68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Hyper-Personalization in Emerging Markets: AI-Driven Consumer Insights & Segmentation Strategies for India

India’s consumer markets are entering an AI-first personalization cycle. As smartphone penetration exceeds 80% among urban youth, UPI becomes default for micro-payments, and vernacular internet use expands, brands are racing to turn first‑party signals into real‑time, hyper‑personalized journeys. We model India’s spend on the core personalization stack customer data platforms (CDP), real‑time decisioning, identity stitching, multilingual NLP, and creative rendering rising from ~US$2.8B in 2025 to ~US$8.1B by 2030. The business case rests on measurable uplifts in conversion, repeat purchase, and lower returns, particularly in mobile‑native categories: ecommerce, BFSI, food delivery, travel, telco, OTT, health, and quick commerce. Operationally, hyper‑personalization in India is not merely “right offer, right time.” It is right language, right context, right device often within low‑bandwidth constraints. Leaders are investing in multilingual NLP (Hindi and leading regional languages), on‑device models to respect latency and privacy, and unified identity graphs that bind offline store behaviors with app telemetry and UPI rails.

What's Covered?

Report Summary

Key Takeaways

1. India’s personalization growth is mobile‑native: optimize for low‑latency and variable bandwidth.

2. Multilingual NLP and cultural nuance are decisive differentiators in engagement and conversion.

3. Unified identity across offline store data, app telemetry, and UPI improves attribution and AOV.

4. Real‑time decisioning must be tied to uplift tests and cost‑aware reward catalogs.

5. Edge/on‑device models cut latency, reduce cloud cost, and improve privacy posture.

6. CFO‑credible dashboards: incremental revenue/1k renders, opt‑in rate, interval compression, return‑rate impact.

7. Fairness and consent: audit for bias; keep flows transparent; allow easy preference editing.

8. Shift from discount‑led acquisition to retention‑led growth using lifecycle personalization.

Key Metrics

Market Size & Share

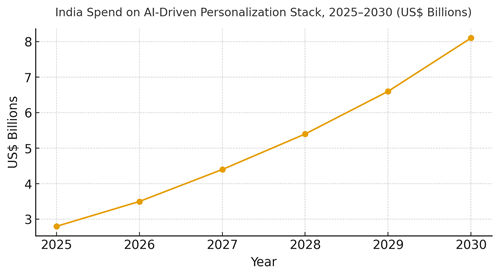

India’s AI‑driven personalization stack is modeled to grow from ~US$2.8B (2025) to ~US$8.1B (2030), propelled by mobile commerce penetration, UPI adoption, vernacular internet expansion, and the maturation of data infrastructure at large consumer platforms. Share dynamics: ecommerce and BFSI lead in spend and measurable ROI, closely followed by telco and food delivery; travel and health tech scale as data and consent mechanics improve. The value pool shifts from broad discounts to **decisioned micro‑offers** tuned by city, language, and lifecycle stage. CDP deployment underpins identity stitching across POS, app telemetry, and payment rails; real‑time decisioning arbitrates between micro‑offers in milliseconds. Multilingual NLP scales targeted conversations and support flows, reducing abandonment. The line figure shows the compounding trajectory through 2030.

Execution guidance: (1) Standardize product/content taxonomies and event schemas; (2) implement holdouts and uplift models to prove incrementality; (3) invest in consent UX and preference centers; and (4) build regional language pipelines (copy + ASR/TTS) tied to QA frameworks. Risks include data quality debt, opaque model behavior, and bias; governance must include bias testing, audit logs, and transparent controls.

Market Analysis

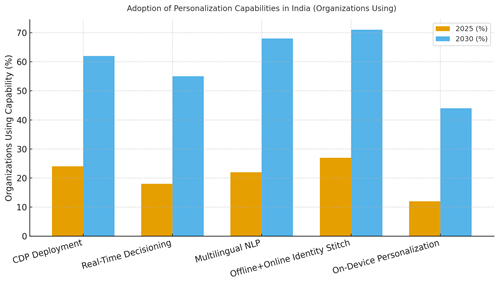

Capability adoption will accelerate as CDPs and identity graphs mature. We project Indian mid/large firms with CDP deployments to rise from ~24% (2025) to ~62% (2030); real‑time decisioning from ~18% to ~55%; multilingual NLP support across top regional languages from ~22% to ~68%; offline+online identity stitching from ~27% to ~71%; and on‑device personalization from ~12% to ~44%. Early ROI appears in abandoned‑cart recovery, credit pre‑qualification nudges in BFSI, language‑localized funnels in ecommerce and travel, and dynamic rewards in food delivery and telco. Barriers: fragmented data, low‑quality event streams, and under‑resourced QA for multilingual content. Organizationally, leaders merge growth, product, data science, and creative ops into a “personalization studio” with weekly experiment cadences.

