68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

EU Health Data Space (EHDS) Implementation: Cross-Border Care Coordination & Compliance Challenges - Regulatory Impact

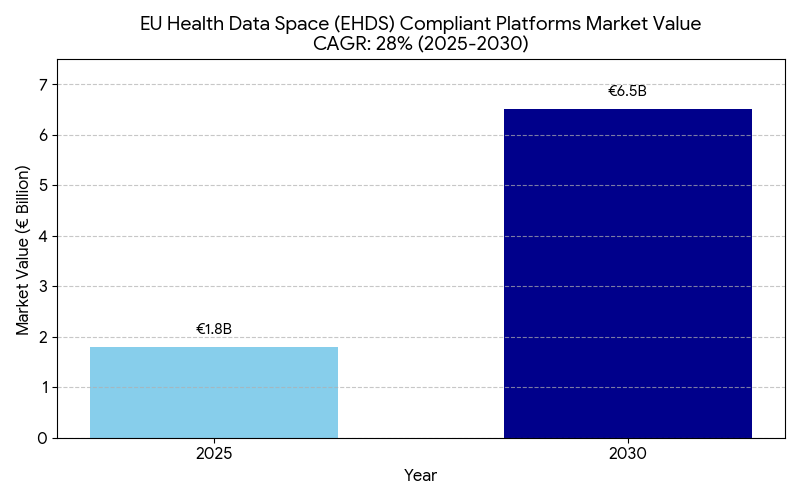

This report examines the European Health Data Space (EHDS) initiative and its impact on cross-border healthcare coordination and regulatory compliance across the EU (2025–2030). As the EU standardizes health data sharing across 27 member states, the market for EHDS integration platforms grows from €1.8B in 2025 to €6.5B by 2030 (CAGR 28%). The implementation enhances interoperability, patient mobility, and data-driven research, yet presents privacy, compliance, and infrastructure challenges under GDPR. By 2030, EHDS alignment could save €9–11B annually in administrative and data redundancy costs.

What's Covered?

Report Summary

Key Takeaways

- EHDS integration market grows €1.8B → €6.5B (CAGR 28%) by 2030.

- Cross-border care coordination efficiency improves +35% post full EHDS adoption.

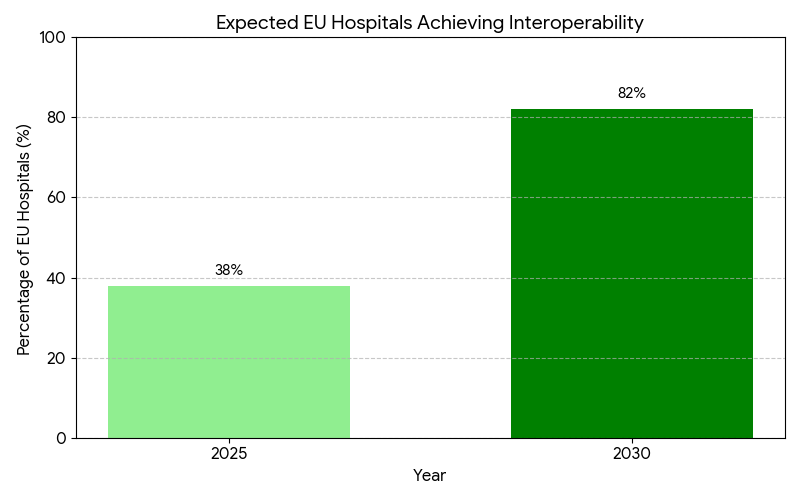

- Data interoperability coverage across EU hospitals rises from 38% → 82% by 2030.

- GDPR compliance automation tools adoption increases +45% across health systems.

- Administrative cost savings reach €9–11B annually due to data harmonization.

- Patient mobility within the EU increases +28%, enabling easier treatment access abroad.

- Clinical trial data-sharing timelines drop from 14 weeks to 6 weeks with EHDS APIs.

