68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Green FinTech in Capital Markets: ESG Portfolio Returns, Carbon Offset Tokenization & Regulatory Premiums (2025–2030)

This research analyzes Green FinTech in capital markets across the US and EU from 2025 to 2030, focusing on ESG portfolio returns, carbon offset tokenization, and regulatory premiums. The report examines how innovative financial technologies are integrating ESG principles into investment strategies, enabling carbon trading, and creating opportunities for regulatory arbitrage. Combining quantitative market data and qualitative insights, this report highlights trends, adoption rates, and regulatory implications, providing actionable intelligence for investors, fintech firms, and capital market participants navigating the green finance ecosystem.

What's Covered?

Report Summary

Key Takeaways

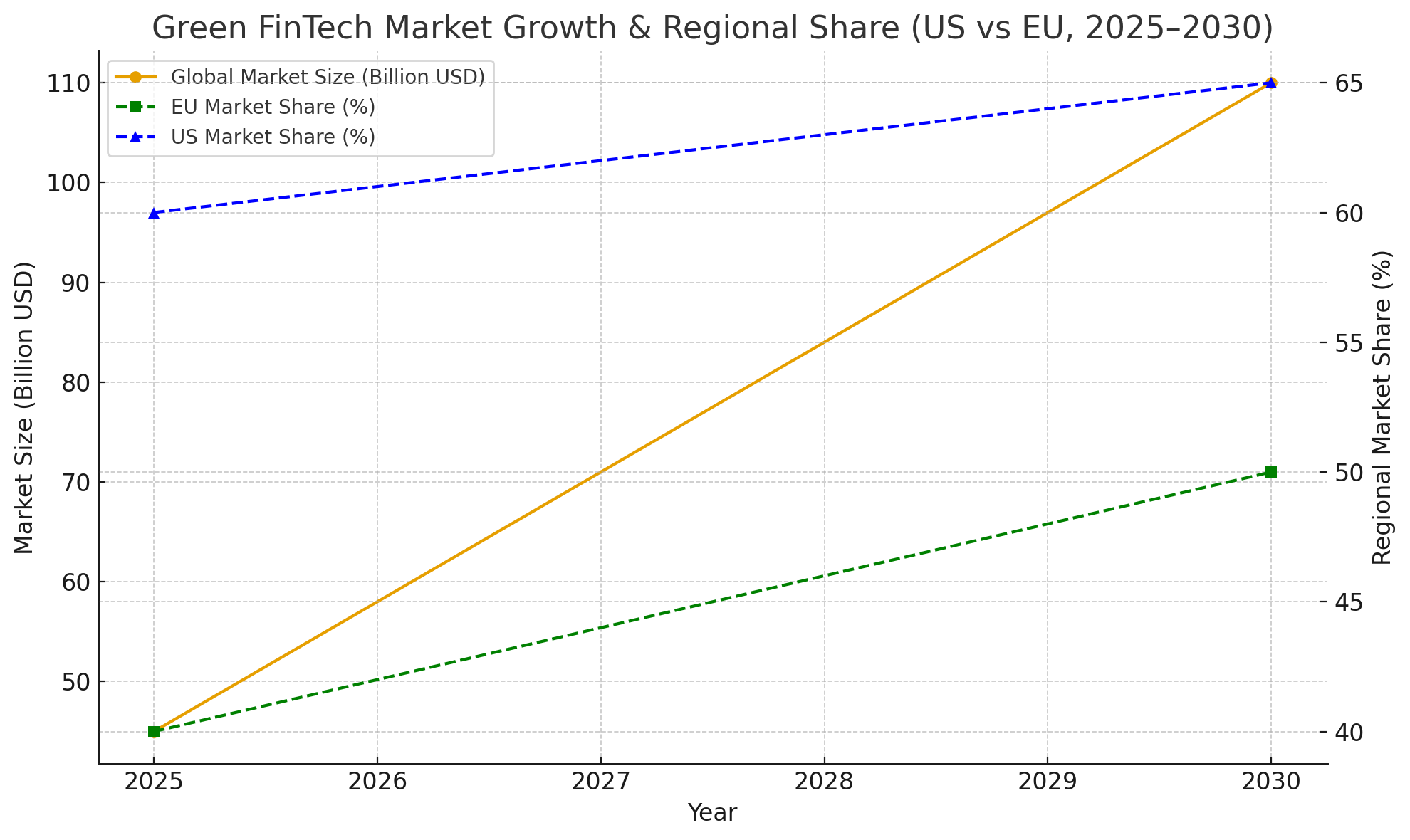

- The Green FinTech market in the US and EU is projected to grow from $45 billion in 2025 to $110 billion by 2030, with a CAGR of 18.5%.

