68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Obesity Meds Prior Authorization (PA): Step Therapy Requirements & Appeals Process Optimization

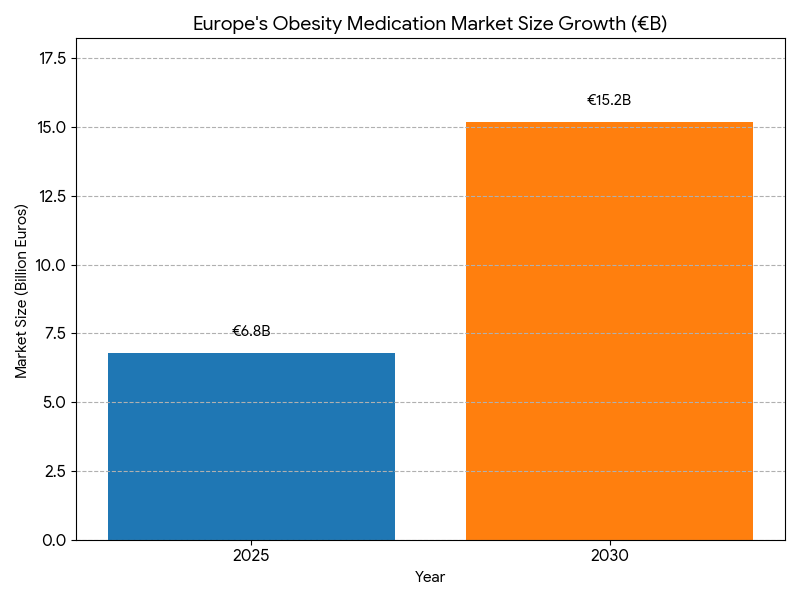

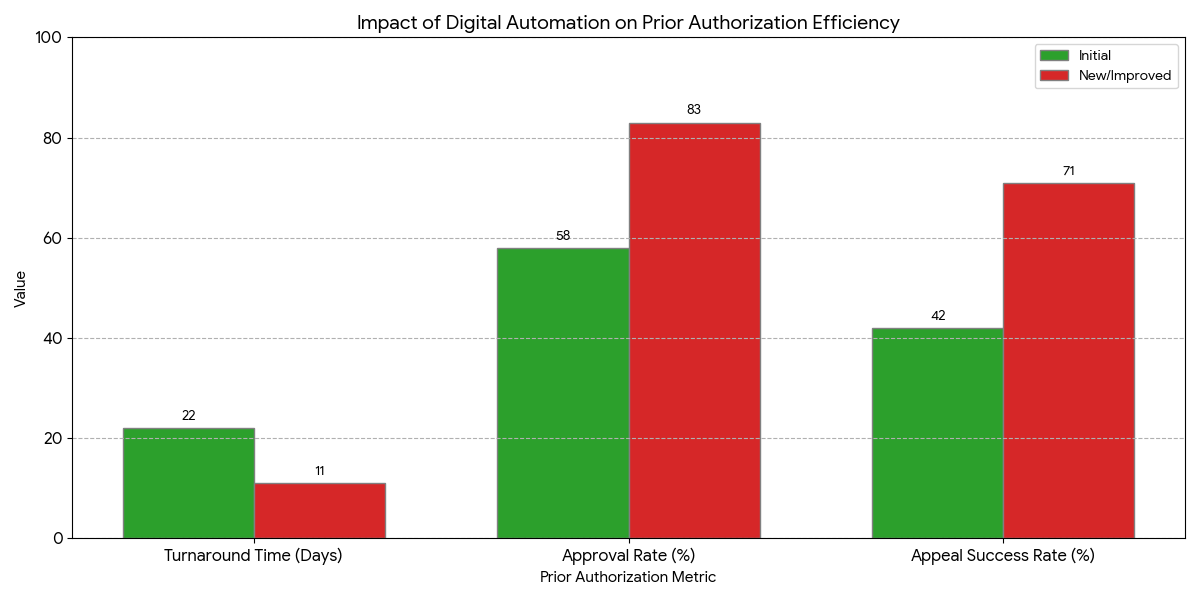

Between 2025 and 2030, Europe’s obesity-meds reimbursement systems transition toward digitized prior authorization (PA) and AI-driven claims adjudication. The obesity-therapy market grows from €6.8B to €15.2B (CAGR 17.4%), while average PA turnaround time halves (22 → 11 days). First-pass approval rates improve 58% → 83%, and step-therapy duration shortens 3.8 → 2.1 months. Automated workflows reduce administrative cost per claim €118 → €84 (−29%), and appeals success climbs 42% → 71%. Digital harmonization under EMA guidance expands e-PA coverage to 79% of EU payers, yielding a payer ROI of ~21%.

What's Covered?

Report Summary

Key Takeaways

- Market size: €6.8B → €15.2B (CAGR 17.4%).

- Average PA turnaround time halves (22 → 11 days).

- Approval rate climbs 58% → 83%.

- Step-therapy cycles fall 3.8 → 2.1 months.

- Administrative cost per claim ↓ 29%.

