68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Luxury Retail Digitalization: Competitive Landscape, Consumer Insights & Pricing Strategies in Post-Pandemic Europe

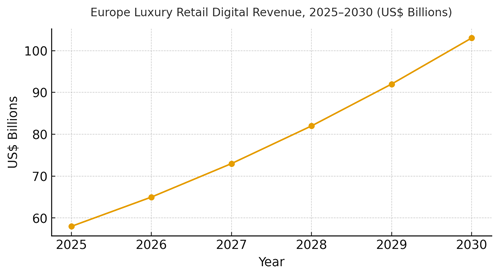

Post‑pandemic Europe has cemented digital as a primary client touchpoint for luxury yet growth now depends on quality, not just channels. From 2025 to 2030, leaders will combine four engines: (1) omnichannel excellence appointments, reserve‑online‑pickup‑in‑boutique (ROPB), same‑day courier; (2) clienteling intelligence advisor‑led outreach with data‑driven chapters; (3) experiential content atelier livestreams, AR try‑ons, provenance storytelling; and (4) pricing science transparent value ladders, dynamic markdown governance, and localized price harmonization. We model Europe’s luxury digital revenue rising from ~US$58B in 2025 to ~US$103B by 2030, with France a top contributor given maison density and boutique networks. Operationally, digitalization is less about adding tools and more about orchestrating journeys. Client data fabrics integrate ecommerce, boutique POS, appointments, and service history to power next‑best actions; content pipelines deliver localized assets at boutique cadence; and pricing algorithms work within strict guardrails to safeguard brand equity.

What's Covered?

Report Summary

Key Takeaways

1. Orchestrated journeys beat tool silos connect POS, ecommerce, appointments, and service data.

2. Clienteling at scale lifts retention and AOV; advisors need content, context, and cadence.

3. Experiential content (atelier, AR) improves conversion without resorting to markdowns.

4. Governed pricing science: harmonize cross‑border prices and cap markdown exposure.

5. First‑party data programs offset cookie loss; value exchanges drive opt‑ins.

6. Return reduction comes from fit aids, better PDP assets, and post‑purchase support.

7. France remains a flagship engine for experiential retail and clienteling depth.

8. CFO‑grade dashboards: omnichannel %, CVR, return %, clienteling reach, markdown exposure.

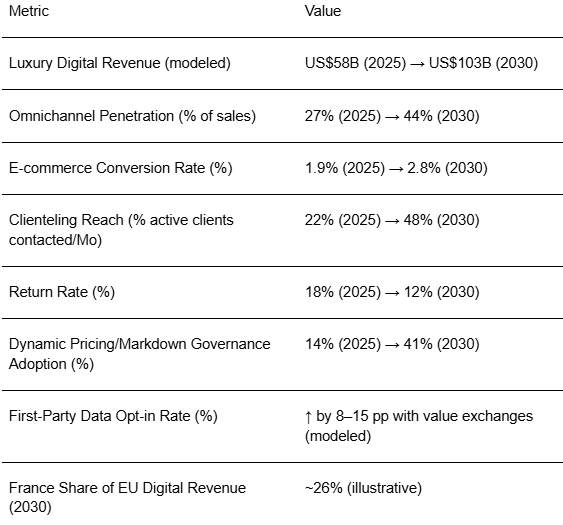

Key Metrics

Market Size & Share

Europe’s luxury digital revenue is modeled to expand from ~US$58B in 2025 to ~US$103B in 2030 as omnichannel experiences normalize and boutique networks embrace service‑led digital tools. France contributes an estimated ~26% share by 2030, propelled by maison density and destination boutiques. The line figure visualizes the compounded growth trajectory. Within categories, leather goods, watches/jewelry, and beauty dominate digital value; RTW scales with fit/return solutions and localized content. Services repairs, personalization, appointments become revenue‑adjacent signals that drive conversion and retention.

Share dynamics: brands with mature clienteling and content pipelines gain share as algorithms and advisors coordinate next‑best actions. Price harmonization and controlled markdown windows reduce cross‑border arbitrage and preserve equity, while certified resale provides circular on‑ramps. Execution risks: siloed data fabrics, under‑resourced boutiques, and inconsistent PDP assets. Mitigations: unified schemas, boutique enablement toolkits, and content SLAs synchronized with retail calendars. Measurement must include omnichannel %, CVR, returns, clienteling reach, and markdown exposure to validate value creation across markets.