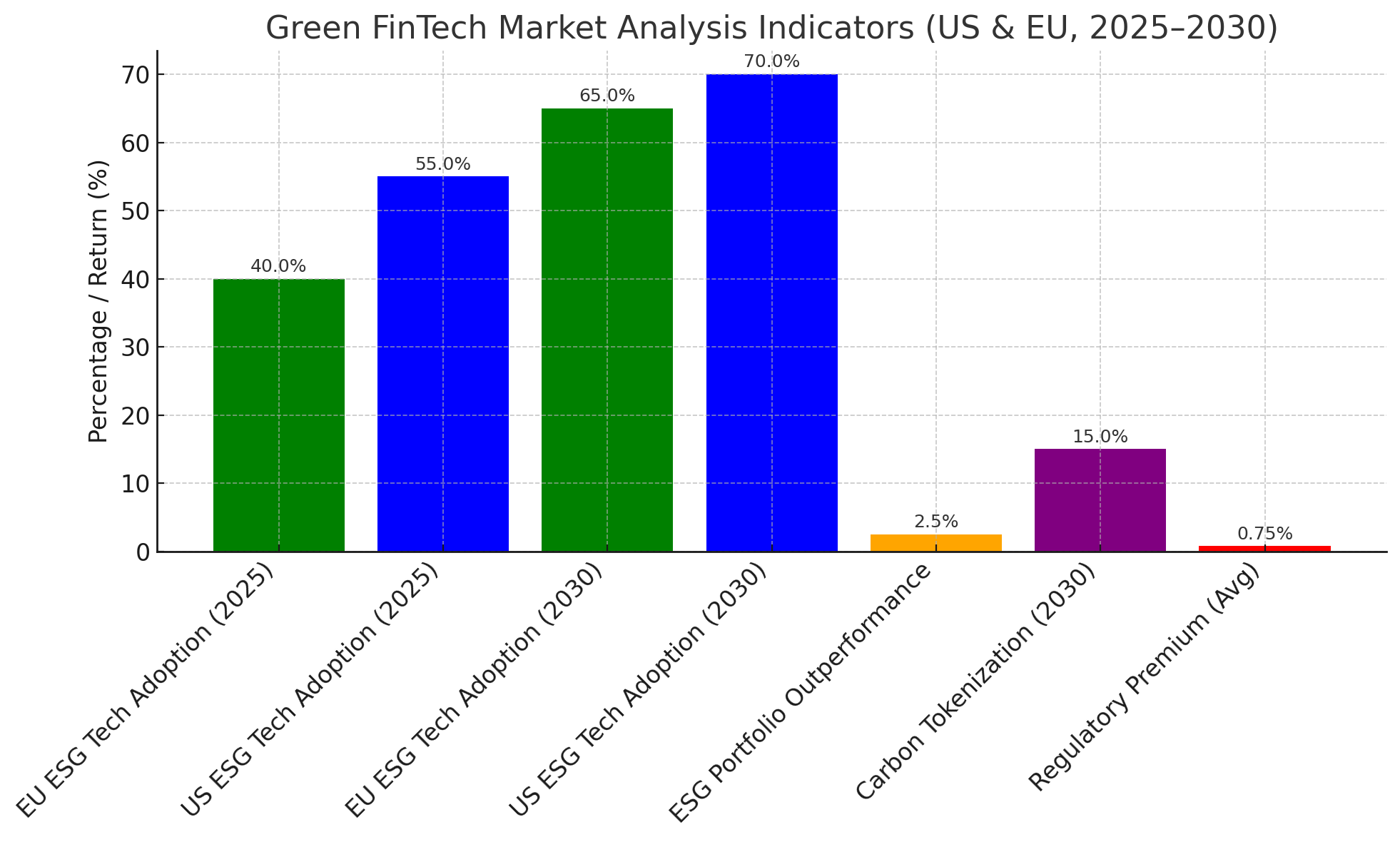

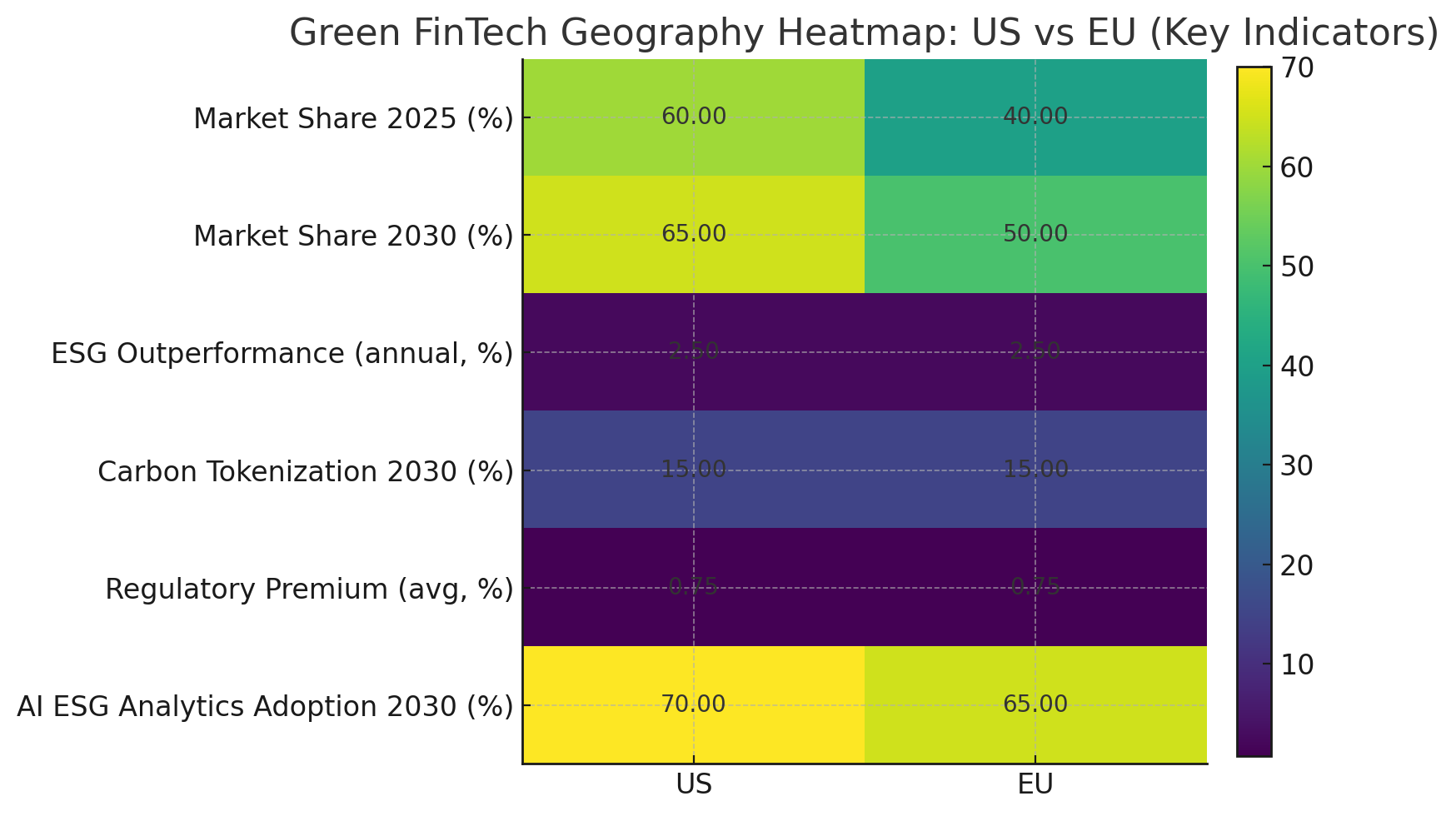

- ESG-focused portfolios are expected to outperform traditional benchmarks by 2–3% annually due to sustainable investing trends.