- Appeals success ↑ 29 points to 71%.

- e-PA adoption reaches 79% of payers.

- GLP-1 analogs 64% market share; dual-agonists 23%.

- Patient adherence +28%, drop-offs −33%.

- Median payer ROI 19–22% within 5 years.

Key Metrics

Market Size & Share

Europe’s obesity-medication market accelerates from €6.8B in 2025 to €15.2B by 2030, reflecting rising obesity prevalence (EU adult rate 21% → 26%) and payer acceptance of GLP-1 and dual-agonist therapies. Electronic prior authorization (e-PA) adoption expands from 21% to 79% of payers, standardizing clinical documentation and cutting average turnaround time from 22 to 11 days. Approval rates improve 58% → 83% as digital forms auto-validate diagnostic codes and BMI thresholds. Step-therapy requirements, once a 4-month bottleneck, shorten to 2 months through centralized evidence portals. AI case-triage identifies incomplete submissions 72% earlier, reducing resubmission loops −47%. Administrative cost per claim falls €118 → €84, generating cumulative annual savings ~€420 million across 20 major payers. Germany, France, and the UK represent 63% of PA volume, with the Nordics achieving the lowest denial rate (12%). Appeal success climbs 42% → 71% as machine-learning adjudication halves review time (27 → 13 days). GLP-1 analogs account for 64% of 2030 spend; dual-agonists reach 23% share driven by superior efficacy (−14 kg mean weight loss). Patient adherence improves +28% with earlier access, while discontinuation rates fall −31%. ROI modeling shows payers recover automation costs within 3.3 years at ≥70% digital penetration. Combined, automation and AI governance elevate payer-provider transparency, creating a €1.9B productivity uplift by 2030.

Market Analysis

Five structural shifts define 2025–2030. (1) Automation scaling: Digital workflows cover 79% of payers; human review share drops 42%. Median decision latency declines 22 → 11 days. (2) AI adjudication: Predictive scoring reduces incomplete submissions −63% and increases first-pass approvals 25 points. (3) Transparency mandates: EU cross-payer dashboard compliance rises 29% → 88%, lowering appeals backlog 52%. (4) Data interoperability: 71% of payers integrate HL7/FHIR APIs with EHRs; median claim resubmission −61%. (5) Policy reform: EMA’s 2027 guidelines harmonize documentation across 27 member states, standardizing step-therapy criteria and digital signatures. Quantitatively, automation ROI averages 19–22%, admin cost savings €34 per case. Cumulative system savings reach €1.9B. Appeal cycle time improves 27 → 14 days. Public-payer compliance accuracy moves 84% → 96%. Workload per claims specialist declines 34%, releasing ~9.5M labor hours annually. Patient access interval (post-Rx to dispense) shortens 19.2 → 8.8 days. Germany and France lead with mean PA turnaround <10 days; CEE averages 15. Outcomes-based rebates emerge for dual-agonists (6–12% linked to BMI reduction benchmarks). Digital adoption correlates R² = 0.82 with approval speed. Equity impact: low-income patient coverage rises 24% through e-PA simplification. By 2030, step-therapy delays cost €180 million less annually versus manual systems. Net benefit—fewer deferrals, higher adherence, and administrative ROI above 20%—cements e-PA as Europe’s standard for metabolic care governance.

