68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Hyperlocal Organic Food Networks: Supply Chain Optimization & Tier-III Market Penetration

India’s demand for organic and residue‑free fresh produce is accelerating, pushed by health consciousness, rising disposable incomes in non‑metro regions, and trust built through traceability and community‑supported models. Hyperlocal organic networks short‑haul supply chains connecting certified farm clusters to dark stores and micro‑fulfillment pick‑points are emerging to serve daily/weekly baskets in 10–24 hour harvest‑to‑home cycles. We model India’s hyperlocal organic GMV rising from ~US$1.6B in 2025 to ~US$4.4B by 2030, with Tier‑III towns contributing a growing share as logistics density and cold‑chain access improve. Operationally, the winning formula blends agronomy discipline with logistics science. Farm‑gate pre‑cooling and pack‑house standardization reduce spoilage; dynamic demand‑sensing and harvest planning minimize gluts and stock‑outs; and zoned dark‑store networks enable late‑cutoff, early‑morning delivery. Cold‑chain orchestration (milk runs, insulated totes, reefer hubs), SKU rationalization (seasonal curation), and compliance automation (organic cert renewals, residue tests, geotagged plots) are core levers.

What's Covered?

Report Summary

Key Takeaways

1. Short‑haul, harvest‑aligned logistics cut spoilage and improve freshness economics.

2. Dark‑store zoning and late‑cutoff micro‑fulfillment raise on‑time delivery to >90%.

3. Embedded fintech compresses farmer payout cycles and stabilizes offtake.

4. Traceability + compliance automation builds trust and supports modest premiums.

5. SKU curation and private‑label staples protect margin while keeping baskets affordable.

6. Subscription micro‑baskets smooth demand and streamline routing.

7. Tier‑III penetration requires trust infrastructure and cost‑efficient cold‑chain nodes.

8. Measure contribution margin after cold‑chain and reattempts not just GMV.

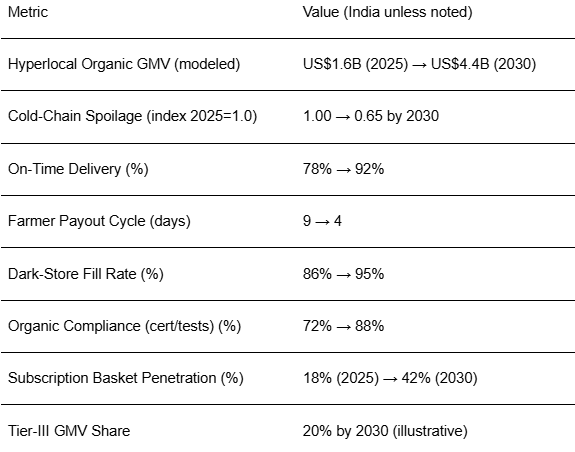

Key Metrics

Market Size & Share

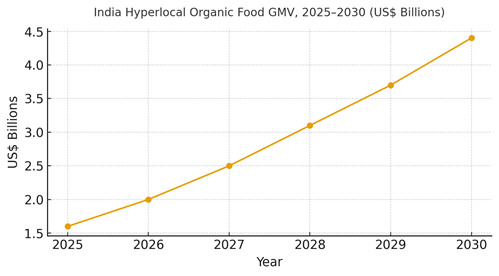

India’s hyperlocal organic GMV is modeled to grow from ~US$1.6B in 2025 to ~US$4.4B by 2030 as consumers shift toward residue‑free produce and reliable fresh chains. Share evolves from metro‑centric to broader coverage as Tier‑II/III density and trust infrastructure improve. Premiums over conventional produce narrow slightly as scale reduces costs and private‑labels expand. The line figure depicts the growth trajectory.

Share dynamics: metros (Tier‑I) retain the largest absolute GMV but lose share to Tier‑II/III as logistics nodes and certification ecosystems mature. Supply‑side share tilts toward farm‑cluster cooperatives and contract farming with predictable offtake. Networks with strong cold‑chain orchestration, traceability, and embedded fintech for farmer payouts capture outsized share, while marketplaces relying on ad‑hoc sourcing lag in freshness and compliance.

Execution: build regional farm clusters within 100–200 km of urban demand; standardize pre‑cooling and pack‑house operations; deploy demand‑sensing to align harvest plans; and anchor dark‑stores in neighborhoods that support first‑wave (early morning) delivery. Measure contribution margin after cold‑chain costs and re‑attempts, not just GMV.