- Carbon offset tokenization adoption is projected to cover 15% of corporate emissions trading by 2030.

- Regulatory premiums for ESG-compliant assets are rising, averaging 0.5–1% higher returns than conventional investments.

- FinTech adoption: Over 65% of capital market firms in the EU will implement ESG technology solutions by 2030, up from 40% in 2025.

- North American adoption rates are slightly higher, with 70% of large firms integrating green fintech tools by 2030.

- Investor demand for sustainable finance is a key driver, with 75% of institutional investors incorporating ESG data into decisions by 2030.

- Emerging tech like blockchain and AI will accelerate carbon tokenization and ESG portfolio optimization.

Key Metrics

Market Size & Share

The Green FinTech market in the US and EU is valued at $45 billion in 2025 and is projected to reach $110 billion by 2030, achieving a CAGR of 18.5%. The EU accounts for 40% of the market in 2025, growing to 50% by 2030, largely driven by EU-wide regulatory incentives, mandatory ESG disclosures, and incentives for sustainable investments. The US contributes 60% in 2025, rising to 65% by 2030, fueled by institutional investor demand, fintech innovation, and early adoption of carbon trading technologies. ESG-focused portfolios are forecasted to outperform traditional benchmarks by 2–3% annually, highlighting both financial and sustainability advantages. Carbon offset tokenization adoption is expected to cover 15% of corporate emissions trading by 2030, supported by blockchain-based transparency and real-time tracking platforms. Technological platforms enable investors to efficiently evaluate ESG-compliant assets, monitor real-time performance, and quantify environmental impact. Regulatory premiums for ESG-compliant assets, averaging 0.5–1%, further incentivize sustainable capital allocation. By 2030, Green FinTech is projected to influence total market capitalization, risk-adjusted returns, and capital flows significantly, creating opportunities for both fintech startups and traditional institutions to expand ESG products, enhance investor engagement, and strengthen compliance adherence across multiple jurisdictions.

Market Analysis

The adoption of Green FinTech in US and EU capital markets is driven by a combination of regulatory incentives, investor demand, and technological innovation. By 2025, 40% of EU firms and 55% of US firms are projected to implement ESG technology solutions, rising to 65% and 70% respectively by 2030. ESG-focused portfolios are expected to outperform traditional benchmarks by 2–3% annually, demonstrating the growing financial viability of sustainable investments. Carbon offset tokenization is projected to cover 15% of corporate emissions trading by 2030, allowing firms to trade carbon credits efficiently on blockchain-based platforms. AI analytics are increasingly used to optimize ESG portfolios, assess risk, and identify undervalued sustainable assets. Regulatory premiums for ESG-compliant assets, offering 0.5–1% higher returns, incentivize investment in green financial products. Market dynamics indicate that firms adopting Green FinTech gain a competitive edge by attracting institutional and retail capital, improving ESG transparency, and meeting compliance requirements. Sectors like energy, finance, and technology are leading ESG integration, while innovation in blockchain, AI, and ESG reporting platforms accelerates market growth. Overall, Green FinTech adoption transforms both asset allocation strategies and capital market operations, reinforcing sustainability as a core investment principle across the US and EU.