Financial lens: track incremental revenue per 1,000 personalized renders, AOV uplift, repeat interval compression, margin after rewards, and return‑rate reduction from better fit and expectations. Vendor strategy: prefer modular stacks (CDP + RTD + ID + NLP) with clean APIs and portable data contracts. The bar chart shows step‑function adoption across capabilities by 2030. Execution risk: over‑personalization fatigue; mitigate with frequency caps, cool‑down windows, and preference controls.

Trends & Insights

1) Vernacular acceleration: regional‑language funnels deliver outsized conversion increases; invest in copy and speech (ASR/TTS) with human QA. 2) UPI‑native offers: micro‑rewards and subscriptions transact seamlessly, enabling fine‑grained lifecycle nudges. 3) Edge AI: on‑device rankings and recommendations reduce latency and protect privacy. 4) Micro‑segments, not personas: thousands of real‑time segments defined by signals (city tier, device, time of day, recent purchases) outperform static personas. 5) Creative systems: template libraries render language and city variants; measure creative win‑rates, not just impressions. 6) Bias and fairness: audit models for regional and socioeconomic skew; ensure beneficial outcomes for new‑to‑credit users. 7) Retail media and marketplaces: personalization assets now flow into RMN/marketplace inventory, closing the loop between ads and commerce. 8) Human‑in‑the‑loop: editors refine prompts, tone, and claims especially for regulated categories (BFSI, health). 9) Privacy controls: explicit consent and easy preference editing build trust; communicate benefits of opting in. 10) Training data hygiene: invest in event quality, deduplication, and taxonomy.

Segment Analysis

Ecommerce & Quick Commerce: High event velocity; best‑in‑class ROI from language‑localized funnels and dynamic rewards. BFSI & Fintech: Pre‑qualification nudges, risk‑aware offers, and consent‑centric flows; heavy governance. Telco: Real‑time usage‑based offers and retention signals; on‑device personalization for app catalogs. Travel & Mobility: City‑aware bundles, language routing for support, and dynamic pricing contexts; latency‑sensitive. OTT & Media: Content recommendations and household profiles; frequency caps to avoid fatigue. Health & Wellness: Symptom/goal routing with privacy by design; human oversight for claims. Retail & CPG: Store‑linked identities and receipt/loyalty data used for next‑best‑offer; RMN tie‑ins. Education & EdTech: Regional language content and adaptive pacing; parent‑student profiles. Across segments, track per‑vertical KPIs (AOV uplift, interval compression, returns reduction) and adjust reward catalogs by margin tolerance.

Geography Analysis

India’s personalization spend concentrates in South (~29%), West (~26%), and North (~24%) regions by 2030, with East (~12%), Central (~7%), and Northeast (~2%) representing smaller but growing shares. Drivers include digital infrastructure, language clusters, retail and BFSI density, and startup ecosystems. Southern metros (Bengaluru, Chennai, Hyderabad) anchor tech-forward adoption; Western hubs (Mumbai, Pune, Ahmedabad) benefit from BFSI and retail concentration; Northern markets (Delhi‑NCR) combine media, travel, and government services. Eastern states see growth from ecommerce logistics and telco investments; Central and Northeast regions scale with vernacular internet expansion and low‑bandwidth optimizations.

Localization principles: translate beyond words adapt idioms, festivities, and price sensitivities; ensure scripts and fonts render crisply across devices; and tune voice (ASR/TTS) for regional accents. Operationally, maintain a central content/prompt library while granting regional teams autonomy to test language and creative variants. For measurement, monitor uplift by region, language pairings, and device classes; use these insights to phase rollouts. The pie chart shows the modeled 2030 spend split across Indian regions.

Competitive Landscape

Stacks converge around CDP + real‑time decisioning + identity + multilingual NLP + creative ops. Global vendors compete with India‑first specialists offering vernacular NLP and UPI‑aware flows. Differentiation vectors: (1) event quality tooling (deduplication, schema enforcement), (2) low‑latency serving and on‑device models, (3) multilingual QA pipelines, (4) privacy and consent orchestration, and (5) RMN/marketplace integrations. Buyers should avoid lock‑in with modular contracts and data portability. Competitive KPIs: incremental revenue per 1,000 renders, opt‑in rate, return‑rate reduction, AOV uplift, and edge‑vs‑cloud latency. A quarterly model governance review should test bias/fairness, audit logs, and rollback plans. The winners of 2025–2030 will be those who combine deep regional language competence, strong identity graphs, and CFO‑credible measurement with human‑in‑the‑loop oversight.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071