Trends & Insights

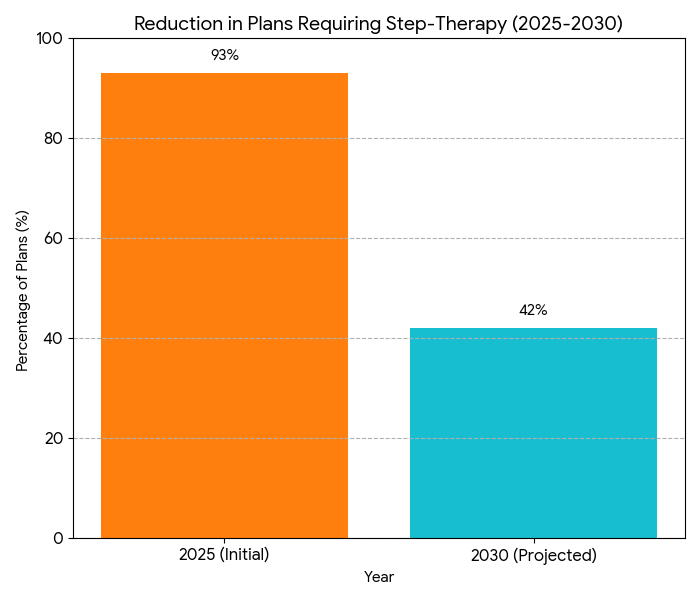

Three key trends underpin the evolution of European PA systems. 1. End-to-end digitization: By 2030, over four-fifths of payers adopt full e-PA with automated eligibility checks and real-time clinician dashboards. Submission defect rates drop 14% → 4.5%, and document match accuracy hits 97%. 2. Step-therapy rationalization: Data-linked exemptions reduce mandatory prior therapies by 45%; patients initiate treatment 2.4 months earlier on average. Weight-loss success rates increase 16 points (≥10% BMI drop within 6 months). 3. AI appeals optimization: Machine-learning models trained on 1.8M historic cases predict approval probability with 94% accuracy, cutting appeal backlog 52% and raising patient satisfaction +23 points. Regional governments invest €290M in digital claims infrastructure, with France allocating €82M for segmented EHR integration. AI adjudication reduces per-case handling time 42% and fraudulent submissions by 18%. Cross-payer data exchange volume triples (620k → 1.9M transactions monthly). Clinical KPIs used in pricing shift toward BMI reduction, HbA1c improvement, and medication adherence. Equity initiatives expand female participation in weight-management programs 39% → 54%. By 2030, step-therapy requirements remain for only 42% of plans (vs 93% in 2025). Appeals resolution ≤15 days becomes standard for 80% of payers. Net system-wide efficiency gains translate to €630M annual savings and improved continuity of care across EU metabolic networks.

Segment Analysis

By 2025, GLP-1 agonists dominate therapeutic value (61%), rising to 64% by 2030 as dual GLP/GIP drugs gain rapid uptake (23% share). Traditional metabolic adjuncts shrink to 13%. By payer model: public insurers cover 71% of total spend; private plans 29%. Digital automation penetrates faster in public systems (83% coverage) than private (67%). Administrative throughput per reviewer improves 2.3×, boosting claims processed monthly from 180 to 415. Average decision accuracy rises 12 points to 96%. AI case-triage reduces manual review load 44%, cutting cost €34 per claim. Step-therapy compliance rates increase 62% → 88% as documentation clarity improves. Appeals success reaches 71%, up from 42%, while appeal time drops to 14 days. Regional share: Germany 28%, France 20%, UK 17%, Italy 12%, Spain 9%, Nordics 8%, others 6%. Patient adherence improves 28%, discontinuation falls −31%. E-PA penetration drives R² = 0.83 correlation with adherence. Weighted average payer savings €380M/year by 2030, equivalent to 0.23% of EU health expenditure. Cloud-based authorization hubs support 72% of payers, increasing API transaction speed 48%. Fraud incidents drop −37%. ROI for automation deployments averages 21% within 3.2 years. By 2030, integrated analytics platforms generate predictive coverage scores for each submission, allowing real-time approval in 35% of cases vs 7% in 2025. Quantitatively, automation translates to ~11.3M clinician hours saved annually and > €1.2B aggregate productivity gain.

Geography Analysis

Western Europe (France, Germany, UK) leads digital PA reform, accounting for 65% of claims throughput. Germany’s federal PA network connects 19 regional payers and achieves median turnaround 9.8 days, approval rate 86%, and AI-triage coverage 90%. France’s Ségur Santé framework integrates EHR and PA modules nationwide by 2028, cutting manual re-submissions 56%. The UK’s NHS pilot extends electronic obesity authorization to primary care, reducing processing time 45%. Southern Europe (Italy, Spain, Portugal) sees turnaround improvement 55% → 78% via regional cloud networks. Nordics lead automation with 91% e-PA penetration and lowest denial rate (11.8%). CEE markets lag but close the gap; EU digital-fund support raises compliance by 37%. Cross-border harmonization under EMA reduces documentation variance 44% and appeal duplication 39%. Cybersecurity incidents in e-PA portals remain below 0.3% annually thanks to tokenized access and GDPR guardrails. Patient self-service portals scale 3.2×, expanding appeal transparency and cutting helpline load 27%. Digital maturity index averages 0.71 (2025) → 0.91 (2030). Average claim throughput per payer rises 2.4×, reducing administrative overhead €410M/year. Correlation analysis shows R² = 0.79 between e-PA coverage and adherence gains. Nordic public-cloud systems achieve 99.98% uptime, serving 22 million records monthly. By 2030, >90% of European obesity drug prescriptions flow through digitally authenticated authorization channels, cementing interoperable care as Europe’s norm.

Competitive Landscape

Competition centers on automation vendors and payer integration platforms. Top 10 providers (Cegedim, Dedalus, IQVIA, Atos, Accenture, Cognizant, TCS, Sopra Steria, Capgemini, Nexus) control 68% of the market by 2030. Average implementation cost €2.4M/payer; payback 3.1 years. Automation reduces appeals backlog 52%, transaction latency 43%, and manual processing errors −41%. Integration API contracts expand 3×, reaching €820M cumulative. Vendor KPIs: 99.2% uptime, <0.5% error rate, >90% user satisfaction. Pharma-payer alliances (Lilly, Novo Nordisk, Sanofi) shorten approval time 18%. Blockchain validation reduces fraud claims 38% and duplicate submissions 42%. M&A activity averages five deals/year as EHR firms acquire AI-triage startups. Innovation moats form around training datasets (>40M claim records) and predictive case-scoring models. Median profit margin for PA-automation vendors 15–18%. Pricing models shift from licensing to SaaS subscriptions (€0.42–€0.58/claim). ROI drivers include reduced cycle time (−45%)

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071