass EU scrutiny. Retailers that convert diagnostics into subscription‑plus baskets will gain share, especially when plans integrate household constraints, price sensitivity, and local cuisine. Execution risks include claims overreach, slow approvals for novel ingredients, and fragmented data consent. Winners adopt consent‑first design, maintain evidence repositories, and localize menus and guidance.

Market Analysis

Programs that align diagnostics, curation, and compliance shift KPIs materially. We model test→program attach rising from ~21% to ~38%, plan→cart CVR from ~4.6% to ~7.9%, ARPU from ~US$18 to ~US$27, and 12‑month retention from ~44% to ~58% by 2030, while the median novel food approval cycle compresses from ~14 to ~9 months with better dossiers and partnerships. Enablers: consent‑grade CDP, SKU/recipe graphs, in‑app adherence nudges, pharmacist/clinician touchpoints, and labeling/compliance automation. Barriers: privacy concerns, evidence gaps, and ingredient supply constraints.

Financial lens: attribute to incremental margin after kit costs, coaching, and ingredient premiums; account for returns/waste in perishables; and evaluate subscription churn versus basket‑only models. The bar figure summarizes directional KPI shifts under disciplined operations.

Trends & Insights

1) Consent‑centric personalization: explicit, layered opt‑ins and value exchanges lift trust. 2) Recipe graphs, not lists: constraints (genetics, goals, budget) mapped to meals and baskets. 3) Clinician‑adjacent models: pharmacist review and tele‑nutrition validate plans and claims. 4) Compliance by design: evidence repositories, label automation, and traceable ingredients. 5) Novel foods go mainstream: algae/precision‑fermented/bioactive components pass via strong dossiers and safety monitoring. 6) Adherence operations: nudges, streaks, and substitutions keep plans realistic. 7) Local gastronomy: French culinary variants increase delight and repeat purchases. 8) Interoperable records: portability and right‑to‑erasure without breaking adherence history. 9) Outcome reporting: weight/markers reported ethically with disclaimers. 10) Retail media adjacency: privacy‑safe segments monetize insights without compromising consent.

Segment Analysis

Weight & Metabolic Health: High attach and ARPU; require cautious claims and monitoring. Food Sensitivities & Allergies: Strict labeling, substitutions, and pharmacist review; strong retention when plans reduce symptoms. Sports & Performance: Higher basket value via protein and recovery products; data portability with wearables. Healthy Aging: Emphasis on convenience, safety, and clinician touchpoints. Family & Kids: Household‑aware plans and recipes; allergen handling and school meal compatibility. Across segments, define evidence thresholds, localize menus for French cuisine, and measure per‑segment attach rate, ARPU, retention, and approval timelines.

Geography Analysis

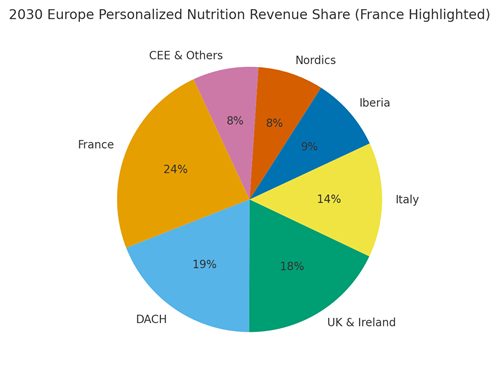

France is projected to contribute ~24% of EU personalized nutrition revenue by 2030, with DACH (~19%), UK & Ireland (~18%), Italy (~14%), Iberia (~9%), Nordics (~8%), and CEE & Others (~8%). France’s leadership is underpinned by pharmacy channels, culinary culture, and food‑tech partnerships. Localization principles: French language and culinary norms, pharmacist co‑sign for sensitive claims, and adherence UX aligned to local schedules. The pie figure illustrates the regional split.

Execution: centralize consent and evidence repositories; empower French pharmacy and grocer partners with toolkits; measure region‑specific attach, CVR, ARPU, retention, and approval cycle times; and iterate recipes and bundles to seasonal produce and prices.

Competitive Landscape

Incumbents blend diagnostics with retail distribution; challengers specialize in AI curation or compliant ingredient platforms. Differentiation vectors: (1) consent‑grade data and opt‑in UX, (2) evidence‑backed claims and label automation, (3) SKU/recipe graph quality, (4) pharmacist/clinician integration, (5) supply of compliant novel foods and bio-actives, and (6) outcome‑reporting credibility. Procurement guidance: demand open APIs, data minimization, right‑to‑erasure tooling, and audit trails for claims; validate ingredient provenance and regulatory pathways. Competitive KPIs: attach rate, plan→cart CVR, ARPU, 12‑month retention, and approval cycle times.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071