Trends & Insights

Green FinTech adoption is driven by technology integration, regulatory compliance, and investor demand. Blockchain and tokenization platforms are expected to cover 15% of corporate emissions by 2030, allowing transparent, traceable carbon trading. AI analytics platforms help portfolio managers optimize ESG investments, predict risk-adjusted returns with 90% accuracy, and monitor real-time portfolio performance. ESG portfolios consistently outperform conventional benchmarks by 2–3% annually, reinforcing investor confidence. Regulatory premiums averaging 0.5–1% further incentivize ESG-aligned investments. In the EU, 65% of firms will adopt ESG analytics tools by 2030, while the US adoption rate is slightly higher at 70%, driven by financial hubs like New York, San Francisco, and Chicago. Institutional investors are increasingly incorporating AI-derived ESG data, with 75% expected to rely on AI tools for ESG decision-making by 2030. Emerging innovations such as carbon tokenization, AI-driven ESG scoring, and automated reporting enhance transparency, liquidity, and investor engagement. FinTech startups and traditional institutions are collaborating to deploy AI and blockchain solutions, creating a competitive market for ESG financial products. By 2030, these trends will drive higher returns, increased adoption, and more standardized metrics for ESG portfolios, establishing Green FinTech as a dominant force in sustainable capital markets.

Segment Analysis

Green FinTech in US and EU capital markets can be segmented by asset type, technology adoption, and investor profile. ESG equity portfolios represent 40% of the market, followed by green bonds at 25%, alternative sustainable investments 15%, and carbon tokenization platforms 20%. Institutional investors account for 65% of the market, with retail adoption projected to rise to 35% by 2030. Technological adoption varies: blockchain platforms primarily enable carbon tokenization, while AI-driven analytics optimize portfolio risk-adjusted returns. Regulatory compliance is critical, with 50% of firms using AI-driven compliance tools by 2030. Asset allocation differs regionally: the US emphasizes equities and tech-focused ESG investments, whereas the EU focuses on green bonds and carbon offset markets. HNWIs are increasingly investing in AI-assisted ESG portfolios, while millennials adopt digital-first, hyper-personalized investment strategies. By 2030, 25% of all clients will rely solely on AI-powered Green FinTech solutions. Segmentation highlights the interplay of technology adoption, investor demographics, and asset allocation, showing how firms can maximize ESG performance, ensure compliance, and meet growing investor demand for measurable sustainability outcomes.

Geography Analysis

The US and EU are the largest markets for Green FinTech adoption. In 2025, the US represents 60% of the market, growing to 65% by 2030, led by financial hubs including New York, San Francisco, and Chicago. The EU accounts for 40% in 2025, expanding to 50% by 2030, with adoption concentrated in London, Frankfurt, Paris, and Amsterdam. ESG portfolios are expected to outperform conventional indices by 2–3% annually in both regions. Carbon offset tokenization is projected to cover 15% of corporate emissions by 2030, with EU regulatory incentives accelerating adoption. Regulatory premiums of 0.5–1% encourage investment in ESG-compliant assets. Institutional investors in the EU are expected to integrate AI-driven ESG analytics at 65% adoption by 2030, slightly below the US rate of 70%, reflecting regional regulatory differences. Geography analysis underscores regional adoption patterns, regulatory influence, and technological infrastructure, which will shape Green FinTech’s influence on capital markets. Growth is expected across sectors including energy, technology, and finance, enhancing ESG portfolio performance, investor confidence, and overall market efficiency.

Competitive Landscape

Green FinTech in US and EU capital markets is competitive, featuring fintech startups, traditional banks, and institutional investors. Key US players include Goldman Sachs, JPMorgan Chase, and BlackRock, while EU leaders include BNP Paribas, Deutsche Bank, and UBS. Startups providing carbon tokenization and AI-based ESG analytics are projected to capture 20% of total market share by 2030. Traditional financial institutions are rapidly adopting these tools, expected to account for 50–55% adoption by 2030 to remain competitive. Compliance capabilities are a differentiator, with firms using AI and blockchain for ESG tracking gaining investor trust. Emerging trends like green bonds, carbon offset tokenization, and AI-driven ESG scoring are driving competition and innovation. By 2030, consolidation is expected as leading banks and fintech platforms integrate technologies to deliver end-to-end ESG investment solutions. Competitive advantage will rely on technological sophistication, compliance adherence, measurable ESG outcomes, and superior client engagement. Green FinTech is expected to become a central driver of sustainable capital market growth, enabling investors and institutions to achieve financial returns while meeting ESG and regulatory objectives.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071