68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Gen-Z Loyalty Programs: Gamification Mechanics & Tokenized Reward Systems in Asia-Pacific Beauty Markets

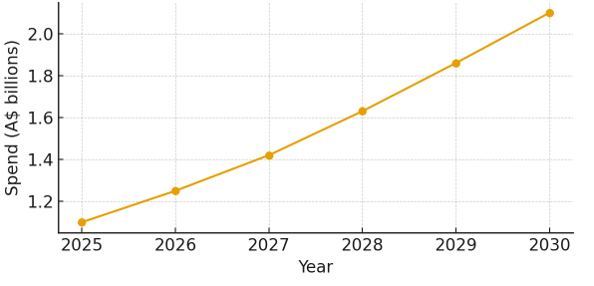

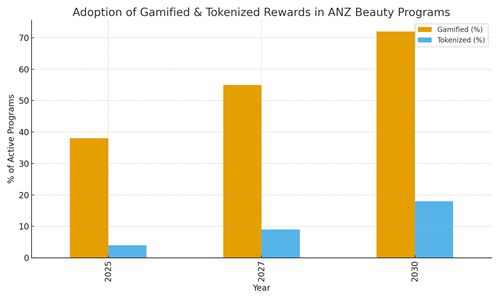

Gen‑Z shoppers (born ~1997–2012) are redefining loyalty performance in Australia and New Zealand (ANZ) beauty retail by demanding instant value, interactive product discovery, and rewards that travel seamlessly across channels. Australia’s beauty & personal care market is projected at ~US$6.07B in 2025, growing to ~US$8.02B by 2030 (CAGR ~5.7%). Participation in retail loyalty is already mainstream ~84% of Australians are enrolled yet the upside now lies in program quality: gamified mechanics that convert discovery into repeat purchase, and, selectively, tokenized rewards that add portability and creator‑economy utility. Our model of ANZ Gen‑Z loyalty‑influenced beauty spend indicates growth from ~A$1.1B (2025) to ~A$2.1B (2030), underpinned by three drivers: (1) base category growth, (2) higher Gen‑Z engagement, and (3) rapid adoption of behavior‑linked quests that reward actions such as AR skin diagnostics, regimen completion, and UGC creation. Program design is shifting from “earn & burn” to mission‑based systems that pace value through daily and weekly challenges, tier acceleration, and limited‑time events. By 2030, we expect ~72% of ANZ beauty programs to embed gamified features (vs. ~38% in 2025), while tokenized rewards scale from ~4% to ~18% as brands pilot portability across partners and events.

What's Covered?

Report Summary

Key Takeaways

1. Gamification is becoming table stakes; it reliably increases session frequency and repeat baskets among Gen‑Z.

2. Treat loyalty as performance media: optimize toward active questers, completion rate, and reward velocity.

3. Coalition programs provide baseline value; brand quests provide depth, data, and margin control.

4. Tokenized rewards work when portability or co‑creation utility is obvious; keep UX frictionless.

5. K‑beauty & skincare are the highest‑fit categories for challenge loops and regimen streaks.

6. Design guardrails to curb discount leakage (behavior‑linked rewards, caps, and tier pacing).

7. Fuse store services (diagnostics, makeovers) with app missions for omnichannel lift.

8. Dashboard shift: measure incremental margin, cross‑category expansion, and interval compression.

Key Metrics

Market Size & Share

Australia’s beauty & personal care market expands from ~US$6.07B in 2025 to ~US$8.02B by 2030 (CAGR ~5.7%), providing a stable base for loyalty‑driven growth. Within this backdrop, we model ANZ Gen‑Z loyalty‑influenced beauty spend rising from ~A$1.1B (2025) to ~A$2.1B (2030). The model integrates: (1) category growth forecasts, (2) high loyalty enrollment and reported spend uplift among members, and (3) adoption of behavior‑linked mechanics (quests, streaks, AR diagnostics) that shift value from static discounts to measured, incremental actions. The program penetration story matters: as more beauty retailers embed gamified missions and real‑time personalization, the share of transactions attributed to loyalty mechanics steadily increases. Coalition ecosystems (e.g., Flybuys) contribute baseline earn/redeem utility and higher redemption frequency, while specialist beauty retailers add depth through curated experiences and tier accelerators. We assume loyalty influence is strongest in skincare where routines and measurable outcomes support habit formation and rising in haircare and suncare via education‑led missions. Sensitivities include margin pressure from excessive reward velocity, execution risk in stores (staff enablement), and macro factors that may alter discretionary spend profiles. A practical governance approach links rewards to profitable behaviors (e.g., regimen completion, cross‑category trial), caps monthly benefit accrual, and directs bonuses to high‑lifetime‑value cohorts. By 2030, programs that actively manage mission design and segment pacing should realize 2–4 pp higher repeat‑purchase rates than non‑gamified peers. Data infrastructure is critical: brands should attribute lift via holdout experiments (store clusters or audience splits) and track interval compression (days between purchases) alongside cross‑category expansion. The overarching message: loyalty’s contribution to Gen‑Z beauty spend is compounding, driven by better mechanics, better data, and better omnichannel execution.