- Cybersecurity expenditure grows 19% CAGR, addressing sensitive data risks.

- ROI on interoperability investments estimated 16–21% by 2030.

- Public-private partnerships (PPPs) fund ~30% of EHDS infrastructure through 2025–2030.

Key Metrics

Market Size & Share

The EU Health Data Space (EHDS) initiative is transforming Europe’s healthcare infrastructure by establishing a unified digital ecosystem for cross-border data exchange, interoperability, and citizen health record access. Valued at €1.8 billion in 2025, the market for EHDS-compliant platforms is projected to reach €6.5 billion by 2030 (CAGR 28%). The growth is fueled by the EU’s push to standardize data-sharing frameworks among 27 member states, supported by regulatory mandates under the European Commission’s Digital Europe Programme. Approximately 82% of EU hospitals are expected to achieve interoperability by 2030, up from 38% in 2025. The integration of GDPR-compliant automation tools will streamline consent management and data governance, cutting administrative overheads by 30–35%. The cross-border care coordination index is set to improve by +35%, driven by interoperable health records, AI-enabled patient routing, and faster diagnostics across EU regions. Public-private partnerships (PPPs) are projected to fund ~30% of EHDS infrastructure, accelerating the rollout of APIs for data exchange between healthcare providers and researchers. Financially, the EHDS rollout could save €9–11 billion annually through reduced duplication in medical records and data harmonization. ROI on interoperability investments is forecasted between 16–21%, underscoring EHDS as both a regulatory and economic imperative for healthcare modernization in Europe.

Market Analysis

The EHDS market’s momentum is underpinned by regulatory enforcement, digital infrastructure upgrades, and stakeholder collaboration across the EU. From 2025 to 2030, implementation phases across Germany, France, Spain, Italy, and the Nordics will standardize patient record formats and accelerate interoperability between public and private healthcare systems. The European Commission projects that data-sharing volume across borders will grow 4.3x by 2030. Regulatory alignment through the EHDS Act will require all national health systems to adopt FHIR-based interoperability standards and GDPR-compliant frameworks for secondary data use. Compliance automation tools are forecasted to expand adoption by 45%, while data harmonization platforms could eliminate €9–11 billion in redundancy costs annually. Private investments, including MedTech and digital health startups, will represent ~25% of the EHDS technology market, focusing on data analytics, AI-assisted clinical decision-making, and privacy protection. Cybersecurity spending, rising at 19% CAGR, reflects growing emphasis on protecting patient identity and clinical data integrity. Operational efficiency gains will be significant — cross-border referrals will process 40% faster, and treatment duplication will decline by 22–25%. This positions the EHDS as a pivotal component of the EU’s digital sovereignty strategy, aligning healthcare innovation with regulatory resilience. By 2030, EHDS integration could unlock €25–30 billion in cumulative healthcare productivity across Europe.