Market Analysis

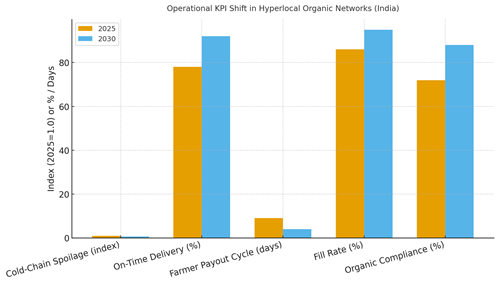

Operational KPIs trend favorably with disciplined process design. We project cold‑chain spoilage index improving from 1.00 to ~0.65 by 2030 as farm‑gate pre‑cooling and insulated tote logistics scale; on‑time delivery from ~78% to ~92% as dark‑store zoning and late‑cutoff routes mature; farmer payout cycles from ~9 to ~4 days using embedded fintech and predictable offtake; dark‑store fill rate from ~86% to ~95% via demand‑sensing and SKU curation; and organic compliance from ~72% to ~88% through automated renewals and residue testing. Risks include cold‑chain energy costs, certification backlogs, and rural road constraints; mitigations involve solar‑assisted pre‑cooling, digital audit trails, and route planning with weather and road quality overlays.

Financial lens: protect margin through private‑label staples, multi‑SKU bundles, and subscription micro‑baskets that stabilize demand and raise route density. Use price ladders (certified organic, residue‑free, natural) with transparent standards. The bar chart summarizes the plausible KPI shift by 2030. Governance priorities: temperature telemetry, recall readiness, fair grading, and clear communication on standards to prevent greenwashing.

Trends & Insights

1) Trust infrastructure at the core: certification, residue tests, and transparent grading are table stakes. 2) Harvest‑aligned logistics: milk runs and late‑cutoff scheduling enable dawn delivery without freshness loss. 3) Embedded fintech: faster payouts stabilize supply and support farmer inputs. 4) Micro‑subscriptions: weekly baskets smooth demand, reduce spoilage, and support planning. 5) Private‑label staples: predictable quality and margin buffers. 6) Cold‑chain sustainability: solar pre‑cooling, efficient reefer utilization, and energy audits. 7) Traceability UX: scannable lot IDs, farm stories, and temperature breadcrumbs build loyalty. 8) Tier‑III playbook: partner with local cooperatives, phase compliance, and pilot hub‑and‑spoke cold nodes. 9) Category curation: fewer, better SKUs with seasonal rotations outperform expansive catalogs. 10) Community engagement: sampling at RWAs and schools drives trial and trust beyond metros.

Segment Analysis

Fresh Produce: Highest spoilage risk and quality sensitivity; invest in pre‑cooling, grading, and insulated last mile. Dairy & Eggs: Cold‑chain integrity, short shelf life, and predictable repeat demand; subscription suitability is high. Packaged Organic Staples: Lower perishability; private‑labels and bundles anchor margin. Ready‑to‑Cook/Meal Kits: Transparent sourcing and short processing times; demand forecasting crucial. Baby & Health‑Focused SKUs: Premium proof points and stringent compliance; limited assortment with high trust signals. Across segments, define tiered promises (freshness window, return policy, traceability depth) and align service levels with contribution margin. Track per‑segment KPIs: spoilage %, on‑time %, re‑attempts, and subscription retention.

Geography Analysis

By 2030, GMV share is expected at ~46% Tier‑I metros, ~34% Tier‑II, and ~20% Tier‑III. Tier‑III momentum stems from rising incomes, smartphone adoption, and improved cold‑chain nodes. Regional nuance: South and West scale faster given cooperative density and agri‑infrastructure; North grows via peri‑urban clusters; East requires targeted cold‑chain investments and road upgrades. Tier‑III entry sequence: partner with trusted local aggregators, stand up reefer micro‑hubs, and phase certification/testing with digital audit trails. Localization: festival calendars drive assortment; language‑localized UX and COD/UPI options sustain early adoption. The pie figure captures the evolving city‑tier split by 2030.

Execution: map farm clusters within 100–200 km of demand centers; plan hub‑and‑spoke reefer routes; and schedule dawn delivery waves. Monitor geography‑specific KPIs spoilage, on‑time %, and subscription retention and iterate node placement quarterly.

Competitive Landscape

Competitors span farm‑to‑fork platforms, regional cooperatives, specialty organic marketplaces, and large e‑commerce players adding organic tiers. Differentiation rests on cold‑chain discipline, certification rigor, and subscription basket design. Vendors cluster across WMS/OMS, routing and cold‑chain IoT, compliance automation, and embedded fintech. Procurement guidance: prioritize open APIs, temperature telemetry, and certification tooling; demand SLAs on cold‑chain integrity and payout timing. Competitive KPIs include spoilage %, on‑time %, farmer price realization, subscription retention, and contribution margin after fulfillment. Winners will balance premium positioning with affordability via private‑labels and bundles, while scaling into Tier‑III with trust‑first operations.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071