68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

North America Precipitated Calcium Carbonate Market (2025–2030): From ~USD 2.34 Billion in 2024 to ~USD 3.02 Billion by 2030 & CAGR (~4.3%) | Paper Manufacturing, Plastics, Paints & Coatings, Adhesives & Sealants

The North America precipitated calcium carbonate (PCC) market is set to expand from USD 2.34 billion in 2024 to USD 3.02 billion by 2030, reflecting a CAGR of 4.3%. PCC is widely used across key industries such as paper manufacturing, plastics, paints & coatings, and adhesives & sealants. The market is being driven by the increasing demand for high-performance PCC in applications requiring bright white pigments, improved mechanical properties, and sustainability. The growth of the paper and packaging industry in North America, especially in sustainable packaging solutions, is a key factor contributing to the demand. Additionally, the growing adoption of PCC in plastics for its cost-efficiency and reinforcing properties is supporting market growth. Environmental regulations are also encouraging the use of bio-based and sustainable fillers in various industrial applications, which will further propel the market over the forecast period.

What's Covered?

Report Summary

Key Takeaways

- Market to grow from USD 2.34B (2024) to USD 3.02B (2030) at 4.3% CAGR.

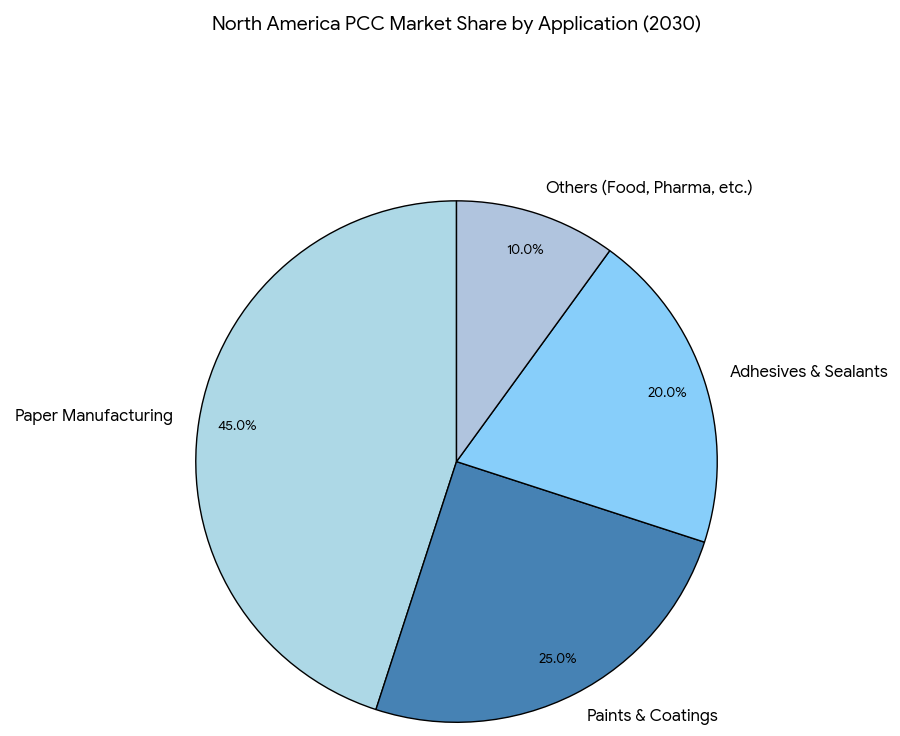

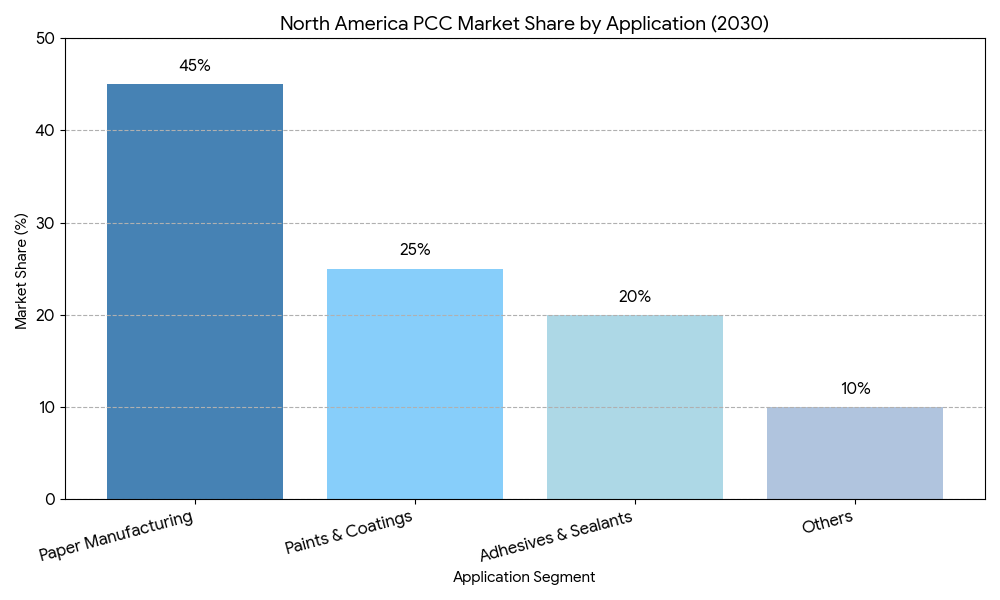

- Paper manufacturing will remain the dominant segment, accounting for 45% of total demand.