Market Analysis

ANZ beauty programs are moving from points‑only constructs to behavior‑linked systems that reward specific, profitable actions. We estimate gamified features in ~38% of programs in 2025, growing to ~55% by 2027 and ~72% by 2030. Tokenized rewards start from a small base (~4%) and expand to ~18% as brands seek portability across partners, events, and creator collaborations. The financial thesis is straightforward: quests convert attention into incremental visits and larger baskets while avoiding blanket discounting. Recommended mechanics include: (1) micro‑missions (try a diagnostic, sample a routine, share UGC), (2) streaks with soft resets, and (3) “path to prestige” tiers that pace benefits. Gamification economics depend on calibrated reward velocity measured as average earn→redeem time and on cost per incremental visit. On tokenization, value appears where rewards must be portable (coalitions, partner festivals) or where secondary markets create buzz; otherwise, a traditional ledger suffices. Operationally, brands should construct a quest library per category, with configurable difficulty and caps, and use real‑time first‑party data to trigger dynamic offers (e.g., regimen completion bonus within 48 hours). Experimentation frameworks should include A/B tests on challenge types, streak lengths, and tier thresholds, with KPIs spanning completion rate, interval compression, category expansion, and incremental gross margin. Finally, align stores and digital: convert consultations, classes, and services into missions that deliver instant value, then retarget via app journeys. By 2030, we expect the competitive gap to widen as leaders treat loyalty as performance media, integrating analytics, creative, and ops in a single cadence.

Trends & Insights

1) Gamification as default UX: Users expect instant feedback, small wins, and visible progress. Beauty brands pair AR try‑ons and diagnostic tools with micro‑rewards, translating exploration into measurable habits. 2) Coalition value in a cost‑of‑living context: Broader earn/redeem rails lift perceived value; higher redemption rates signal liquidity and confidence. 3) Tokenization with utility: When rewards act like portable assets usable across partner events or creator collabs engagement improves; when utility is unclear, complexity harms adoption. 4) K‑beauty momentum: Fast innovation cycles, regimen‑driven education, and social discovery make K‑beauty a natural anchor for quest libraries. 5) In‑store × app fusion: Services (consultations, makeovers) should appear as missions with instant credit, ensuring data capture and next‑best‑action offers. 6) Data‑led personalization: First‑party signals diagnostic outcomes, preferred textures/shades, sensitivity flags power next purchase suggestions and reduce returns. 7) Guardrails matter: Cap monthly benefits, vary mission difficulty, and link boosts to higher‑margin products. 8) Measurement discipline: Use audience or store‑cluster holdouts; track challenge completion, repeat interval, category expansion, and incremental gross margin; monitor reward velocity to avoid margin erosion. 9) Creative ops: Refresh quests monthly; attach surprises to product newness and seasonal events; test social‑referral boosts that reward dyads or small groups. 10) Compliance & trust: Keep tokenization invisible to the user; communicate plainly; avoid exposing fees; ensure clear terms for portability and expiry. Collectively, these trends imply a playbook that is experiential, data‑rich, and margin‑aware, with loyalty treated as an always‑on performance engine.