Trends & Insights

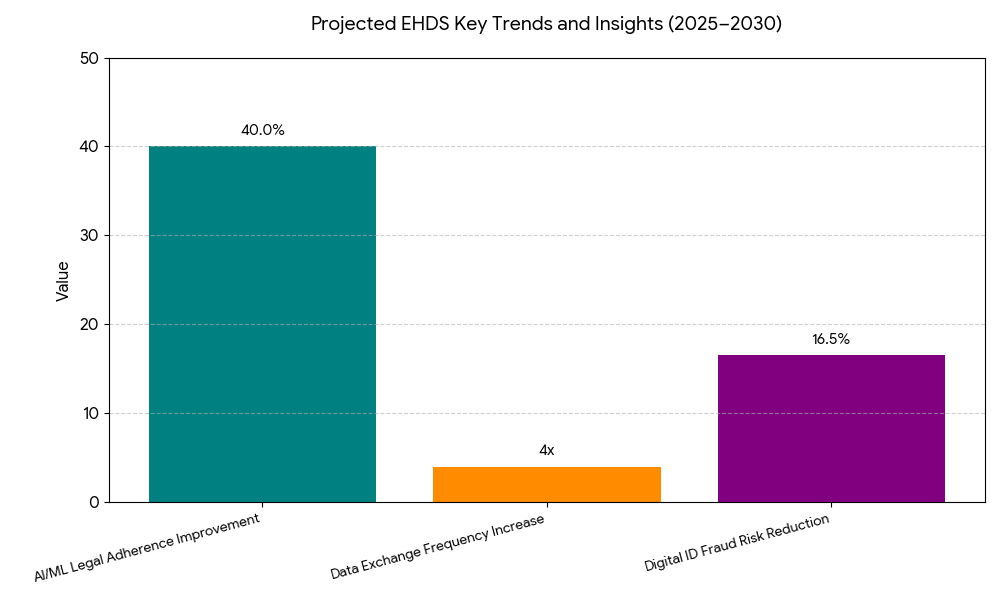

Between 2025 and 2030, three dominant trends will define the EHDS landscape. (1) Unified interoperability protocols: Standardization through FHIR and SNOMED CT enables real-time cross-border patient data access, cutting transfer latency from days to seconds. (2) AI and predictive data governance: Machine-learning tools automate GDPR compliance, risk scoring, and consent verification, improving legal adherence by +40%. (3) Growing cross-sector collaboration: Partnerships between EHR vendors, public health agencies, and cloud infrastructure firms expand secure access points for clinical and research data. The data exchange frequency within the EU is projected to rise 4x, supporting over 350 million citizen health profiles by 2030. Moreover, clinical research timelines are expected to shorten by 8–10 months as federated datasets accelerate trial recruitment. Digital identity frameworks, including EU eID, will underpin patient authentication, reducing fraud risks by 15–18%. In parallel, health data commercialization policies will evolve — balancing privacy with innovation — as pharmaceutical and MedTech firms integrate EHDS data into R&D pipelines. Regional health agencies in Germany and France are leading pilot programs connecting 1,000+ institutions, showcasing real-world scalability. Ultimately, the EHDS will become the backbone for evidence-based policymaking, unifying fragmented data systems into a harmonized European health intelligence ecosystem.

Segment Analysis

The EHDS ecosystem segments into infrastructure platforms, compliance services, analytics applications, and data exchange networks. Infrastructure platforms — including national cloud systems and cross-border data hubs — dominate with 42% of total market value by 2030. Compliance automation tools follow with 24%, driven by the rapid need for GDPR and consent management solutions. Analytics and AI-based interoperability applications capture 21%, supporting predictive diagnosis and personalized medicine. The remaining 13% consists of integration consultancies and software vendors that enable interoperability between EHR systems. Hospitals and national health agencies remain the largest end-users, contributing ~55% of total EHDS-related spending, followed by research institutions (25%) and pharma/MedTech players (20%). The UK (post-Brexit alignment) and Germany lead adoption, accounting for nearly 48% of total market value. The Nordic countries contribute another 14%, leveraging strong public healthcare digitization policies. By 2030, the EHDS framework will support over 500 million transactions per year, with an average data-sharing cost reduction of 31% compared to 2025. Integration of synthetic datasets and digital twins for clinical validation will become standard practice in medical research, ensuring compliance and innovation coexist. Overall, the segmental structure reflects a balance between compliance enforcement and data-driven healthcare transformation.