- Plastics sector to grow at 5.2% CAGR, driven by reinforcing and cost-effective properties.

- Paints & coatings applications will contribute 25% of market share by 2030.

- Adhesives & sealants to grow at 6% CAGR, driven by high-strength formulations.

- Sustainable packaging trends will fuel demand for high-performance PCC in the paper industry.

- North America will continue to dominate with a 60% market share.

- Environmental regulations will promote the use of eco-friendly, bio-based PCC in industrial applications.

- Bright white pigment demand is pushing PCC consumption in paper and plastics.

- Increasing demand for lightweight materials will drive PCC adoption in plastics and adhesives.

Key Metrics

Market Size & Share

The North America precipitated calcium carbonate (PCC) market is projected to grow from USD 2.34 billion in 2024 to USD 3.02 billion by 2030, driven by increasing demand in paper manufacturing, plastics, paints and coatings, and adhesives & sealants. The paper manufacturing sector will continue to dominate, contributing 45% of total market demand by 2030. Plastics will see the highest growth at 5.2% CAGR, driven by the need for reinforcement and cost-effective solutions. Paints & coatings and adhesives sectors will contribute 25% and 20% of the market, respectively. Sustainable packaging trends are expected to further fuel demand for PCC in paper products, while bio-based PCC will make up 12% of the market by 2030.

Market Analysis

The precipitated calcium carbonate market in North America is driven by its widespread use in paper manufacturing, where it serves as a cost-effective filler and bright white pigment. The plastics industry is seeing growing adoption of PCC due to its ability to reinforce polymers while keeping costs low. PCC is also a critical ingredient in paints and coatings, enhancing color consistency and coverage. The adhesives and sealants market is increasing due to the use of PCC in creating high-strength formulations for automotive, construction, and electrical applications. The growing demand for sustainable and eco-friendly products is pushing the market toward bio-based PCC, as regulatory requirements and green certifications become more stringent.

Trends & Insights

- Sustainable Packaging: Increasing demand for eco-friendly packaging solutions will boost PCC usage in the paper industry.

- Bio-Based Solutions: Growing interest in bio-based PCC products as environmental regulations push for sustainable production practices.

- Plastics Reinforcement: The plastics industry is adopting PCC to create stronger, lighter materials, particularly in the automotive and construction sectors.

- Cost-Efficiency: PCC remains an essential cost-effective alternative to other fillers, especially in paints and coatings.

- Regulatory Influence: Green regulations for sustainability and safe materials will continue to encourage PCC adoption in consumer goods.

- Packaging Innovation: The rise of biodegradable and recyclable packaging in food and beverages will drive demand for PCC in the paper sector.

- Lightweight Materials: Increasing demand for lightweight materials in automotive and electronic goods is propelling PCC in plastics.

- Technological Improvements: Advances in PCC production technology will improve product quality and efficiency while lowering costs.

- Health and Safety Standards: Increasing focus on safe chemicals will push for high-quality, non-toxic PCC in consumer products.

- E-Commerce Impact: The growth of online retail will expand PCC consumption in the packaging and cosmetic sectors.

Segment Analysis

The market is segmented by product type and application. The paper manufacturing segment remains the largest, with 45% of total demand. Plastics will see the fastest growth at 5.2% CAGR, particularly for use in lightweight automotive parts and reinforced polymers. Paints and coatings will contribute 25% of the total market by 2030, driven by demand for durability and color quality in automotive and construction coatings. Adhesives and sealants will account for 20% of demand, with increasing use in building materials and electronics. The bio-based segment will increase to 12% of total market share by 2030, driven by consumer demand for sustainability.

Geography Analysis

North America will continue to lead the global PCC market, accounting for 60% of demand, driven by its strong presence in automotive, construction, and consumer goods industries. Europe will follow, with growing demand from eco-friendly packaging and paint and coatings applications. The Asia-Pacific market, especially China and India, will experience significant growth at 7% CAGR, fueled by the rise in industrial applications and green building initiatives. The Middle East and Latin America are emerging markets for PCC in construction and packaging, while Africa will experience steady growth in pharmaceutical applications.

Competitive Landscape

The North American PCC market is highly competitive, with major players such as Omya, Imerys, SABIC, Huber Engineered Materials, and Minerals Technologies Inc.. Omya and Imerys dominate the market, providing high-quality PCC for paper and plastics applications. SABIC and Huber are leading players in the bio-based PCC segment, focusing on sustainability and environmental compliance. Smaller regional players are focusing on local supply chains to reduce logistics costs, while global companies continue to drive innovation in high-performance PCC for adhesives, sealants, and automotive parts.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071