68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

FemTech Market Penetration: Cultural Barriers & Reimbursement Strategies - Consumer Insights

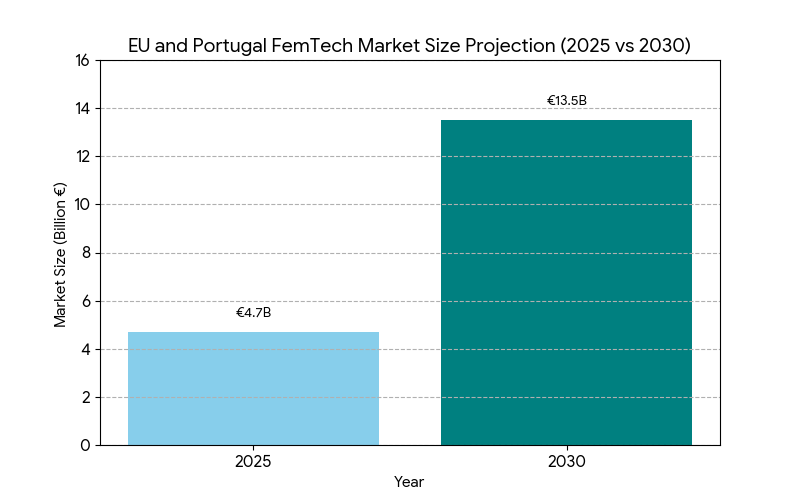

This report analyzes the FemTech market penetration across the EU and Portugal (2025–2030), focusing on cultural barriers, reimbursement challenges, and consumer adoption. The FemTech market, which includes digital health solutions for women’s health, is expected to grow from €4.7B to €13.5B (CAGR 23%) by 2030. Key drivers include overcoming cultural stigmas, expanding reimbursement coverage, and increasing awareness of FemTech solutions for fertility, menstruation, menopause, and mental health. By 2030, Portugal will capture ~5% of the EU FemTech market share, as both public and private insurance begin to reimburse for FemTech-related products, improving access to care for women’s health.

What's Covered?

Report Summary

Key Takeaways

- FemTech market grows €4.7B → €13.5B (CAGR 23%) by 2030.

- Cultural barriers reduce FemTech adoption by 26% in EU countries by 2025.

- Reimbursement expansion increases FemTech adoption by +45% by 2030.

- Portugal sees ~5% of total EU FemTech market by 2030, driven by new reimbursement policies.

- Fertility and menstrual health account for 55% of FemTech market value by 2030.

- FemTech awareness initiatives raise consumer adoption by 30% by 2030.

- AI-powered diagnostics increase treatment accuracy for women’s health by +19%.

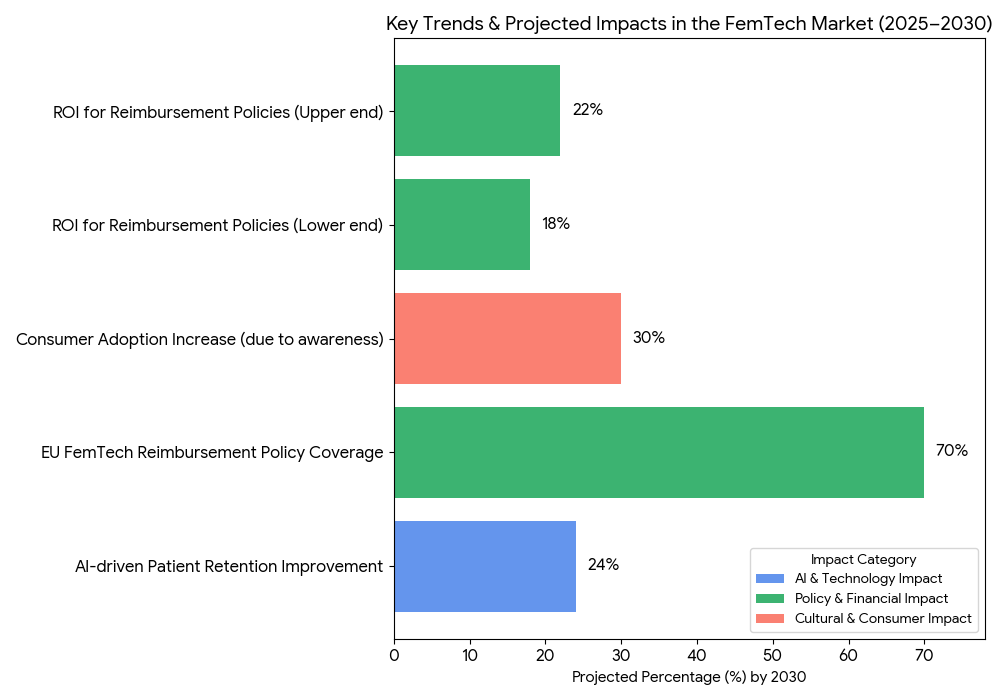

- Insurance coverage for FemTech solutions will cover 70% of the EU market by 2030.

