68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Global Fitness Tracker Market Set for 4.5X Growth: USD 71.92 Billion (2025) to USD 323.47 Billion (2034), at 18.04% CAGR

The global fitness tracker market is expected to grow from USD 71.92 billion in 2025 to USD 323.47 billion by 2034, achieving a CAGR of 18.04%. Growth is driven by rising demand for wearable health technology, the integration of AI-driven fitness analytics, and the expansion of connected health ecosystems across developed and emerging economies. The market’s rapid evolution reflects a shift from basic step-counting devices to multi-sensor platforms monitoring cardio, sleep, stress, and glucose levels. With corporate wellness programs, telemedicine integration, and subscription-based analytics accelerating adoption, fitness trackers are becoming an essential pillar of preventive healthcare worldwide.

What's Covered?

Report Summary

Key Takeaways

- Market to grow 4.5×, reaching USD 323.47B by 2034 from USD 71.92B in 2025.

- CAGR projected at 18.04% (2025–2034).

- Asia-Pacific to lead adoption, holding 45% of global share by 2034.

- Smartwatches to capture 50% of total sales, dominating wearable formats.

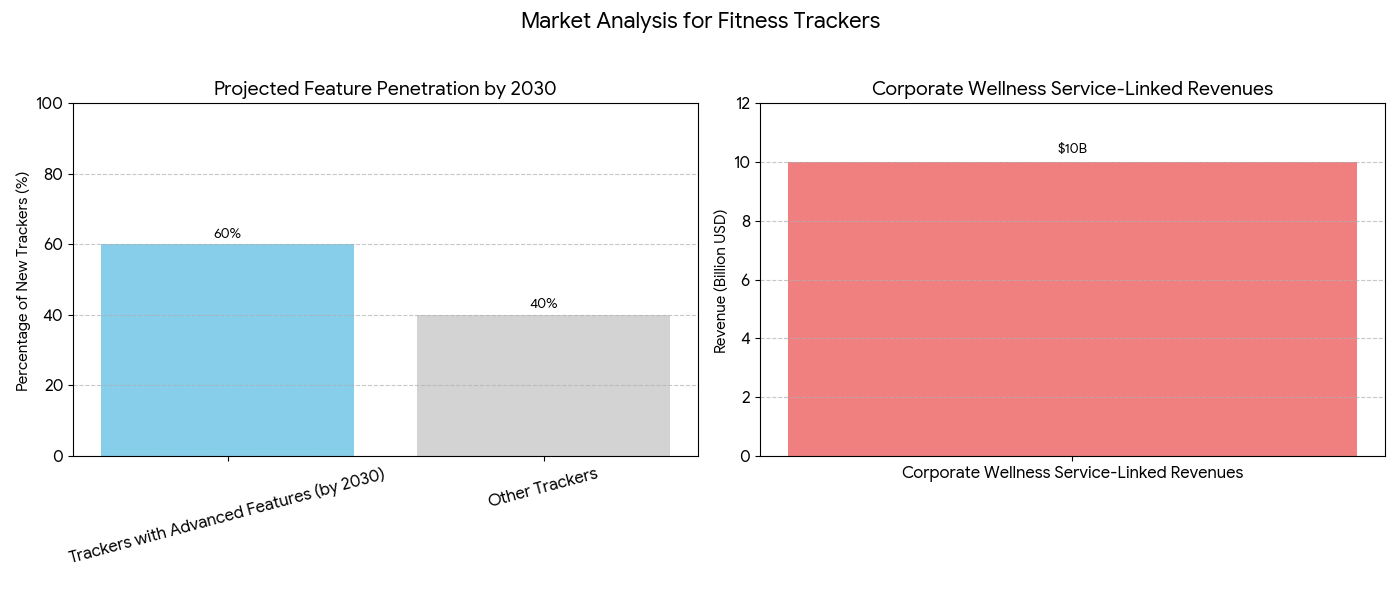

- AI-powered health insights to drive 60% of new device purchases.

- Corporate wellness programs expected to generate USD 10B+ in tracker-linked services.

- North America to contribute USD 110B in annual sales by 2032.

- Subscription-based fitness data analytics to reach USD 20B by 2030.

- Integration with health insurance and telemedicine to improve policy efficiency by 32%.

- Over 1 billion connected fitness devices to be active globally by 2034.

Key Metrics

Market Size & Share

The fitness tracker market will expand from USD 71.92B (2025) to USD 323.47B (2034), supported by widespread adoption in North America, Europe, and Asia-Pacific. The Asia-Pacific region led by China, India, and Japan will command 45% market share, driven by affordable smartwatches and health-conscious consumer trends. North America, accounting for USD 110B by 2032, will sustain strong growth due to corporate health initiatives and medical-grade wearables. The smartwatch segment, with 50% share, will outpace fitness bands and rings, while AI-enhanced trackers become the preferred format for precision health monitoring.

Market Analysis

Global demand for fitness trackers reflects a convergence of consumer electronics, digital health, and wellness technology. The integration of AI-driven biometric analytics and predictive health algorithms is transforming passive trackers into proactive diagnostic tools. By 2030, over 60% of new trackers will include continuous glucose monitoring, stress mapping, and blood oxygen tracking. Corporate wellness programs, especially in the U.S., Europe, and Asia, are expanding device-based incentives for employees, generating USD 10B in service-linked revenues. As cloud platforms connect wearables to telehealth and insurance ecosystems, the data monetization model via subscriptions, insights, and healthcare partnerships is becoming a key revenue driver.

Trends & Insights

- Health Tech Convergence: Fitness trackers are merging with clinical-grade diagnostics and telehealth.

- AI Personalization: Machine learning improving calorie and heart-rate accuracy by >30%.