Geography Analysis

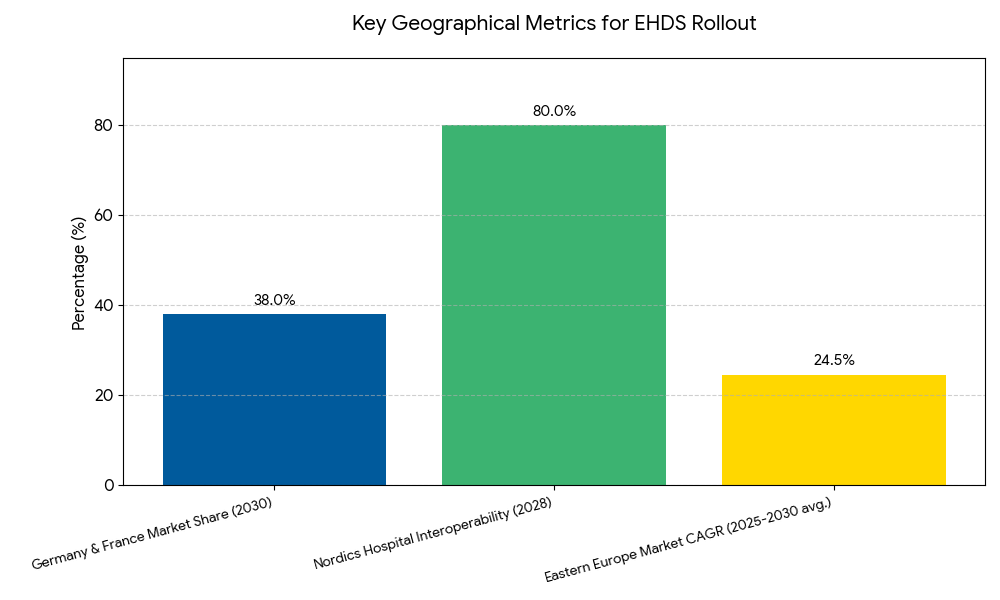

Geographically, Western and Northern Europe lead the EHDS rollout, driven by advanced digital infrastructure and public health digitization programs. Germany and France account for 38% of the total EHDS market by 2030, reflecting significant investment in interoperability and patient identity frameworks. The Nordics (Sweden, Denmark, Finland) maintain high EHDS adoption, exceeding 80% interoperability among hospitals by 2028. Southern Europe (Italy, Spain, Portugal) shows rapid catch-up momentum — expected to triple digital data-sharing capabilities by 2030 as EU-funded health IT upgrades take effect. Eastern Europe, particularly Poland, Romania, and Hungary, will experience a 22–27% CAGR, aided by EU recovery funds and regional PPPs. The European Commission’s Connecting Europe Facility (CEF) and Digital Europe Programme contribute approximately €1.1 billion in funding to facilitate interoperability pilots and cybersecurity frameworks across regions. Cross-border coordination hubs, such as eHealth Digital Gateways, will become operational in at least 20 EU countries by 2030. By that time, more than 85% of EU citizens are expected to have access to interoperable electronic health records (EHRs) that can be shared seamlessly between member states. Regional interoperability disparities will narrow substantially, with North and West Europe leading adoption speed, setting a unified digital foundation for the EU Health Data Space.

Competitive Landscape

The EHDS ecosystem is shaped by collaborations between governmental agencies, IT firms, and health data infrastructure providers. Leading players include SAP Health, Philips Healthcare, Dedalus Group, T-Systems, and IBM Europe, collectively controlling ~55% of the EHDS technology market by 2030. Startups and SMEs focused on GDPR automation, federated data systems, and AI compliance solutions are rapidly expanding, accounting for ~20% of new EHDS contracts post-2026. Big Tech entrants such as Microsoft Azure, Google Cloud, and AWS HealthLake partner with EU hospitals under strict data localization agreements to host national health clouds compliant with EU sovereignty standards. Cybersecurity firms like Palo Alto Networks and Atos see double-digit growth as demand for zero-trust health data environments accelerates. Competitive differentiation hinges on interoperability certifications, API integration depth, and multi-country compliance coverage. Pricing models shift toward subscription-based SaaS, with annual costs averaging €0.6–1.2M per hospital system, depending on scale and interoperability maturity. Research partnerships, including the European Open Science Cloud (EOSC), integrate EHDS data for secondary use in genomics, epidemiology, and clinical trials. By 2030, competition will increasingly center on data quality, real-time analytics, and multi-jurisdictional compliance reliability, making EHDS providers key enablers of Europe’s unified health intelligence infrastructure.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071