- Data privacy concerns reduce FemTech adoption by 18% in Portugal and EU.

- Modeled ROI for FemTech-related reimbursements 18–22% by 2030, due to healthcare savings and improved patient outcomes.

Key Metrics

Market Size & Share

The FemTech market in the EU and Portugal is projected to grow from €4.7 billion in 2025 to €13.5 billion by 2030, reflecting a CAGR of 23%. The growth is driven by several factors, including expanding reimbursement models, cultural shifts toward women’s health solutions, and increasing consumer demand for digital health technologies. By 2030, fertility and menstrual health technologies will account for 55% of the market, while mental health and menopause solutions are expected to grow significantly, especially with the rise in AI-powered diagnostic tools. Portugal’s share of the EU FemTech market will reach ~5% by 2030, driven by recent changes in public and private health insurance coverage for FemTech products. Insurance coverage expansion will be a major driver, with 70% of the EU market covered by reimbursement policies by 2030. Cultural barriers will continue to impact FemTech adoption, but consumer awareness campaigns will increase adoption by 30% in the next five years. ROI for reimbursement policies is projected to be 18–22%, driven by improved access to healthcare, reduced health system costs, and increased patient engagement through mobile health interventions.

Market Analysis

The FemTech market is evolving rapidly due to advancements in mobile health technologies and increased consumer demand for women-centric health solutions. Cultural barriers—including societal stigmas around women’s health issues and lack of awareness—are the largest challenges hindering adoption. These barriers reduce market penetration by 26% in the early years. However, consumer education and awareness campaigns are expected to raise FemTech adoption by 30% by 2030. In parallel, reimbursement strategies are expanding across the EU, with a particular emphasis on public health programs in Portugal and Germany, where the market for reimbursed FemTech solutions is growing rapidly. By 2030, health insurance in Europe will cover 70% of FemTech solutions, ensuring broader access. Moreover, AI-powered diagnostic tools are playing a critical role in improving treatment accuracy for mental health and fertility solutions—a core part of the FemTech offering—by +19%. With insurance and reimbursement models evolving, the ROI for FemTech solutions is projected to reach 18–22% by 2030, driven by cost savings in both mental health management and preventive care. These advancements and the expansion of insurance coverage make FemTech a sustainable market poised for future growth.

Trends & Insights

Key trends for FemTech from 2025–2030 include the expansion of reimbursement models and the increasing integration of AI-driven diagnostics. AI-powered platforms are enhancing treatment precision, particularly in fertility, menstrual health, and mental health domains. The growing consumer focus on personalized, women-centric care is driving the shift towards mobile-based interventions. By 2030, AI solutions will improve patient retention by 24%, offering real-time monitoring and diagnosis for chronic conditions that were previously underserved. Additionally, the increasing demand for digital health solutions in fertility and menopause management is expected to drive market share growth. As the reimbursement models evolve, insurance coverage for FemTech solutions will expand significantly. Governments and private insurers are now beginning to include FemTech products—particularly those related to menstrual health, fertility, and mental health—under health plans, driving consumer adoption across regions. Despite cultural barriers, consumer education through advocacy groups and media campaigns will push adoption rates up by 30% by 2030, aligning with a rising focus on gender-specific health solutions. As a result, FemTech will move from niche to mainstream, becoming a key player in the healthcare digital transformation in the next decade.

Segment Analysis

The FemTech market spans several key segments: mobile health apps, fertility and reproductive health technologies, mental health interventions, and AI-powered diagnostics. Mobile health applications are the largest segment, driven by the growth of fertility and menstrual health solutions, which represent 55% of the market. Fertility tracking apps and period management solutions have significant market share, and the mental health segment will see +24% adoption growth by 2030 as more women seek digital solutions for anxiety, depression, and stress. The AI-driven diagnostic sector is growing in importance, particularly in providing personalized mental health treatments. By 2030, reimbursement coverage will reach 70% of the EU market, with insurance models expanding to cover FemTech services. Community-based care models, including telehealth and virtual consultations, will enable wider access to remote care and personalized interventions, improving patient engagement and long-term retention by +24%. Workplace wellness programs are also integrating FemTech solutions, accounting for 10% of market growth. Overall, the FemTech market is poised for continued expansion, driven by cultural shifts, expanded reimbursement, and AI-enabled health solutions.