- Corporate Health Expansion: Businesses funding tracker subscriptions for employee engagement.

- Subscription Revenue Models: Analytics-based services driving USD 20B+ recurring income.

- Wearable Ecosystem Growth: Integration with AR/VR fitness, metaverse gyms, and virtual training.

- Next-Gen Sensors: Advancements in bioimpedance and hydration tracking.

- Elderly Market Adoption: 28% of new devices to target aged 55+ demographics.

- Insurance Integration: Premium discounts tied to active tracking and verified fitness data.

- Regional Growth: China and India emerging as cost-efficient manufacturing and demand centers.

- Data Security Emphasis: Health data encryption compliance with GDPR and HIPAA frameworks.

Segment Analysis

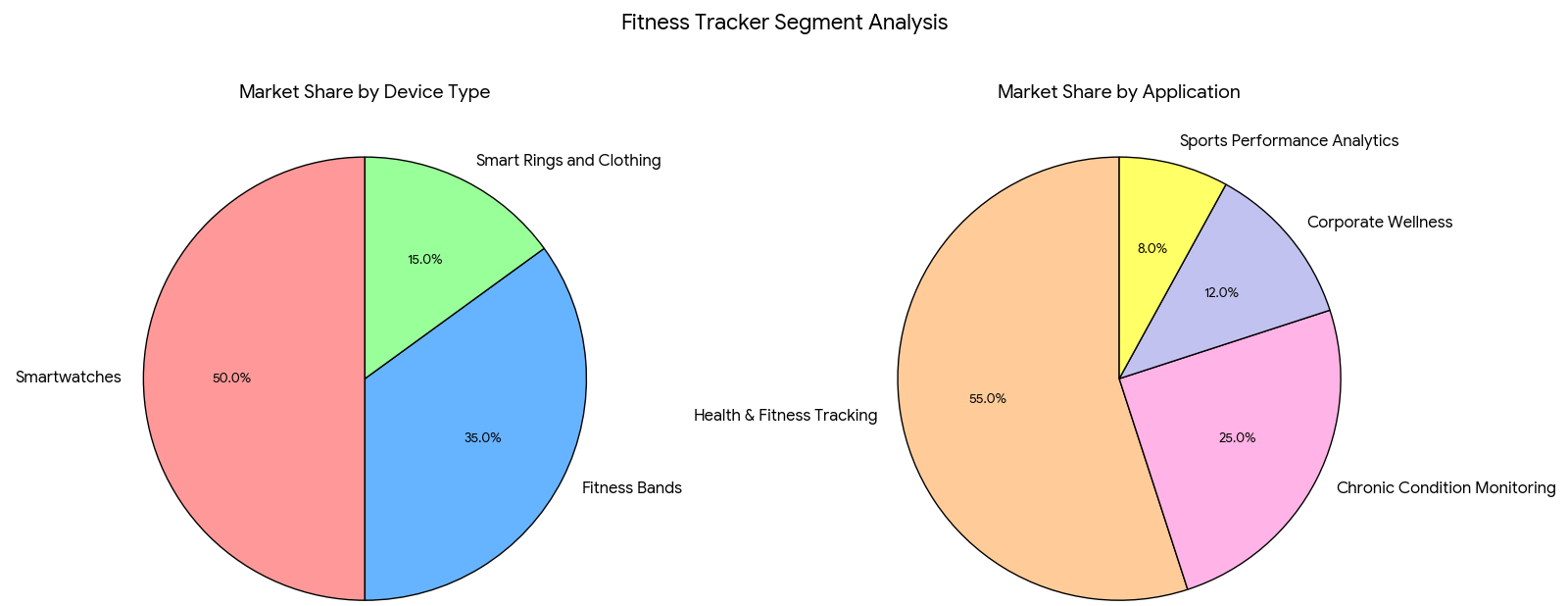

By device type, smartwatches (50%), fitness bands (35%), and smart rings and clothing (15%) dominate. Smartwatches lead due to expanded health features like ECG, blood oxygen, and temperature tracking. Fitness bands retain traction in emerging markets due to affordability, while smart rings and wearable apparel are gaining popularity in sports and clinical monitoring. By application, health & fitness tracking (55%) remains the largest, followed by chronic condition monitoring (25%), corporate wellness (12%), and sports performance analytics (8%). Subscription-based analytics and ecosystem integration will drive recurring revenue growth across all device segments.

Geography Analysis

Asia-Pacific leads with 45% global share, followed by North America (30%), Europe (18%), and Latin America & MEA (7%). China and India dominate manufacturing and domestic consumption, fueled by affordable devices from Xiaomi, Noise, and Amazfit. North America remains the highest-value market, generating USD 110B by 2032, driven by Apple, Fitbit, and Garmin. Europe is seeing steady growth under digital health regulations and insurance-linked wearable programs. By 2034, cross-platform health data interoperability and 5G-enabled wearables will accelerate adoption across all key regions.

Competitive Landscape

Leading players include Apple, Fitbit (Google), Samsung, Garmin, Huawei, Xiaomi, Whoop, Oura, and Amazfit. Apple continues to dominate with its Watch Series ecosystem, accounting for over 35% global smartwatch market share. Fitbit and Garmin focus on medical-grade data and corporate partnerships, while Whoop and Oura target premium wellness subscriptions. Asian brands like Xiaomi and Amazfit lead in affordability, democratizing wearable adoption in India and Southeast Asia. The competitive landscape is shifting toward AI integration, cloud analytics, and predictive diagnostics, with players racing to secure regulatory clearances for FDA and CE-compliant health monitoring devices, transforming wearables into an integral part of the global healthcare ecosystem.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071