Segment Analysis

Skincare: Highest fit for game loops due to daily routines and measurable outcomes. Anchor quest libraries around regimen steps (cleanse, treat, moisturize, SPF), 7‑ and 14‑day streaks, and diagnostic follow‑ups. Expect strongest lift in repeat‑purchase interval compression and cross‑sell to serums and suncare. Color Cosmetics: Short feedback loops and strong creator influence. Use UGC challenges, shade‑match try‑ons, and limited‑time “look” bundles; reward try‑ons that convert to mini→full‑size upgrades. Haircare: Education‑led missions (scalp health, heat protection) and regimen bundles (“shampoo+mask+oil”) drive attachment. Leverage subscription options with streak bonuses. Fragrance & Body: Seasonality and gifting peaks support event‑based quests; tie experiential rewards (scent profiling, engraving) to premium tiers. Suncare: High‑relevance in AU summers; run protection‑education quests and routines that unlock multi‑pack value. Men’s Grooming: Lower baseline engagement but rising; emphasize routine simplicity and replenishment reminders. Across segments, combine coalition base value (points everywhere) with brand‑specific depth (missions that collect meaningful signals). Track per‑segment KPIs: challenge completion, repeat interval, AOV, and margin after rewards. Introduce soft difficulty scaling entry missions for new members, advanced paths for enthusiasts to pace benefits. For tokenized rewards, restrict to collaborations where portability, collectibility, or co‑creation is central; otherwise keep rewards ledger‑based to minimize complexity. Competitive differentiation stems from mission craft (useful education, fun challenges), fast creative refresh cycles, and omnichannel execution that makes stores essential nodes in the progression system.

Geography Analysis

Australia represents ~85% of ANZ Gen‑Z loyalty‑influenced beauty spend; New Zealand accounts for ~15%, reflecting population, store density, and coalition coverage. Australia’s market benefits from large specialist footprints (e.g., Mecca, Sephora), strong online penetration, and established coalition rails (Flybuys, Everyday Rewards), which increase redemption liquidity and program utility. New Zealand, while smaller, exhibits strong responsiveness to digital‑first mechanics; app‑centric missions and social referrals travel well. Localization principles: in AU, lean into summer suncare education quests, festival calendars, and in‑store services integrated with app missions; in NZ, prioritize mobile‑first flows, social proof, and community‑driven perks. Operationally, harmonize currencies and tier names across markets but tailor quest libraries to local seasonality and product preferences. Track geography‑specific KPIs: active questers as a share of members, challenge completion, and store‑linked mission participation. Inventory and staffing planning should mirror quest calendars align newness drops, sampling, and service capacity with peak mission windows. For tokenized pilots, test cross‑market portability only where partner networks exist and regulatory considerations are clear; otherwise, keep reward value local to reduce complexity. By 2030, we expect Australia to remain the primary volume driver, with New Zealand contributing outsized engagement on a per‑capita basis due to higher mobile reliance and community mechanics. The strategic aim is consistent: maintain a common backbone for measurement and governance while allowing creative and seasonal variation to reflect local culture and retail rhythms.

Competitive Landscape

Retail specialists (Mecca, Sephora, Adore Beauty) define category experience, while coalitions (Flybuys, Everyday Rewards) define mass liquidity. Leaders converge on three moats: experience (in‑store diagnostics fused with app missions), data (first‑party signals from mission completions), and value (baseline coalition utility plus brand‑specific quests). Mecca’s tiered benefits and experiential events set expectations for prestige; Sephora leverages omnichannel services and exclusive launches; Adore is scaling omnichannel reach. Coalitions deliver everyday value and redemption breadth that matter during cost‑of‑living pressure. Challenger DTC and indie brands win through creative velocity: monthly quest refreshes, creator‑linked challenges, micro‑drops, and community rewards. The emerging frontier is selective tokenization: perks that are portable across collaborators or act as access keys to drops and events kept invisible under the hood to avoid UX friction. Competitive KPIs include active questers, completion rate by mechanic, incremental margin after rewards, and cross‑category expansion rates. Execution risks: undisciplined discounting disguised as gamification; reward inflation; store‑ops bottlenecks that break the loop between services and app missions. Governance should link benefits to profitable behaviors, enforce caps, and run constant holdout testing. Playbooks that win: (1) build a quest library per segment with clear objectives and measurable outcomes; (2) integrate store calendars and staffing with mission peaks; (3) align creative and analytics teams on a weekly optimization cadence; (4) maintain a small but active backlog of tokenized pilots where portability or co‑creation is essential. By 2030, the spread between loyalty leaders and laggards in ANZ beauty will widen materially, reflected in repeat‑purchase intervals, category breadth per member, and contribution margin after rewards.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071