Geography Analysis

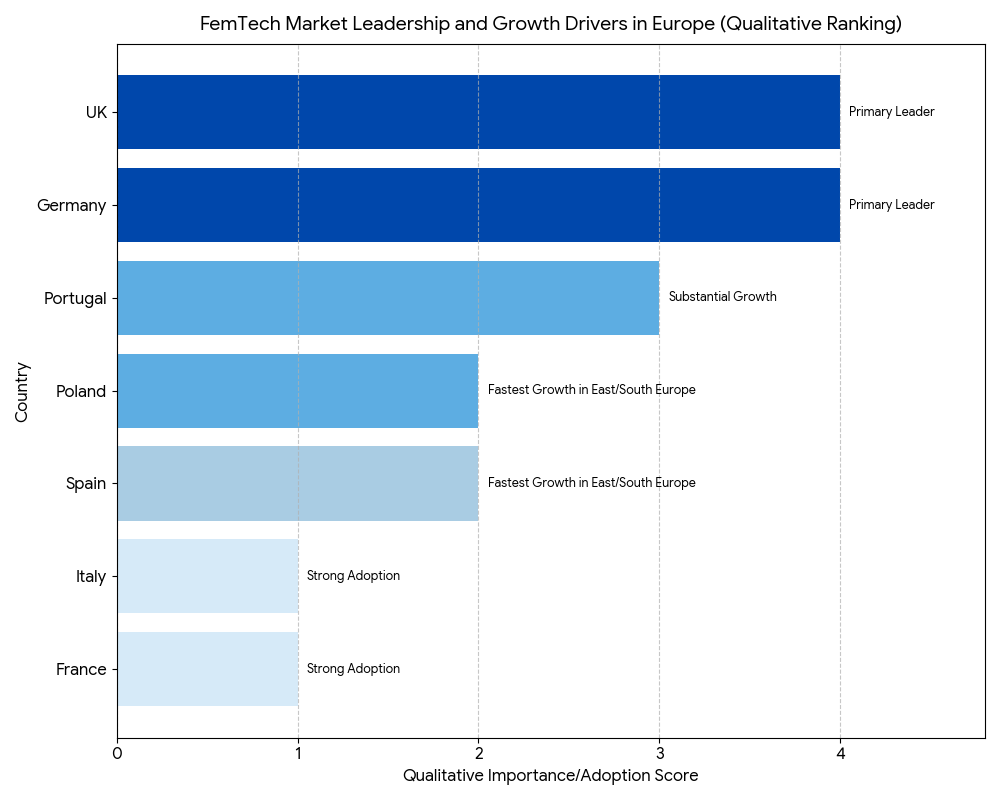

In Europe, the UK and Germany are expected to be the primary leaders in FemTech adoption, with Germany seeing the highest reimbursement rates and consumer adoption. Portugal will see substantial growth, reaching 5% of the EU FemTech market by 2030, due to newly adopted public and private insurance programs for reproductive health and mental health solutions. Other EU countries such as France and Italy will also show strong adoption, but cultural barriers may slow early-stage penetration compared to Northern Europe. As awareness campaigns and patient advocacy groups continue to grow, consumer adoption will increase by 30% by 2030, while cultural stigmas surrounding women’s health will begin to ease. East and Southern European countries will follow, with Spain and Poland experiencing the fastest growth in FemTech adoption. Regulatory frameworks, including the EU Health Digitalization Strategy, will provide the necessary backbone to ensure cross-border interoperability and data privacy standards across countries, which will drive overall FemTech market expansion in Europe.

Competitive Landscape

The FemTech market is led by global companies like Elvie, Clue, and Flo Health, which dominate the mobile health app segment. Startups focusing on AI-driven diagnostics for women’s health are emerging as key players, with platforms like Maven Clinic and Ovia Health advancing AI-powered fertility, menstrual health solutions, and mental health support. Key players in the sector also include Babylon Health and Cigna, which are expanding their reach through global digital health programs. Insurance companies are becoming integral players, offering reimbursement packages for FemTech services, thus reducing financial barriers for women’s health solutions. By 2030, private insurance providers will lead, with public health schemes following closely behind. Emerging players are differentiating by AI-enabled personalization, user-friendly interfaces, and affordable subscription models. Pricing strategies in FemTech products typically range from €3–€15/month for mobile apps and €80–€150 per consultation for virtual consultations, with teletherapy services offering bundled packages for continued care. The competitive advantage lies in the ability to scale both telehealth services and mobile solutions, expand reimbursement models, and continually innovate with AI-based diagnostics to meet consumer needs.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071