Market Analysis

Digitalization shifts core KPIs when run as an operating system rather than a set of pilots. We model omnichannel penetration rising from ~27% to ~44%; e‑commerce CVR improving from ~1.9% to ~2.8% through better PDP assets, AR try‑ons, and provenance content; clienteling reach expanding from ~22% to ~48% with advisor tooling and content kits; return rates moderating from ~18% to ~12% via fit aids and post‑purchase service; and dynamic pricing/markdown governance adoption climbing from ~14% to ~41% under strict guardrails. The bar chart summarizes these shifts. Enablers: CDP‑backed client data fabrics, advisor‑friendly clienteling CRM, DAM‑driven content ops, and pricing platforms that harmonize and limit markdown exposure. Barriers: boutique capacity, data quality, and cross‑border arbitrage pressures.

Financial lens: attribute uplift to contribution margin after returns and markdowns. Use cohort holdouts for clienteling and content formats; monitor markdown exposure and price elasticity; and align incentives across ecommerce and boutiques to prevent channel conflict. Vendor strategy: select modular components with clean APIs to avoid lock‑in and enable local innovation in France and other EU markets.

Trends & Insights

1) Clienteling as growth OS: advisors orchestrate journeys across channels with data‑informed chapters. 2) Provenance‑forward PDPs: origin, craft, and repair options elevate perceived value and reduce returns. 3) AR try‑ons and fit tech: conversion up, returns down in RTW/footwear/beauty. 4) Experiential commerce: atelier/live formats and appointments carry more weight than performance ads. 5) Price harmonization windows: reduce arbitrage while respecting local VAT/rules. 6) Circular programs: certified resale and repair subscriptions as loyalty levers. 7) First‑party data exchanges: value‑for‑data propositions replace cookies. 8) Accessibility and localization: captions, language variants, and boutique‑grade assets. 9) Fraud & counterfeit resilience: serialization, track‑and‑trace, and marketplace enforcement. 10) Measurement discipline: omnichannel %, CVR, returns, clienteling reach, markdown exposure.

Segment Analysis

Leather Goods: Clienteling depth and personalization drive AOV; provenance reduces counterfeit risk. Watches & Jewelry: Appointment‑led journeys, boutique pick‑up, and authenticated resale. Beauty: Sampling, AR shade finders, and subscription care; low return friction with strong PDPs. RTW & Footwear: Fit tech, size exchanges, and limited capsules to limit markdown dependence. Home/Design: Appointment installs and storytelling around materials. Across segments, set guardrails on dynamic pricing and markdowns; track per‑segment CVR, return %, clienteling reach, and markdown exposure; and enable boutiques with content kits and appointment capacity.

Geography Analysis

France commands ~26% of Europe’s luxury digital revenue by 2030, followed by DACH (~19%), UK & Ireland (~17%), Italy (~18%), Iberia (~7%), Nordics (~6%), and CEE & Others (~7%). Paris remains a flagship hub, while regional French boutiques deepen loyalty through appointments, repairs, and events. DACH benefits from logistics efficiency and data discipline; Italy from atelier‑driven storytelling; the UK from media and marketplace sophistication. The pie figure highlights France’s role within the European mix.

Execution: centralized client data and content provenance; localize experiences and price harmonization to city‑level realities; equip boutiques with appointment capacity and repair partnerships. Track geography‑specific KPIs and reinvest where omni + clienteling outperforms markdown‑led tactics.

Competitive Landscape

Incumbent maisons leverage boutique networks, heritage, and clienteling systems; challengers win on digital craft, speed, and modular stacks. Competitive vectors: (1) client data fabrics (CDP + POS + ecommerce), (2) clienteling CRM with advisor UX, (3) DAM‑led content operations, (4) pricing governance and harmonization, (5) circular programs (repair/resale), and (6) anti‑counterfeit serialization. Procurement guidance: prioritize open APIs, boutique enablement, and ROI tied to omnichannel %, CVR, return %, and markdown exposure. Winners in 2025–2030 will preserve brand aura while scaling service‑led digital growth across Europe, with France as the experiential flagship.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071